Econ 201 Principles of Microeconomics Lecture #1.2 1-06-2009

advertisement

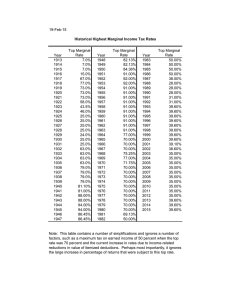

Econ 201 Principles of Microeconomics Lecture #1.2 1-06-2009 Economics as a Marginalist Paradigm Why Marginal Anything? • According to economic theory: – Decisions are made at the margin – Firms • Decision on how much to supply is determined by comparing additional (marginal) costs of producing one more unit to additional (marginal) revenue – Consumers • Compare marginal value (in use) of consuming the good versus the additional (marginal) cost of purchase (or price paid) Today • Look at how to compute (and why it’s important): – Marginal Cost of production for a firm • Derived from total costs of production – Total costs only determine whether or not firm enters an industry, not how much to produce/supply – Marginal Value of consumption for an individual • Derived from the individual’s demand curve • People compare at the margin to determine how much to buy Marginal Costs – What do we mean by marginal costs? • incremental, or additional, costs of producing one more unit of output – Difference in total costs of producing one more unit – Marginal cost of the 4th unit = Total Costs of the 4th unit minus the Total Costs of the 3rd unit MC[4] = TC[4] – TC[3] A Numeric Example • From Alchian and Allen # Tees produced daily Total Costs 0 $1.00 1 $1.90 2 $2.70 3 $3.40 4 $4.00 5 $4.70 6 $5.50 7 $6.40 8 $7.40 9 $8.60 Marginal Costs A Numeric Example • What Are the Marginal Costs # Tees produced daily Total Costs Marginal Costs 0 $1.00 --- 1 $1.90 $0.90 2 $2.70 $0.80 3 $3.40 $0.70 4 $4.00 $0.60 5 $4.70 $0.70 6 $5.50 $0.80 7 $6.40 $0.90 8 $7.40 $1.00 9 $8.60 $1.20 All of the Numbers # tees/day Total Cost Marg Cost Total Rev Marg Rev Profit Marg Profit 0 $1.00 $1.00 $0.00 $0.00 -$1.00 -$1.00 1 $1.50 $0.50 $1.00 $1.00 -$0.50 $0.50 2 $2.70 $1.20 $2.00 $1.00 -$0.70 -$0.20 3 $3.40 $0.70 $3.00 $1.00 -$0.40 $0.30 4 $4.00 $0.60 $4.00 $1.00 $0.00 $0.40 5 $4.70 $0.70 $5.00 $1.00 $0.30 $0.30 6 $5.50 $0.80 $6.00 $1.00 $0.50 $0.20 7 $6.40 $0.90 $7.00 $1.00 $0.60 $0.10 8 $7.40 $1.00 $8.00 $1.00 $0.60 $0.00 9 $8.60 $1.20 $9.00 $1.00 $0.40 -$0.20 What Do They Mean? Marginal and Total Costs increasing at Increasing rate Total and Marginal Costs Total and Marginal Costs Cost in Dollars $10.00 $8.00 $6.00 $4.00 $2.00 $0.00 0 Total Cos t Marg Cos t 1 2 3 4 5 6 # of Tees per day 7 8 9 Marginal Costs at Minimum, TC increasing at dec rate What’s It Mean to a Supplier? • Firm’s supply decision – Supply up to the point where p = MC • Profit maximizing point Profit Max Dollars Profits, Marginal Revenues & Costs $1.40 $1.20 $1.00 $0.80 $0.60 $0.40 $0.20 $0.00 MR = MC $1.00 $0.50 $0.00 -$0.50 -$1.00 -$1.50 0 1 2 3 4 5 6 # tees per day 7 8 9 Marg Rev Marg Cost Profit From the Demand Side • First Law of Demand – What Does Law Of Demand Mean? – all other factors being equal, as the price of a good or service increases, consumer demand for the good will decrease and vice versa. • Investopedia explains Law Of Demand... – summarizes the effect price changes on consumer behavior. For example, a consumer will purchase more pizzas if the price of pizza falls. The opposite is true if the price of pizza increases. – http://www.investopedia.com/terms/l/lawo fdemand.asp A Demand Example Price Individual's Demand Curve Qty Demanded $10.00 1 $9.00 2 $8.00 3 $7.00 4 $6.00 5 $5.00 6 $4.00 7 $3.00 8 $2.00 9 $1.00 10 Price per unit $12.00 $10.00 $8.00 $6.00 Price $4.00 $2.00 $0.00 1 2 3 4 5 6 7 Quantity Demanded 8 9 10 Consumer’s Marginal Value • Some basic definitions – Total Willingness-to-pay: “value in use” • How much would you be willing to pay for x units of the good than go entirely without? – Equals the area under the demand curve up to x units Individual's Demand Curve WTP for 4 units Price per unit $12.00 $10.00 $8.00 $6.00 Price $4.00 $2.00 $0.00 1 2 3 4 5 6 7 Quantity Demanded 8 9 10 Computing Marginal Value Price Qty Demanded $10.00 1 $9.00 2 $8.00 3 $7.00 4 $6.00 5 $5.00 6 $4.00 7 $3.00 8 $2.00 9 $1.00 10 Total and Marginal Value Price Qty Demanded Amt Paid Marginal Value Total Value Price x Qty Dem $10.00 1 $10.00 $10.00 $10.00 $9.00 2 $18.00 $9.00 $19.00 $8.00 3 $24.00 $8.00 $27.00 $7.00 4 $28.00 $7.00 $34.00 $6.00 5 $30.00 $6.00 $40.00 $5.00 6 $30.00 $5.00 $45.00 $4.00 7 $28.00 $4.00 $49.00 $3.00 8 $24.00 $3.00 $52.00 $2.00 9 $18.00 $2.00 $54.00 $1.00 10 $10.00 $1.00 $55.00 Area under Demand Difference in TV(3)-TV(2) MV is also equal to price paid In Graphic Terms Note: (again) price = marginal value Consumer is willing to buy up to P = MV Dollars Price, Total & Marginal Use Value $12.00 $10.00 $8.00 $60.00 $50.00 $40.00 $6.00 $4.00 $2.00 $0.00 $30.00 $20.00 $10.00 $0.00 1 2 3 4 5 6 7 8 Quantity Demanded 9 10 Price Marginal Value Total Value What Have We Learned? • How to compute marginal or incremental values – Marginal cost: the additional (change in Total Costs) of producing one more unit – Marginal value: the value to a consumer of purchasing one more unit The Bigger Lesson • Sell rule for firms – Firms will supply up to the point where the MC of producing the next unit are just equal to the price it receives for the good • First law of supply: supply curves will be upward sloping • Buy rule for consumers – Consumers will buy up to the point that price equals MV • First law of demand: demand curves are downward sloping • Negative slope diminishing marginal value of consuming next unit