Economics is frequently referred to as the marginalist paradigm. ... economic decisions by the comparing the marginal (additional) benefits and... Homework Assignment #1

advertisement

benefits and... Homework Assignment #1")

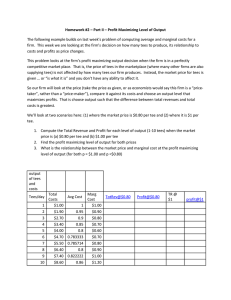

Homework Assignment #1 Computing Marginal Value Economics is frequently referred to as the marginalist paradigm. That is, we typically model most economic decisions by the comparing the marginal (additional) benefits and marginal costs of the alternatives. This week’s exercise looks at how we compute marginal values for a couple of economic problems. First, given a schedule (or table) for price, quantity and total revenue at each price point for a hypothetical golf tee manufacturer, we will compute the total and marginal revenue at each price/quantity point. Total Revenue equals price per tee times the number of tees sold. Marginal revenue is simply the change (increase or decrease) in total revenue when the next (marginal) tee is sold at the market price. For example, the Marginal Revenue for the 2nd tee equals the difference between the Total Revenue when 2 tees are sold minus the Total Revenue when only 1 tee is sold. It measures how much total revenue changes when 1 more tee (than before) is sold. Here’s the table. Compute Total Revenue and Marginal Revenue for each tee sold (from 1 to 10 tees) and fill the table in. Price per #Tees Total Marginal tee sold Revenue Revenue $10 1 9 2 8 3 7 4 6 5 5 6 4 7 3 8 2 9 1 10 a) At what price and quantity is Total Revenue Maximized? P=_______ Q=____________ b) As price decreases, up to where Tot Rev is maximized, what is happening to Marginal Revenue? c) What is the value of Marg Rev when Tot Rev is max’ed? 1 d) After Tot Rev is max’ed, what happens to Marg Rev as price continues to fall? Economists also model the supplier, or firm’s, decision about how much to produce as a marginalist decision. That is, a firm decides whether or not to produce a good by comparing the market price for the good against the firm’s cost or producing the good …. At the margin. Alternatively, we could choose to maximize profits by finding the quantity of output where the difference between total revenues and total costs is greatest. But, as we will see later, marginal analysis will lead to the same output decision and is simpler and quicker to compute. Here is the manufacturer’s production cost table. Compute the Average and Marginal Costs of producing golf tees from 1 to 10. output of tees and costs Total Avg Tees/day Costs Cost 1 $1.00 2 $1.90 3 $2.70 4 $3.40 5 $4.00 6 $4.70 7 $5.50 8 $6.40 9 $7.40 10 $8.60 Marg Cost compute 1) average costs (from tees = 1 to 10) 2) compute marginal cost (increase in cost of producing 1 more tee from tees = 2 to 10) 2 3) what is the relationship between increases/decreases in average costs and increases/decreases in marginal costs – before and after the point of minimum average cost 3