13-Mar-09 PRELIMINARY RESULTS Change (% Under the

advertisement

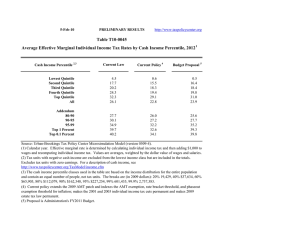

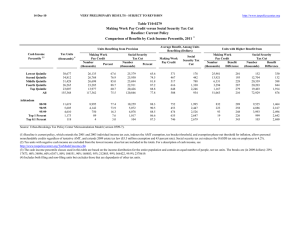

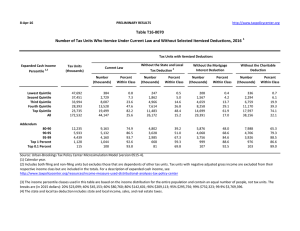

13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups. Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Percentile, 2012 1 Summary Table Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change ($) Average Federal Tax Rate6 Change (% Points) Under the Proposal 78.0 88.8 97.2 99.8 97.1 90.8 0.1 0.2 0.1 0.0 2.9 0.5 5.2 4.7 3.8 4.1 2.8 3.5 6.8 12.8 16.0 23.5 40.7 100.0 -576 -1,208 -1,671 -2,914 -5,718 -2,110 -4.9 -4.1 -3.1 -3.2 -2.0 -2.7 0.8 8.4 15.2 18.1 26.0 20.6 99.9 100.0 96.0 58.6 39.5 0.0 0.0 3.9 41.4 60.5 4.7 4.2 3.0 0.3 0.0 17.8 10.9 10.6 1.4 -0.1 -4,952 -6,251 -7,466 -3,890 2,372 -3.5 -3.2 -2.2 -0.2 0.0 20.8 22.3 25.3 32.6 35.6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). Number of AMT Taxpayers (millions). Baseline: 19.6 Proposal: 3.2 (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $19,957, 40% $37,919, 60% $66,635, 80% $111,847, 90% $160,851, 95% $224,521, 99% $590,626, 99.9% $2,706,134. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law 1 Distribution of Federal Tax Change by Cash Income Percentile, 2012 Detail Table Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Average Federal Tax Change Dollars Percent Share of Federal Taxes Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 78.0 88.8 97.2 99.8 97.1 90.8 0.1 0.2 0.1 0.0 2.9 0.5 5.2 4.7 3.8 4.1 2.8 3.5 6.8 12.8 16.0 23.5 40.7 100.0 -576 -1,208 -1,671 -2,914 -5,718 -2,110 -85.9 -32.7 -16.9 -15.0 -7.3 -11.6 -0.8 -1.1 -0.7 -0.7 3.2 0.0 0.2 3.5 10.3 17.6 68.3 100.0 -4.9 -4.1 -3.1 -3.2 -2.0 -2.7 0.8 8.4 15.2 18.1 26.0 20.6 99.9 100.0 96.0 58.6 39.5 0.0 0.0 3.9 41.4 60.5 4.7 4.2 3.0 0.3 0.0 17.8 10.9 10.6 1.4 -0.1 -4,952 -6,251 -7,466 -3,890 2,372 -14.6 -12.4 -7.9 -0.7 0.1 -0.5 -0.1 0.7 3.1 1.7 13.8 10.1 16.4 28.0 14.2 -3.5 -3.2 -2.2 -0.2 0.0 20.8 22.3 25.3 32.6 35.6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile, 2012 1 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 39,109 35,235 31,797 26,816 23,648 157,316 24.9 22.4 20.2 17.1 15.0 100.0 11,727 29,685 53,843 91,347 279,733 77,851 671 3,696 9,863 19,467 78,501 18,131 11,056 25,988 43,980 71,880 201,232 59,720 5.7 12.5 18.3 21.3 28.1 23.3 3.7 8.5 14.0 20.0 54.0 100.0 4.6 9.8 14.9 20.5 50.7 100.0 0.9 4.6 11.0 18.3 65.1 100.0 11,954 5,808 4,701 1,185 120 7.6 3.7 3.0 0.8 0.1 139,760 197,580 346,049 1,831,745 8,392,568 33,949 50,261 95,151 600,423 2,984,078 105,810 147,320 250,898 1,231,322 5,408,490 24.3 25.4 27.5 32.8 35.6 13.6 9.4 13.3 17.7 8.2 13.5 9.1 12.6 15.5 6.9 14.2 10.2 15.7 24.9 12.5 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). Number of AMT Taxpayers (millions). Baseline: 19.6 Proposal: 3.2 (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The breaks are (in 2009 dollars): 20% $19,957, 40% $37,919, 60% $66,635, 80% $111,847, 90% $160,851, 95% $224,521, 99% $590,626, 99.9% $2,706,134. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 Detail Table Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Share of Federal Taxes Average Federal Tax Change Dollars Percent Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 81.1 83.7 93.7 99.5 97.6 90.8 0.0 0.3 0.1 0.0 2.3 0.5 7.2 5.2 4.0 3.9 2.8 3.5 7.5 12.1 15.0 22.5 42.8 100.0 -768 -1,239 -1,587 -2,479 -4,689 -2,110 -285.7 -40.8 -19.6 -14.9 -7.2 -11.6 -1.0 -1.1 -0.8 -0.7 3.5 0.0 -0.6 2.3 8.2 17.0 73.1 100.0 -7.0 -4.6 -3.3 -3.1 -2.0 -2.7 -4.6 6.7 13.8 17.8 25.8 20.6 99.9 99.7 97.3 63.7 42.3 0.0 0.0 2.7 36.3 57.7 4.0 3.9 3.1 0.5 0.0 16.9 11.4 12.1 2.3 0.0 -3,678 -4,966 -6,746 -5,438 -748 -12.9 -11.6 -8.4 -1.1 0.0 -0.2 0.0 0.6 3.1 1.7 15.0 11.5 17.5 29.1 14.7 -3.1 -2.9 -2.3 -0.3 0.0 20.8 22.5 25.0 32.3 35.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 20121 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Number (thousands) Percent of Total Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Average Federal Tax Rate6 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 32,338 32,399 31,437 30,153 30,278 157,316 20.6 20.6 20.0 19.2 19.3 100.0 10,962 27,043 47,482 79,882 236,122 77,851 269 3,036 8,118 16,663 65,519 18,131 10,693 24,007 39,364 63,218 170,603 59,720 2.5 11.2 17.1 20.9 27.8 23.3 2.9 7.2 12.2 19.7 58.4 100.0 3.7 8.3 13.2 20.3 55.0 100.0 0.3 3.5 9.0 17.6 69.6 100.0 15,269 7,622 5,955 1,432 142 9.7 4.9 3.8 0.9 0.1 119,425 168,851 296,127 1,589,334 7,406,757 28,486 42,886 80,644 518,082 2,622,066 90,940 125,965 215,483 1,071,252 4,784,692 23.9 25.4 27.2 32.6 35.4 14.9 10.5 14.4 18.6 8.6 14.8 10.2 13.7 16.3 7.2 15.3 11.5 16.8 26.0 13.0 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). Number of AMT Taxpayers (millions). Baseline: 19.6 Proposal: 3.2 (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,636, 40% $25,075, 60% $42,597, 80% $68,949, 90% $98,059, 95% $138,184, 99% $356,154, 99.9% $1,639,811. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Single Tax Units Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Share of Federal Taxes Average Federal Tax Change Dollars Percent Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 76.6 75.1 92.1 99.4 98.4 86.3 0.0 0.4 0.1 0.0 1.3 0.3 4.9 3.2 2.9 2.7 3.5 3.3 7.9 11.6 15.5 18.1 46.9 100.0 -366 -582 -840 -1,224 -3,864 -1,148 -54.2 -23.1 -13.5 -9.7 -8.8 -11.1 -0.8 -0.8 -0.3 0.3 1.6 0.0 0.8 4.8 12.4 20.9 60.9 100.0 -4.5 -2.8 -2.4 -2.1 -2.5 -2.5 3.8 9.4 15.3 19.7 26.2 20.4 99.9 99.2 99.1 70.2 43.8 0.0 0.0 0.9 29.8 56.2 3.6 3.8 4.9 1.8 0.1 14.7 10.3 16.2 5.7 0.2 -2,289 -3,412 -7,279 -12,349 -3,784 -10.6 -10.6 -12.6 -3.3 -0.2 0.1 0.1 -0.2 1.6 1.1 15.5 10.9 14.1 20.5 10.1 -2.7 -2.8 -3.5 -1.2 -0.1 22.5 23.8 24.5 33.7 38.4 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 4 Tax Units 2,3 Cash Income Percentile Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Number (thousands) Percent of Total 16,855 15,642 14,507 11,601 9,540 68,506 24.6 22.8 21.2 16.9 13.9 100.0 8,088 20,751 35,163 57,652 153,955 45,237 676 2,524 6,232 12,607 44,125 10,354 7,413 18,227 28,932 45,045 109,830 34,883 5,053 2,377 1,749 362 31 7.4 3.5 2.6 0.5 0.1 86,100 121,430 207,161 1,058,983 5,306,728 21,636 32,297 57,963 369,316 2,041,697 64,464 89,133 149,198 689,667 3,265,032 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 8.4 12.2 17.7 21.9 28.7 22.9 4.4 10.5 16.5 21.6 47.4 100.0 5.2 11.9 17.6 21.9 43.9 100.0 1.6 5.6 12.8 20.6 59.4 100.0 25.1 26.6 28.0 34.9 38.5 14.0 9.3 11.7 12.4 5.4 13.6 8.9 10.9 10.4 4.3 15.4 10.8 14.3 18.8 9.0 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,636, 40% $25,075, 60% $42,597, 80% $68,949, 90% $98,059, 95% $138,184, 99% $356,154, 99.9% $1,639,811. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Married Tax Units Filing Jointly Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Share of Federal Taxes Average Federal Tax Change Dollars Percent Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 79.0 87.3 93.4 99.6 97.2 93.6 0.0 0.3 0.2 0.0 2.7 0.9 8.9 6.6 4.7 4.5 2.6 3.5 4.1 8.5 13.2 25.6 48.5 100.0 -1,238 -2,021 -2,438 -3,500 -5,264 -3,381 -258.3 -51.5 -24.2 -17.7 -6.9 -10.8 -0.5 -0.8 -0.9 -1.2 3.4 0.0 -0.3 1.0 5.0 14.5 79.8 100.0 -8.6 -5.8 -3.9 -3.6 -1.9 -2.6 -5.3 5.5 12.3 16.7 25.6 21.7 99.9 100.0 96.7 62.0 42.0 0.0 0.0 3.3 38.1 58.0 4.3 4.0 2.7 0.3 0.0 20.3 13.8 12.7 1.7 0.1 -4,570 -5,802 -6,686 -3,382 -2,082 -14.1 -12.0 -7.3 -0.6 -0.1 -0.6 -0.2 0.7 3.4 1.8 15.0 12.2 19.6 33.0 16.4 -3.3 -3.0 -2.0 -0.2 0.0 20.1 22.0 25.1 31.9 34.8 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 4 Tax Units 2,3 Cash Income Percentile Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Number (thousands) Percent of Total 6,836 8,755 11,214 15,212 19,110 61,400 11.1 14.3 18.3 24.8 31.1 100.0 14,389 34,618 62,026 97,768 279,599 128,766 479 3,926 10,077 19,789 76,818 31,308 13,910 30,692 51,949 77,978 202,781 97,458 9,202 4,942 3,955 1,011 102 15.0 8.1 6.4 1.7 0.2 138,970 192,850 337,574 1,756,500 7,937,859 32,431 48,251 91,428 563,203 2,762,543 106,540 144,600 246,146 1,193,297 5,175,316 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 3.3 11.3 16.3 20.2 27.5 24.3 1.2 3.8 8.8 18.8 67.6 100.0 1.6 4.5 9.7 19.8 64.8 100.0 0.2 1.8 5.9 15.7 76.4 100.0 23.3 25.0 27.1 32.1 34.8 16.2 12.1 16.9 22.5 10.2 16.4 11.9 16.3 20.2 8.8 15.5 12.4 18.8 29.6 14.7 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,636, 40% $25,075, 60% $42,597, 80% $68,949, 90% $98,059, 95% $138,184, 99% $356,154, 99.9% $1,639,811. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 1 Detail Table - Head of Household Tax Units Percent of Tax Units4 2,3 Cash Income Percentile With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax 5 Income Share of Total Federal Tax Change Share of Federal Taxes Average Federal Tax Change Dollars Percent Change (% Points) Under the Proposal Average Federal Tax Rate6 Change (% Points) Under the Proposal 91.3 96.4 98.4 99.6 97.7 95.4 0.0 0.1 0.0 0.0 2.0 0.1 8.2 6.0 4.4 3.6 2.1 4.8 24.2 30.8 22.4 14.6 7.9 100.0 -1,205 -1,692 -1,863 -2,226 -2,838 -1,672 158.5 -56.8 -20.4 -13.2 -5.8 -25.3 -9.5 -5.8 1.8 4.5 9.0 0.0 -13.4 7.9 29.5 32.4 43.4 100.0 -8.6 -5.4 -3.6 -2.8 -1.5 -4.0 -14.0 4.1 14.1 18.7 25.0 11.8 99.7 99.1 95.0 57.9 36.4 0.0 0.2 5.0 42.1 63.6 2.8 3.0 1.9 0.1 -0.4 4.4 1.8 1.6 0.1 -0.1 -2,468 -3,524 -3,992 -818 16,670 -8.7 -8.8 -5.7 -0.2 0.7 2.8 1.1 1.9 3.1 1.5 15.6 6.3 9.2 12.4 5.8 -2.1 -2.2 -1.4 -0.1 0.2 22.4 23.1 23.8 32.5 35.5 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 2012 1 4 Tax Units 2,3 Cash Income Percentile Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average After5 Tax Income (Dollars) Number (thousands) Percent of Total 8,355 7,578 5,002 2,726 1,153 24,862 33.6 30.5 20.1 11.0 4.6 100.0 13,999 31,423 51,564 78,373 184,854 41,756 -760 2,979 9,121 16,860 49,121 6,618 14,759 28,444 42,443 61,512 135,733 35,138 740 211 169 32 3 3.0 0.9 0.7 0.1 0.0 115,411 158,521 280,025 1,444,013 6,993,121 28,300 40,190 70,657 469,766 2,463,279 87,111 118,332 209,368 974,247 4,529,841 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total -5.4 9.5 17.7 21.5 26.6 15.9 11.3 22.9 24.8 20.6 20.5 100.0 14.1 24.7 24.3 19.2 17.9 100.0 -3.9 13.7 27.7 27.9 34.4 100.0 24.5 25.4 25.2 32.5 35.2 8.2 3.2 4.6 4.5 2.0 7.4 2.9 4.1 3.6 1.5 12.7 5.2 7.3 9.3 4.3 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,636, 40% $25,075, 60% $42,597, 80% $68,949, 90% $98,059, 95% $138,184, 99% $356,154, 99.9% $1,639,811. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 Detail Table - Tax Units with Children Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Share of Federal Taxes Average Federal Tax Change Dollars Percent Change (% Points) Average Federal Tax Rate 6 Under the Proposal Change (% Points) Under the Proposal 94.6 99.4 99.8 100.0 96.0 98.0 0.0 0.1 0.0 0.0 4.0 0.7 9.9 7.8 5.5 5.4 2.4 4.4 10.8 16.4 18.7 26.8 27.2 100.0 -1,590 -2,476 -2,864 -4,400 -5,497 -3,218 170.0 -66.2 -24.4 -18.7 -6.0 -14.5 -2.0 -2.2 -1.3 -1.0 6.5 0.0 -2.9 1.4 9.8 19.7 71.9 100.0 -10.5 -6.9 -4.5 -4.2 -1.7 -3.4 -16.7 3.6 13.9 18.1 27.1 20.0 100.0 100.0 92.2 47.6 30.1 0.0 0.0 7.7 52.4 70.0 4.5 4.1 2.0 -0.1 -0.3 14.0 8.2 5.5 -0.4 -0.4 -5,456 -6,871 -5,691 1,695 17,665 -13.5 -11.6 -5.0 0.2 0.5 0.2 0.4 1.8 4.2 2.0 15.1 10.6 17.7 28.5 13.7 -3.4 -3.0 -1.4 0.1 0.2 21.7 23.1 27.0 33.9 35.9 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 20121 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 10,815 10,484 10,353 9,644 7,855 49,293 21.9 21.3 21.0 19.6 15.9 100.0 15,090 35,679 64,150 105,690 316,419 95,214 -935 3,741 11,754 23,563 91,377 22,259 16,025 31,938 52,396 82,128 225,042 72,956 4,070 1,884 1,523 378 37 8.3 3.8 3.1 0.8 0.1 160,563 227,342 403,939 2,087,355 9,762,184 40,340 59,433 114,831 706,123 3,484,212 120,224 167,909 289,108 1,381,233 6,277,972 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total -6.2 10.5 18.3 22.3 28.9 23.4 3.5 8.0 14.2 21.7 53.0 100.0 4.8 9.3 15.1 22.0 49.2 100.0 -0.9 3.6 11.1 20.7 65.4 100.0 25.1 26.1 28.4 33.8 35.7 13.9 9.1 13.1 16.8 7.6 13.6 8.8 12.2 14.5 6.4 15.0 10.2 15.9 24.3 11.7 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,636, 40% $25,075, 60% $42,597, 80% $68,949, 90% $98,059, 95% $138,184, 99% $356,154, 99.9% $1,639,811. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 13-Mar-09 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T09-0136 Administration's Fiscal Year 2010 Budget Proposals Major Individual Income Tax Provisions, Maintain Estate Tax at 2009 Parameters, Major Corporate Tax Provisions Baseline: Current Law 1 Distribution of Federal Tax Change by Cash Income Percentile Adjusted for Family Size, 2012 Detail Table - Elderly Tax Units Percent of Tax Units4 Cash Income Percentile2,3 With Tax Cut Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All With Tax Increase Percent Change in After-Tax Income5 Share of Total Federal Tax Change Share of Federal Taxes Average Federal Tax Change Dollars Percent Change (% Points) Under the Proposal Average Federal Tax Rate 6 Change (% Points) Under the Proposal 42.8 50.1 72.0 98.4 98.0 73.9 0.0 0.1 0.1 0.1 1.7 0.5 1.4 1.2 1.2 2.6 3.6 3.0 1.0 3.4 4.3 15.9 75.3 100.0 -150 -276 -484 -1,691 -6,252 -2,021 -38.8 -25.4 -20.5 -17.6 -10.4 -11.7 -0.1 -0.2 -0.2 -0.7 1.3 0.0 0.2 1.3 2.2 9.9 86.3 100.0 -1.4 -1.2 -1.2 -2.3 -2.7 -2.4 2.2 3.5 4.6 10.7 23.3 17.9 99.6 99.5 98.9 75.4 53.1 0.0 0.1 1.1 24.6 46.9 4.1 4.6 5.0 1.7 0.5 20.5 16.5 27.1 11.3 1.5 -3,653 -5,532 -9,858 -15,880 -22,582 -18.0 -16.3 -14.4 -3.5 -1.0 -1.0 -0.6 -0.7 3.5 2.3 12.4 11.3 21.3 41.5 21.1 -3.3 -3.6 -3.7 -1.1 -0.4 15.2 18.4 21.9 31.7 35.7 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Baseline Distribution of Income and Federal Taxes by Cash Income Percentile Adjusted for Family Size, 20121 Tax Units4 Cash Income Percentile2,3 Lowest Quintile Second Quintile Middle Quintile Fourth Quintile Top Quintile All Average Income (Dollars) Average Federal Tax Burden (Dollars) Average AfterTax Income5 (Dollars) Number (thousands) Percent of Total 4,167 7,540 5,432 5,756 7,378 30,291 13.8 24.9 17.9 19.0 24.4 100.0 10,783 23,370 41,368 74,513 232,411 85,420 385 1,088 2,367 9,633 60,422 17,306 10,398 22,282 39,001 64,880 171,990 68,114 3,435 1,827 1,681 434 42 11.3 6.0 5.6 1.4 0.1 109,456 155,369 267,378 1,393,711 6,524,092 20,315 34,044 68,371 457,846 2,348,994 89,141 121,324 199,006 935,864 4,175,097 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 3.6 4.7 5.7 12.9 26.0 20.3 1.7 6.8 8.7 16.6 66.3 100.0 2.1 8.1 10.3 18.1 61.5 100.0 0.3 1.6 2.5 10.6 85.0 100.0 18.6 21.9 25.6 32.9 36.0 14.5 11.0 17.4 23.4 10.6 14.8 10.7 16.2 19.7 8.5 13.3 11.9 21.9 37.9 18.8 Average Federal Tax Rate6 Addendum 80-90 90-95 95-99 Top 1 Percent Top 0.1 Percent Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0309-1). Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current law. Proposal extends the Making Work Pay Credit, the Earned Income Tax Credit expansion; the Saver's credit expansion; creates automatic 401(k)s and IRAs; and extends the American Opportunity Tax Credit; reinstates the 36 percent and 39.6 percent rates; reinstates the personal exemption phaseout and limitation on itemized deductions for those taxpayers with AGI over $250,000 (married) and $200,000 (single); imposes a 20 percent rate on capital gains and qualified dividends for those taxpayers with AGI over $250,000 (married) and $200,000 (single); and limits the tax rate at which itemized deductions reduce tax liability to 28 percent. The estate tax is maintained at its 2009 parameters. Corporate income tax measures included were making the research and experimentation tax credit permanent; expanding net operating loss carryback, taxing carried interest as ordinary income, repealing LIFO, and implementing international enforcement, reform deferral and other reform policies. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) The cash income percentile classes used in this table are based on the income distribution for the entire population and contain an equal number of people, not tax units. The incomes used are adjusted for family size by dividing by the square root of the number of people in the tax unit. The resulting percentile breaks are (in 2009 dollars): 20% $13,636, 40% $25,075, 60% $42,597, 80% $68,949, 90% $98,059, 95% $138,184, 99% $356,154, 99.9% $1,639,811. (4) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (5) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (6) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.