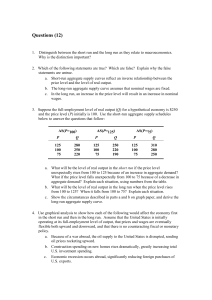

20 Aggregate Demand and Aggregate Supply Chapter

advertisement

Chapter 20 Aggregate Demand and Aggregate Supply Aggregate Demand & Aggregate Supply • Economic activity – Fluctuates from year to year • Economic fluctuation – Business cycle • Recession – Economic contraction – Period of declining real incomes and rising unemployment • Depression – Severe recession 2 3 Key Facts About Economic Fluctuations 1. Economic fluctuations are irregular and unpredictable – i.e, fluctuations (around the trend) = business cycles (booms/recessions) 2. Most macroeconomic quantities fluctuate together – GDP (growth rate) - Investment (I) – Unemployment Rate (U) – Inflation (∏) 3. As output falls, unemployment rises 3 Economic “Fluctuations” Irregular and Unpredictable 4 Economic “Fluctuations” Irregular and Unpredictable 5 Figure 1 A look at short-run economic fluctuations (a) This figure shows real GDP in panel (a), investment spending in panel (b), and unemployment in panel (c) for the U.S. economy using quarterly data since 1965. Recessions are shown as the shaded areas. Notice that real GDP and investment spending decline during recessions, while unemployment rises. 6 Figure 1 A look at short-run economic fluctuations (b) Note that real GDP and investment spending decline during recessions. Although I accounts for only 15-20% of GDP; it accounts for 50% of the decline in GDP during a recession 7 Figure 1 A look at short-run economic fluctuations (c) . Recessions are shown as the shaded areas. Notice that real GDP and investment spending decline during recessions, while unemployment rises. 8 Explaining Short-Run Economic Fluctuations • The assumptions of Classical economists – Austrian school (Hayek, von Mises) – Monetarists (Friedman, Univ of Chicago, “Fresh Water”) • Classical dichotomy – Separation of variables into • Real variables • Nominal variables • Monetary neutrality – Changes in the money supply • Affect nominal variables • Does not affect real variables 9 Explaining Short-Run Economic Fluctuations • Classical Economist Focus on the “Long-Run” – Classical theory holds • Changes in money supply – Affect prices, nominal interest rates and other nominal variables – Does not affect real GDP, unemployment, real interest rates, or other real variables 10 4 The long-run aggregate-supply curve (Classical View) Price Level Long-run aggregate supply P1 1. A change in the price P2 level . . . 2. . . . does not affect the quantity of goods and services supplied in the long run Natural rate of output Quantity of Output Classical View – Supply determines equilibrium (real Y -> thereby U) 11 Figure 11-5 Classical Theory and Increases in Aggregate Demand Explaining Short-Run Economic Fluctuations • The reality of short-run fluctuations • Short-run – Assumption of monetary neutrality - no longer appropriate (can affect real variables in short-run due to sticky prices/wages or “surprises” – Real and nominal variables are highly intertwined – Changes in the money supply • Can temporarily push real GDP away from its long-run trend 13 Explaining Short-Run Economic Fluctuations • Model of aggregate demand & aggregate supply – Model that most economists use to explain short-run fluctuations in economic activity • Around its long-run trend • Aggregate-demand curve – Shows the quantity of goods and services • That households, firms, the government, and customers abroad • Want to buy at each price level – Downward sloping 14 Figure 11-7 Demand-Determined Equilibrium Real GDP at Less Than Full Employment Keynes assumed prices will not fall when aggregate demand falls Figure 11-8 Real GDP and the Price Level, 1934–1940 6 Tradeoff between Inflation and Unemployment? Annual data from 1961 to 1968 shows a negative relationship between inflation and unemployment (inflation = stimulative monetary (M1) and fiscal (G) policy) 17 Explaining Short-Run Economic Fluctuations • Model of aggregate demand & aggregate supply • Aggregate-supply curve – Shows the quantity of goods and services • That firms choose to produce and sell • At each price level – Upward sloping (very different from Classical) • Similar factors that shift micro-based supply curve (input prices, technology) also shift AS curve – E.g., OPEC oil prices 18 Figure 2 Aggregate demand and aggregate supply Price Level Aggregate supply Equilibrium price level Aggregate demand Equilibrium output Quantity of Output Economists use the model of aggregate demand and aggregate supply to analyze economic fluctuations. On the vertical axis is the overall level of prices. On the horizontal axis is the economy’s total output of goods and services. Output and the price level adjust to the point at which the aggregate-supply and aggregate-demand curves intersect. 19 The Aggregate-Demand Curve • Why the aggregate-demand (AD) curve slopes downward • Y = C + I + G + NX • Three effects: – Wealth effect (C ): decrease in prices – consumable income increases – Interest-rate effect (I): need less money to buy goods -> increase loanable funds -> interest rate decreases – Exchange-rate effect (NX) -> dec in interest rate -> depreciaion of $ • Assumption: government spending (G) – Fixed by policy 20 Figure 3 The aggregate-demand curve Price Level P1 1. A decrease in the price P2 level . . . Aggregate demand Y1 Y2 Quantity of Output 2. . . . increases the quantity of goods and services demanded A fall in the price level from P1 to P2 increases the quantity of goods and services demanded from Y1 to Y2. There are three reasons for this negative relationship. As the price level falls, real wealth rises, interest rates fall, and the exchange rate depreciates. These effects stimulate spending on consumption, investment, and net exports. Increased spending on any or all of 21 these components of output means a larger quantity of goods and services demanded. The Aggregate-Demand Curve • Why the AD curve might shift • Changes in consumption, C – Events - change how much people want to consume at a given price level • Level of taxation (decrease in income taxes, increases spendable income -> increase C) • Decrease C: increase in the savings rate (marginal propensity to save) during a recession – Increase in consumer spending • Aggregate demand - shift right 22 The Aggregate-Demand Curve • Why the AD curve might shift • Changes in investment, I – Events - change how much firms want to invest at a given price level • Better technology • Tax policy (tax credits for I, faster depreciation) • Money supply, Federal Discount Rate, Budget deficit/surplus – Increase in investment • Aggregate demand - shift right 23 The Aggregate-Demand Curve • Why the AD curve might shift • Changes in government purchases, G – Policy makers – change government spending at a given price level • Build new roads – Increase in government purchases • Aggregate demand - shift right – Or decreases in government purchases • AD curve shifts left 24 The Aggregate-Demand Curve • Why the AD curve might shift – Decreases in government purchases Costs of government sequester • low 0.1 percent growth in personal income attributed todefense furloughs, more than 650,000 workers, – a 0.5 percent decline in government pay, reduced wages by $7.7 billion that month, – Without sequester, income growth would have been closer to 1.2 percent. 25 The Aggregate-Demand Curve • Why the AD curve might shift – If it sequester were reversed, the non-partisan Congressional Budget Office has estimated that as many as 1.6 million jobs would be added and GDP would get a boost of as much as 1.2 percent. Even the deficit would be in better shape if the cuts were undone. 26 The Aggregate-Demand Curve • Why the AD curve might shift • Changes in net exports, NX – Events - change net exports for a given price level • Recession in Europe –decrease demand US goods • International speculators – change in exchange rate – Increase in net exports • Decrease in exchange rate; US goods cheaper • Aggregate demand - shift right 27 The Aggregate Supply Curve • Long run – Aggregate-supply curve is vertical • Short run – Aggregate-supply curve is upward sloping • Why the aggregate-supply curve (LRAS) is vertical in the long run – Price level does not affect the long-run determinants of GDP: • Supplies of labor, capital, and natural resources • Available technology 28 Figure 4 The long-run aggregate-supply curve Price Level Long-run aggregate supply P1 1. A change in the price P2 level . . . 2. . . . does not affect the quantity of goods and services supplied in the long run Natural rate of output Quantity of Output In the long run, the quantity of output supplied depends on the economy’s quantities of labor, capital, and natural resources and on the technology for turning these inputs into output. Because the quantity supplied does not depend on the overall price level, the long-run aggregate-supply curve is vertical at the natural rate of output. 29 The Aggregate Supply Curve • Why the LRAS curve might shift • Natural rate of output – Production of goods and services – That an economy achieves in the long run • When unemployment is at its normal rate – Potential output – Full-employment output 30 The Aggregate Supply Curve • Why the LRAS curve might shift – Any change in natural rate of output • Changes in labor – Quantity of labor – increases • Aggregate supply – shifts right – Natural rate of unemployment – increases • Aggregate supply – shifts left 31 The Aggregate Supply Curve • Why the LRAS curve might shift • Changes in capital – Capital stock – increase • Aggregate supply – shifts left – Physical capital – Human capital 32 The Aggregate Supply Curve • Why the LRAS might shift • Changes in natural resources – New discovery of natural resource • Aggregate supply – shifts right – Weather – Availability of natural resources 33 The Aggregate Supply Curve • Why the LRAS curve might shift • Changes in technology – New technology, for given labor, capital and natural resources • Aggregate supply – shifts right – International trade – Government regulation 34 The Aggregate Supply Curve • Using AD and LRAS to depict long-run growth and inflation • In long run: both AD and LRAS curve shift • Continual shifts of LRAS curve to right – Technological progress • AD curve shifts to right – Monetary policy – The Fed increases money supply over time • Result: – Continuing growth in output – Continuing inflation 35 Figure 5 Long-run growth and inflation in the model of aggregate demand and aggregate supply Price Level 2. . . . and growth in the money supply shifts aggregate demand . . . 1. In the long run, technological progress shifts long-run aggregate Long-run aggregate supply, supply… LRAS1980 LRAS1990 LRAS2000 P2000 3. . . . leading to growth in output . . . P1990 P1980 AD2000 4. . . . and ongoing inflation AD1980 Y1980 Y1990 AD1990 Y2000 Quantity of Output As the economy becomes better able to produce goods and services over time, primarily because of technological progress, the long-run aggregate-supply curve shifts to the right. At the same time, as the Fed increases the money supply, the aggregate-demand curve also shifts to the right. In this figure, output grows from Y1980 to Y1990 and then to Y2000, and the price level rises from P1980 to P1990 and then to P2000. Thus, the model of aggregate 36 demand and aggregate supply offers a new way to describe the classical analysis of growth and inflation The Aggregate Supply Curve • Why the aggregate-supply (AS) curve slopes upward in the short-run – Basic Microeconomic Theory – Increase in overall level of prices in economy • Tends to raise the quantity of goods and services supplied – Decrease in level of prices • Tends to reduce quantity of goods and services supplied 37 Figure 6 The short-run aggregate-supply curve Price Level Short-run aggregate supply P1 1. A decrease in the price P2 level . . . Y2 Y1 Quantity of Output 2. . . . reduces the quantity of goods and services supplied in the short run In the short run, a fall in the price level from P1 to P2 reduces the quantity of output supplied from Y1 to Y2. This positive relationship could be due to sticky wages, sticky prices, or misperceptions. Over time, wages, prices, and perceptions adjust, so this positive relationship is only temporary. 38 The Aggregate Supply Curve • Why the AS curve slopes upward in short-run • Sticky-wage theory – Nominal wages - slow to adjust to changing economic conditions • Long-term contracts: workers and firms • Slowly changing social norms • Notions of fairness - influence wage setting – Nominal wages - based on expected prices • Don’t respond immediately when: – Actual price level – different from what was expected 39 The Aggregate Supply Curve • Why the AS curve slopes upward in short-run • Sticky-wage theory – If price level < expected • Firms – incentive to produce less output – If price level > expected • Firms – incentive to produce more output 40 The Aggregate Supply Curve • Why the AS curve slopes upward in short-run • Sticky-price theory – Prices of some goods & services • Slow to adjust to changing economic conditions • Menu costs – Costs to adjusting prices 41 The Aggregate Supply Curve • Why the AS curve slopes upward in short-run • Misperceptions theory – Changes in the overall price level • Can temporarily mislead suppliers – About changes in individual markets – Changes in relative prices • Suppliers - respond to changes in level of prices – Change - quantity supplied of goods and services 42 The Aggregate Supply Curve • Why the AS curve slopes upward in short-run • Quantity of output supplied = = Natural rate of output + + a(Actual price level – Expected price level) • Where a - number that determines how much output responds to unexpected changes in the price level 43 The Aggregate Supply Curve • Why the short-run AS curve might shift • Changes in labor, capital, natural resources, or technological knowledge – Shift the short-run AS curve • Expected price level increases – Aggregate-supply curve – shifts left 44 Table 2 The short-run aggregate-supply curve: summary (a) Why Does the Short-Run Aggregate-Supply Curve Slope Upward? 1. The Sticky-Wage Theory: An unexpectedly low price level raises the real wage, which causes firms to hire fewer workers and produce a smaller quantity of goods and services. 2. The Sticky-Price Theory: An unexpectedly low price level leaves some firms with higher-than desired prices, which depresses their sales and leads them to cut back production. 3. The Misperceptions Theory: An unexpectedly low price level leads some suppliers to think their relative prices have fallen, which induces a fall in production. 45 Table 2 The short-run aggregate-supply curve: summary (b) Why Might the Short-Run Aggregate-Supply Curve Shift? 1. Shifts Arising from Labor: An increase in the quantity of labor available (perhaps due to a fall in the natural rate of unemployment) shifts the aggregate-supply curve to the right. A decrease in the quantity of labor available (perhaps due to a rise in the natural rate of unemployment) shifts the aggregate-supply curve to the left. 2. Shifts Arising from Capital: An increase in physical or human capital shifts the aggregate-supply curve to the right. A decrease in physical or human capital shifts the aggregate-supply curve to the left. 3. Shifts Arising from Natural Resources: An increase in the availability of natural resources shifts the aggregate-supply curve to the right. A decrease in the availability of natural resources shifts the aggregate-supply curve to the left. 4. Shifts Arising from Technology: An advance in technological knowledge shifts the aggregate-supply curve to the right. A decrease in the available technology (perhaps due to government regulation) shifts the aggregate-supply curve to the left. 5. Shifts Arising from the Expected Price Level: A decrease in the expected price level shifts the shortrun aggregate-supply curve to the right. An increase in the expected price level shifts the short-run aggregate-supply curve to the left. 46 Two Causes of Economic Fluctuations • Assumption – Economy begins in long-run equilibrium • Long-run equilibrium: – Intersection of AD and LRAS curves • Output - natural rate • Actual price level – And: Intersection of AD and short-run AS curve • Expected price level = Actual price level 47 Figure 7 The long-run equilibrium Price Level Equilibrium price Long-run aggregate supply Short-run aggregate supply A Aggregate demand Natural rate of output Quantity of Output The long-run equilibrium of the economy is found where the aggregate-demand curve crosses the long-run aggregate-supply curve (point A). When the economy reaches this long-run equilibrium, the expected price level will have adjusted to equal the actual price level. As a result, the short-run aggregate-supply curve crosses this point as well. 48 Two Causes of Economic Fluctuations • The effects of a shift in aggregate demand • Wave of pessimism – Affects aggregate demand • Aggregate demand – shifts left – Short-run • Output falls & Price level falls – Long-run • Short-run aggregate supply curve – shifts right • Output – natural rate • Price level – falls 49 Table 3 Four steps for analyzing macroeconomic fluctuations 1. Decide whether the event shifts the aggregate demand curve or the aggregate supply curve (or perhaps both). 2. Decide in which direction the curve shifts. 3. Use the diagram of aggregate demand and aggregate supply to determine the impact on output and the price level in the short run. 4. Use the diagram of aggregate demand and aggregate supply to analyze how the economy moves from its new short-run equilibrium to its long-run equilibrium. 50 Figure 8 A contraction in aggregate demand Price Level Short-run aggregate supply, AS1 Long-run aggregate supply AS2 P1 3. . . . but over time, the short-run aggregate-supply curve shifts . . . A B P2 C 4. . . . and output returns to its natural rate. P3 1. A decrease in aggregate demand . . . AD2 Y2 Aggregate demand, AD1 Y1 Quantity of Output 2. . . . causes output to fall in the short run . . . A fall in aggregate demand is represented with a leftward shift in the aggregate-demand curve from AD1 to AD2. In the short run, the economy moves from point A to point B. Output falls from Y1 to Y2, and the price level falls from P1 to P2. Over time, as the expected price level adjusts, the short-run aggregate-supply curve shifts to the right from AS1 to AS2, and the economy reaches point C, where the new aggregate-demand curve crosses the long-run aggregate51 supply curve. In the long run, the price level falls to P3, and output returns to its natural rate, Y1. Two big shifts in aggregate demand: Great Depression and World War II • Early 1930s: large drop in real GDP – The Great Depression – Largest economic downturn in U.S. history – From 1929 to 1933 • Real GDP fell by 27% • Unemployment rose from 3 to 25% • Price level fell by 22% – Cause: decrease in aggregate demand • Decline in money supply (by 28%) • Decreasing: consumer spending, investment spending 52 Two big shifts in aggregate demand: Great Depression and World War II • Early 1940s: large increase in real GDP – Economic boom – World War II • • • • • • More resources to the military Government purchases increased Aggregate demand – increased 1939 - 1944 Doubled the economy’s production of goods and services 20% increase in the price level Unemployment fell from 17 to 1% 53 Figure 9 U.S. real GDP growth since 1900 Over the course of U.S. economic history, two fluctuations stand out as especially large. During the early 1930s, the economy went through the Great Depression, when the production of goods and services plummeted. During the early 1940s, the United States entered World War II, and the economy experienced rapidly rising production. Both of these events are usually explained by large shifts in aggregate demand. 54 The recession of 2001 • 2001: Recession – Unemployment rate • • • • December 2000: 3.9% August 2001: 4.9% June 2003: 6.3% January 2005: 5.2% • Three events – decrease in aggregate demand 1. The end of dot-com bubble in stock market • Stock prices fell (25%) • Reduced consumer & investment spending • Aggregate-demand curve - shifted to left 55 The recession of 2001 • Three events – decrease in aggregate demand 2. Terrorist attacks on September 11, 2001 • Stock market fell (12%) in one week • Increased uncertainty about the future • Aggregate-demand curve – shifted further to left 3. Series of corporate accounting scandals • Enron and WorldCom • Stock market fell • Aggregate-demand curve – shifted further to left 56 The recession of 2001 • 2001: Recession – Policymakers - quick to respond – The Fed - expansionary monetary policy • Interest rates fell; Federal funds rate fell • Stimulated spending – Congress • Tax cut in 2001; Immediate tax rebate; Tax cut in 2003 • To stimulate consumer & investment spending – Aggregate-demand curve – shifted to right • Offset the three contractionary shocks 57 Two Causes of Economic Fluctuations • The effects of a shift in aggregate supply • Start: long run equilibrium – Firms – increase in production costs • Aggregate supply curve – shifts left • Short-run – Output falls & Price level rises – Stagflation • Long-run, if AD is held constant – Short-run AS shifts back to right – Output – natural rate – Price level - falls 58 Figure 10 An adverse shift in aggregate supply Price Level Long-run aggregate supply AS2 1. An adverse shift in the short-run aggregate-supply curve . . . Short-run aggregate supply, AS1 B P2 3. . . . and the price P1 level to rise A Aggregate demand Y2 Y1 Quantity of Output 2. . . . causes output to fall . . . When some event increases firms’ costs, the short-run aggregate-supply curve shifts to the left from AS1 to AS2. The economy moves from point A to point B. The result is stagflation: Output falls from Y1 to Y2, and the price level rises from P1 to P2. 59 Two Causes of Economic Fluctuations • The effects of a shift in aggregate supply • Start: long run equilibrium – Firms – increase in production costs • Aggregate supply curve – shifts left • Short-run – Output falls and Price level rises • Long-run – Policymakers – shift AD to right – Output – natural rate – Price level – rises 60 Figure 11 Accommodating an adverse shift in aggregate supply Price Level 3. . . . which causes the price level to rise further . . . Long-run aggregate supply P3 P2 C P1 A AS2 1. When short-run aggregate supply falls . . . Short-run aggregate supply, AS1 2. . . . policymakers can accommodate the shift by expanding aggregate demand . . . AD2 Aggregate demand, AD1 4. . . . but keeps output at its natural rate. Y1 Quantity of Output Faced with an adverse shift in aggregate supply from AS1 to AS2, policymakers who can influence aggregate demand might try to shift the aggregate-demand curve to the right from AD1 to AD2. The economy would move from point A to point C. This policy would prevent the supply shift from reducing output in the short run, but the price level would permanently rise from P1 to P3. 61 Oil and the economy • Economic fluctuations in the U.S. economy – Since 1970 – Some: originated in the oil fields of the Middle East • Some event - reduces the supply of crude oil flowing from Middle East – Price of oil - rises around the world – Aggregate-supply curve – shifts left – Stagflation • Mid-1970s • Late-1970s 62 Oil and the economy • Some event – increases the supply of crude oil from Middle East – Price of oil decreases – Aggregate-supply curve – shifts right • Output – rapid growth • Unemployment – falls • Inflation rate – falls 63 Oil and the economy • Recent years: World market for oil – not an important source of economic fluctuations – Conservation efforts – Changes in technology • 2008 - world oil prices – rising significantly – Increased demand from a rapidly growing China 64