Capital markets and resource mobilisation (multilateral institutions)

")

Capital Markets and

Resource Mobilization

IFC presentation to:

THIRD REGIONAL CONSULTATION ON

“RETHINKING THE ROLE OF NATIONAL

DEVELOPMENT FINANCE INSTITUTIONS IN

AFRICA”

By Louis-B. Ngassa Batonga

Principal Investment Officer

IFC-Johannesburg Office

November 2006

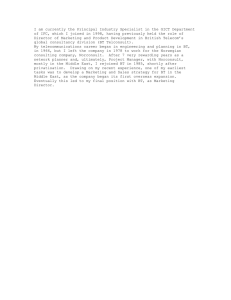

Growing interest of major international financial institutions in financing private sector

IFI Private Sector Volumes by Major Groups

25

20

15

10

5

0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Other MDB

EDFI

OPIC

EIB

EBRD

IFC

Changes in the allocation of IFI resources over the recent years

• Declining share of the Sub-Saharan Africa (9.7% of total allocations of US$23.6 billion in 2005 as compared to 12.1% of the year 2000 US$10.3 billion allocations)

• Increased shares of the Europe and Middle-East North Africa regions, with Europe now accounting for 50.8% of total allocations

• More resources being channeled into Financial Markets: 45.1% of the allocations in 2005 as compared to 29.5% in 2000.

Such changes create new challenges to DFIs and for institutions such as IFC. Hence the need to rethink their strategies.

IFC’s Five Strategic Priorities

1.

Strengthen the focus on Frontier Markets, in particular

Africa, with emphasis on technical assistance, investment climate and SMEs

2.

Build Long-term partnerships with emerging global players (South-South) capitalizing on the strengths of clients in China, India, Brazil, South Africa, etc.

3.

Help expand the sustainability agenda

4.

Address constraints to private sector growth in infrastructure, health and education

5.

Continue to emphasize local financial market development

IFC Role in Mobilization and capital Markets

• Mobilization of 3rd party capital, a major IFC role

• Investment criteria limits IFC participation, forcing mobilization

• Capital Market development, also seen as a major role for IFC

• Development of sustainable financing

• Clients want IFC to mobilize funding

Top 6 Reasons African Borrowers Work with IFC

16%

14%

12%

10%

8%

6%

4%

2%

0%

Stam p of

Approval

Long-term

Partner

Long Tenors Mobilization Ris k Mitigation Pricing

How IFC does Mobilization

• B Loans

- Open local markets to foreign banks and introduce them to clients

- Help to demonstrate mis-perceptions of risk in these markets

• Local Currency

Helps to increase the depth and liquidity of cross border swap markets

Swap market development is an important factor for overall capital market development

• Securitization and Guarantees

Help to deepen and broaden domestic financial markets

Help to improve risk appetite of domestic financial institutions

IFC Mobilization: B Loan Program

• Began in 1957

• Has mobilized US$25 billion

• Maintains a portfolio of US$ 5.1 billion

• Mobilized over US$1.6 billion in FY06 (US$1.1 billion in FY05)

• In FY06:

•

• Average B Loan Size: US$60m

Average Tenor: 7.1 years

B Loan Structure

Participation

Agreements

B Loan

Participants

Loan Agreement

Borrower

A + B Loans

• One loan agreement - IFC is lender of record and administers entire loan

• IFC fully shares project risks with participants

• Offshore participants, not per se local currency

IFC

’

s Local Currency Financing Instruments Using

Derivatives

• Two main local currency alternatives

•

• Local currency swaps

Overlay swaps

• Local Currency Swap: IFC swaps its own hard currency financing for local currency at time of disbursement

• Overlay Swap: IFC assists in obtaining local currency swap for existing third party loans

• Need the following to implement

•

• Existence of long term swap market

Regulatory approval

• IFC able to provide swaps in 8 African countries

IFC

’

s Local Currency Loans and Swaps

• South Africa : Up to 20 years, fixed and floating rate based on JIBAR and Prime

• Nigeria : Up to 10 years, fixed and floating rate based on 90 / 180 Day T-Bills

• Ghana : Up to 7 years, fixed and floating rate based on 90 / 180 Day T-Bills

• Kenya : Up to 10 years, fixed and floating rate based on 90 / 180 Day T-Bills

• Botswana : Up to 15 years, fixed and floating rate based on government bond yields

• Tanzania : Up to 7 years, fixed and floating rate based on 90 / 180 Day T-Bills

• Zambia : Up to 7 years, fixed and floating rate based on 90 / 180 Day T-Bills

• Uganda : Up to 7 years, fixed and floating rate based on 90 / 180 Day T-Bills

(*) For variable rate instruments other indexes than the ones mentioned above can be considered on a case by case basis

IFC

’

s Existing Portfolio and Pipeline of Local Currency

Transactions

Existing Portfolio

• 21 projects in 4 countries

• 1st transaction was in 1997

• US$210 million equivalent committed

• US$162 million disbursed

• Transactions completed for financial institutions and the general manufacturing sector, agribusiness and oil & gas sectors

Current Pipeline

• Over 10 projects in about 6 countries

• Current local currency transactions in the pipeline are targeting the financial services industry, the housing sector, agribusiness companies and the health & education sector

Structured Finance and Guarantees

• Partial Credit Guarantees (PCGs)

• IFC irrevocably guarantees a portion of the debt service due on a local currency bond or loan

• Partial debt service coverage insures that domestic investors take at least a portion of the borrower credit risk

• Risk-sharing Facilities

• Provides portfolio insurance for banks lending local currency to domestic borrowers.

• IFC guarantees part of the principal balance of an on-balance sheet portfolio of loans

• Securitization

• Allows clients to raise local currency funding through sale of assets from their balance sheet

• Can be used to issue debt at ratings higher than that of the borrower itself

• IFC credit enhances securitization through provision of guarantees on part of the capital structure or through purchase of subordinated tranches .

Structured Finance at IFC

Completed 62 transactions in 22 different countries

Mobilized a total of US$5,434mn (US$1,579mn during FY06) with

IFC’s credit exposure of only US$1,034mn

Capital Market Development

• B Loans

• Opens market to foreign banks and introduces them to clients

• Helps to demonstrate mis-perceptions of risk in markets

• Local Currency

• Helps to increase the depth and liquidity of cross border swap markets

• Swap market development important for overall capital market development

• Securitization and Guarantees

• Helps to deepen and broaden domestic financial markets

• Helps to improve risk appetite of domestic financial institutions

IFC Financial Markets Strategy for the Future

• Continue to develop existing products

• B Loans, Local Currency, Structured Finance

• Work on direct development of capital markets

• Development of the Nigeria Bond Market through Technical Assistance

• Maintain strong collaboration with other financial institutions, including

DFIs