Schroders Outlook 2015: European Equities

advertisement

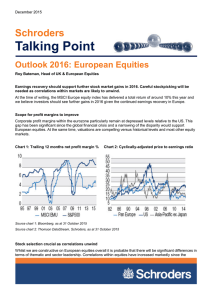

Schroders Outlook 2015: European Equities By Rory Bateman, Head of UK and European Equities November 2014 Monetary policy remains loose and QE remains a possibility in the coming months, but governments need to do more to stimulate aggregate demand Corporate profitability should improve given the stable economic environment with exporters benefiting from a weaker euro European equities remain attractively valued versus their own history, as well as compared to other regions and asset classes Europe’s economic recovery has been unpredictable during 2014. It has been our view for some time that the recovery would be protracted and uneven, and the recent data has done little to contradict us. The sluggish macro environment does not mean all is doom and gloom in terms of the outlook for European equities; on the contrary, we see equity market weakness as a buying opportunity. Firstly, there are still measures the authorities can take to strengthen the economic recovery, and secondly there are several other factors with the potential to support eurozone equities over the coming year. ECB actions are helping but governments also have a part to play The main concern facing Europe is that low levels of inflation may turn into deflation. This is not a new issue and we do not believe that the probability of deflation is high. The European Central Bank (ECB) has already taken significant steps to ease credit conditions and boost growth in the eurozone. Some of these measures – such as the purchases of asset backed securities - are only just being implemented so their full impact is yet to be felt. Moreover, we see a high probability that full-scale quantitative easing (QE) could be introduced if deflationary worries in Europe persist. Each of the three QE programmes in the US sparked a period of strong upward momentum for the US equity market and we would expect the response in Europe to be similarly positive for share prices. That said, ECB President Mario Draghi has made the point on a number of occasions that the central bank cannot do all the heavy lifting on its own. In order to create a sustained economic recovery in Europe, the ECB also needs governments to take appropriate fiscal measures in conjunction with structural reforms in order to stimulate aggregate demand. 1 2 In our view, Germany’s insistence on balanced budgets is laudable but a more flexible approach is needed to respond to the reality of the economic cycle. Stage is set for corporate earnings to improve Another factor that offers a significant opportunity is the scope for earnings improvement in Europe. Profit margins for eurozone businesses still lag far behind their US counterparts and closing the gap could help deliver sizeable share price upside. As well as an improved backdrop in terms of credit conditions, there are other factors that could provide a catalyst for an improvement in profits. 12 months forwards earnings per share € $ 40 0 20 MSCI EMU (LHS) Jun 12 5 Jun 09 60 Jun 06 10 Jun 03 80 Jun 00 15 Jun 97 100 Jun 94 20 Jun 91 120 Jun 88 25 MSCI US (RHS) Source: Datastream, 30 September 2014 One of the most obvious results so far of the ECB’s looser monetary policy has been the weakening of the euro. The strength of the currency was a major headwind for eurozone equities, particularly exporters, in the early part of 2014. That headwind has now eased and the currency is likely to weaken further, especially with the US Federal Reserve poised to raise interest rates next year. The weaker euro should be a source of positive earnings momentum in 2015. Banks offer strong recovery potential The banking sector is one important area where we see the potential for significant improvement in terms of profits. Banks have been subject to myriad pressures, most notably with regard to potential recapitalisations. The ECB’s recently-concluded Asset Quality Review has demonstrated that the worst is over from that respect and banks should now have the confidence to return to lending. We would expect European banks to emulate the recovery already seen in the profitability of US banks. As lending growth picks up, our forecasts indicate that banking profitability will escalate quite substantially over the coming three to five years, leading in turn to a significant positive impact on net income. 3 European banks net income € billion 2007-2017e 140 120 100 80 60 40 20 0 -20 -40 -60 2007 2008 UK 2009 Nordic 2010 France 2011 2012 Germany 2013 Switzerland 2014e 2015e Spain and Italy 2016e 2017e Other Source: Schroders estimates, top 29 listed European banks, as of August 2014 Europe remains attractively valued There is also the impact that fund flows could have in the eurozone. While flows have improved since the nadir of the eurozone crisis, we are still some 40% off the levels reached during 2001-07 so there is still a substantial amount of money on the side-lines that could potentially make its way back into European equities. Moreover, we believe that current valuation levels would tend to suggest that European equities remain an attractive area in which to invest. The pan-European market trades on a cyclically-adjusted price-to-earnings ratio of around 16x, compared to the 30year average of 20.8x and to the US market on around 27x. We feel that represents a very compelling opportunity. Important Information: Important Information: The views and opinions contained herein are those of Rory Bateman, Head of UK and European Equities, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. No responsibility can be accepted for errors of fact or opinion. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results, prices of shares and the income from them may fall as well as rise and investors may not get back the amount originally invested. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA, which is authorised and regulated by the Financial Conduct Authority. For your security, communications may be taped or monitored. Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data provider's consent. Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the third party data. The Prospectus and/or www.schroders.com contains additional disclaimers which apply to the third party data.