UVU Cracking the Mystery of Financial Aid 2010

advertisement

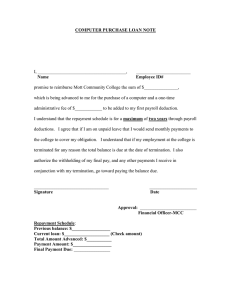

Cracking the Mystery of Financial Aid Eileen Doyle Crane, Utah Valley University Stephen Brown, Fordham University Introduction Financial aid world is highly developed industry Rules and regulations are set by Congress and the U.S. Department of Education Schools have their own policies Many are different; many change as needed Need-based aid versus Merit-based aid Negotiation Topics of Discussion Federal Aid FAFSA Direct Student Loans, subsidized and unsubsidized Perkins Loans Work Study Income-based Repayment Loan Forgiveness Private Educational Lenders Loan Limits Credit Issues Cost of Attendance (COA) Disbursement of Funds Debt Load Salary Data Repayment Issues and Impacts Scholarships and Grants Loan Repayment Assistance Programs (LRAP) FAFSA Free Application for Federal Student Aid Basic federal need analysis document Available on the Web www.fafsa.gov FREE – No cost to student All graduate & professional students are independent Parental info not required for federal aid May be required for high-cost private schools Complete student (and spouse) section ASAP after January 1st FAFSA 1st Step: Apply for a PIN online www.pin.ed.gov/ Collect income, tax, asset information Calculate federal taxes early A PIN number will be emailed to you; save it in a safe place Specify up to 10 schools; check correct codes Student Aid Report (SAR) data will be posted on your FAFSA account; check for accuracy; correct as needed If applying to more than ten law schools, add new schools above the ten initial listed after your SAR posted Federal Aid Programs Federal Direct Stafford Loans: Subsidized and Unsubsidized Federal Direct Grad Plus Loan Program Federal Perkins Loans Federal Work Study Federal Loan Consolidation Federal Stafford Loans Total of $20,500 per year Interest rate fixed at 6.8% 6-Month grace period after enrollment ends 1/2% origination/ 0% guarantee fees If you fail to make first 12 payments on time, origination fee goes up to 1% Stafford Loans Subsidized Taxpayers pays interest while student in school Maximum of $8,500 per year Unsubsidized Interest accrues while student in school Maximum of $20,500 less Subsidized Stafford Perkins Loans Federally guaranteed Campus Based May not be offered by all schools 5% fixed interest 9-month grace period Maximum $6,000 annually Federal Work Study Campus-based program Some law schools do not offer this in the first year of law school Hourly wage for work Need-based program On campus or off campus sites Minimum wage or higher Cost of Attendance Each law school prepares a budget for single students Budget includes: tuition and fees, books, room and board, transportation, insurance, child care (some, not all), and personal needs Financial aid administrators may alter budget for unusual situations Creating a relationship with FA administrators to understand your particular situation is always good; they are happy to meet with students Federal Grad Plus Loans All loan programs are built on the back of the Stafford Loans—up $20,500 available per year Grad Plus Loans--difference between COA and the portion of the $20,500; no cap on borrowing Loans will only be given up to COA; if you need more money, it must come from other sources Terms: 7.9% interest 2 ½ % origination fee Interest accrues while student in school Absence of bad credit required Absence of Bad Credit No account currently 90 days past-due Any account included in this No write-offs, charge-offs, bankruptcies, or foreclosures allowed More detail: www.studentloans.ed.gov Private Loans Schools are required to encourage students to borrow through federal program Credit- based Signature- no collateral Market rate interest - no cap Variable interest rate Guarantee fees Co-Signor options/requirements Capitalization may be monthly, quarterly Pay monthly in order to avoid capitalization Credit Is an important issue in law school finance for public and private schools If your credit is bad, you may not be able to borrow GradPlus or private loans If you need GradPlus or private loans for graduate school and have bad credit You may not be able to attend!! Nationally, 15-20% rejection rate for bad credit Likely to increase! Credit Issues Consumer Debt Credit Bureaus and what they do You are entitled to one free credit report per year; get it early in case there are issues to address Credit Scoring If possible, consider borrowing only for tuition, fees, and books Credit Reporting Agencies Experian www.experian.com Trans Union www.transunion.com Equifax www.equifax.com Annual credit report www.annualcreditreport.com Disbursement of Funds Two times per year at beginning of semester after schools subtract tuition You receive the money AFTER you have moved to graduate school Must live within COA and loan amounts Graduate Student Borrowing Graduate Education Debt All Education Debt Graduate & Professional Degrees % Borrowing Cumulative Debt % Borrowing Cumulative Debt Total 60.1% $37,067 70.1% $42,406 Master’s 58.4% $26,895 69.3% $32,858 Doctoral 51.0% $49,007 58.3% $53,405 Professional 86.5% $82,688 88.4% $93,134 MBA 53.0% $35,525 63.6% $41,687 MSW 76.5% $37,136 81.0% $37,029 PhD 40.0% $36,917 46.8% $41,540 EdD 53.4% $49,050 65.7% $47,725 Law 87.7% $70,933 89.7% $80,754 Medicine 95.0% $113,661 95.0% $125,819 http://www.finaid.org/loans / Physician Salary Data Type of Practice Lowest Reported Mean Reported Highest Reported Family Practice $128,000 $204,000 $299,000 Internal Medicine $154,000 $176,000 $245,000 Cardiologist $268,000 $403,000 $811,000 General Surgeon $226,000 $291,000 $520,000 http://www.studentdoc.com/salaries.html Legal Salary Data Median Hourly $51.97 Mean Hourly $57.40 Mean Annual $119,390 Hourly Wage 10% $24.32 25% $33.61 50% $49.26 75% >$70 90% >$70 25% $69,910 50% $102,470 75% >$145,600 90% >$145,600 Annual Wage 10% $50,580 Department of Labor, Bureau of Labor Statistics www.bls.gov Average MBA Starting Salaries by School Ranking Business School Applicants Accepted Median Total Pay Package 1 Harvard 15% 130,000 2 Stanford 10% 130,00 3 Penn 19% 145,000 4 MIT 20% 113,500 5 Northwestern 24% 133,000 6 Chicago NA 136,000 7 Dartmouth 20% 109,000 8 UC Berkeley 17% 118,000 9 Columbia 17% 144,000 10 NYU 20% 128,000 11 Michigan 28% 104,000 12 Duke 37% 114,000 13 Virginia 41% 121,000 14 Cornell 36% 117,000 15 Yale 22% 115,00 http://www.admissionsconsultants.com/mba/compensation.asp Repayment Details Repayment begins 6 months after graduation Equation-- $12 X $1,000 (6.8%/7.9% interest) = Payment Current average indebtedness– Law $ 100,000 Medicine $ 139, 517 Business $ 35,525 Repayment for $100K= $144,000; Monthly payment $1200 Ten-year standard (can go to 20 or IBR) repayment time frame No penalties for early payoff Repayment Impacts Debt #1 impact on job choice Lifestyle choices: before, during, & after law school 2006 Study: 55% of graduates in repayment report feeling burdened by their debt, especially law graduates Up from 50% in 1997 54% report that they would have borrowed less had they known the extent of the burden 15% report that the benefits of borrowing were out-weighed by the burden of repayment IBR Repayment Impacts How much will this really cost? Can I afford it? Repayment options/incentives 10-, 15-, 20-, 25-, and 30-year repayment plans may be available Be careful of stretching it out: when you should be preparing for retirement, you may still be paying off your college debt AND you may have children in college Debt Management Software Access Group Advisor 1-800-282-1550 www.accessgroup.org Nellie Mae EDvisor 1-800-EDU-LOAN www.nelliemae.org Scholarships Information School Catalogues—Institutional scholarships www.fastweb.com www.finaid.org LRAP Loan Repayment Assistance Programs Awarded post-graduation To grads who work in public interest jobs, as defined by their school May be given as a grant or a loan Loan may be forgiven, after certain number of years of working in job ____ programs nationally Not available at all schools Law School LRAP Programs Public interest jobs Equal Justice Works—former National Association of Public Interest Law www.equaljusticeworks.org High-cost schools pay all/part of loan payments for certain period Limited funds and job descriptions Be Creative!! If you’re paying on your own, and someone want to help you, let them pay one bill while you’re in school (phone, texts, rent, gas, travel, clothes, etc.) Creative entertainment; Find free things to do! Insurance is a MUST!! One medical event could lead to bankruptcy. Stay on parents’ plan, if possible. Holiday presents: textbooks, phone cards, clothes, necessities