Questions (13)

advertisement

")

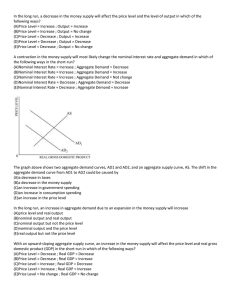

Questions (13) 1. What are the four supply factors of economic growth? What is the demand factor? What is he efficiency factor? Illustrate these factors in terms of the production possibilities curve. 2. What is the relationship between a nation’s production possibilities curve and its long-run aggregate supply curve? How does each relate to the idea of a New Economy? 3. Between 1990 and 2005 the U.S. price level rose by about 50 percent while real output increased by about 56 percent. Use the aggregate demand-aggregate supply model to illustrate these outcomes graphically. 4. To what extent have increases in U.S. real GDP resulted from more labor inputs? From higher labor productivity? Rearrange the following contributors to the growth of real GDP in order of their quantitative importance: economies of scale, quantity of capital, improved resource allocation, education and training, technological advance. 5. True or false? If false, explain why. a. Technological advance, which to date has played a relatively small role in U.S. economic growth, is destined to play a more important role in the future. b. Many public capital goods are complementary to private capital goods. c. Immigration has slowed economic growth in the U.S. 6. Explain why there is such a close relationship between changes in a nation’s rate of productivity growth and changes in its average real hourly wage. 7. Relate each of the following to the New Economy: a. The rate of productivity growth b. Information technology c. Increasing returns d. Network effects e. Global competition 8. Provide three examples of products or services that can be simultaneously consumed by many people. Explain why labor productivity greatly rises as the firm sells more units of the product or service, and explain why the higher level of sales greatly reduces the perunit cost of the product.