8-Feb-10 PRELIMINARY RESULTS Less than 10 10-20

advertisement

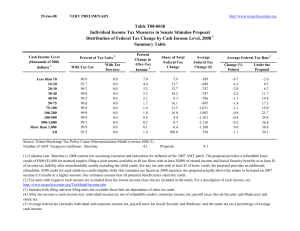

8-Feb-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Click on PDF or Excel link above for additional tables containing more detail and breakdowns by filing status and demographic groups. Table T10-0032 Administration's FY2011 Budget Proposals Major Individual Income and Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Level, 2012 Summary Table Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut 25.3 57.6 78.5 87.8 91.7 96.7 98.7 99.1 97.5 66.0 38.1 79.0 With Tax Increase 10.1 9.4 8.9 6.6 5.2 2.3 0.9 0.8 2.5 34.0 61.9 6.0 Percent Change in After-Tax Income 4 2.5 2.6 3.3 3.2 3.0 2.9 3.3 4.0 3.3 0.7 -0.8 2.7 1 Share of Total Federal Tax Change Average Federal Tax Change ($) 0.9 3.7 6.5 6.3 5.9 13.4 13.4 35.1 16.9 1.5 -3.6 100.0 -136 -381 -765 -984 -1,143 -1,483 -2,330 -4,268 -7,164 -3,676 17,181 -1,594 Average Federal Tax Rate5 Change (% Points) -2.4 -2.5 -3.0 -2.7 -2.5 -2.3 -2.6 -3.0 -2.4 -0.5 0.6 -2.1 Under the Proposal 3.0 2.8 7.7 12.1 14.8 17.1 19.0 21.6 24.9 28.0 34.4 21.3 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-4. Number of AMT Taxpayers (millions). Baseline: 19.5 Proposal: 4.0 (1) Calendar year. Baseline is current law. The proposal would: (a) extend the higher EITC credit value for families with 3 children and higher phase-out thresholds for married couples and allow it against the AMT; (b) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (c) create automatic 401(k)s and IRAs; (d) extend the American Opportunity Tax Credit; (e) extend child tax credit refundability with a $3,000 refundability threshold, extend the $1,000 credit, and allow against the AMT; (f) extend the higher 35 percent child and dependent care tax credit rate, raise the phase-out threshold to $85,000, and allow against the AMT; (g) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (h) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (i) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (j) limit value of itemized deduction s to 28 percent; (k) maintain the estate tax at its 2009 parameters; (l) extend the 2001 and 2003 tax cuts for low and middle income individuals including marriage penalty relief, the 10,15, 25, 28 percent brackets, the 15 percent rate on capital gains and qualified dividends for taxpayers in those brackets. Business provisions included were making the research and experimentation tax credit permanent, taxing carried interest as ordinary income, repealing LIFO, international corporate tax reforms, and reforms affecting the tax treatment of financial institutions. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 8-Feb-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0032 Administration's FY2011 Budget Proposals Major Individual Income and Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table Cash Income Level (thousands of 2009 2 dollars) Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut With Tax Increase 25.3 57.6 78.5 87.8 91.7 96.7 98.7 99.1 97.5 66.0 38.1 79.0 10.1 9.4 8.9 6.6 5.2 2.3 0.9 0.8 2.5 34.0 61.9 6.0 Percent Change in After-Tax 4 Income 2.5 2.6 3.3 3.2 3.0 2.9 3.3 4.0 3.3 0.7 -0.8 2.7 Share of Total Federal Tax Change 0.9 3.7 6.5 6.3 5.9 13.4 13.4 35.1 16.9 1.5 -3.6 100.0 Average Federal Tax Change Dollars Percent -136 -381 -765 -984 -1,143 -1,483 -2,330 -4,268 -7,164 -3,676 17,181 -1,594 -44.1 -46.4 -27.8 -18.4 -14.2 -11.9 -12.0 -12.3 -8.9 -1.8 1.6 -8.9 Share of Federal Taxes Change (% Points) -0.1 -0.3 -0.4 -0.3 -0.2 -0.3 -0.3 -0.9 0.0 0.6 2.3 0.0 Under the Proposal 0.1 0.4 1.7 2.8 3.5 9.8 9.7 24.6 17.1 8.1 22.3 100.0 Average Federal Tax Rate Change (% Points) -2.4 -2.5 -3.0 -2.7 -2.5 -2.3 -2.6 -3.0 -2.4 -0.5 0.6 -2.1 5 Under the Proposal 3.0 2.8 7.7 12.1 14.8 17.1 19.0 21.6 24.9 28.0 34.4 21.3 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) 16,958 24,305 21,133 16,074 12,909 22,702 14,431 20,606 5,930 1,048 531 157,348 Percent of Total 10.8 15.5 13.4 10.2 8.2 14.4 9.2 13.1 3.8 0.7 0.3 100.0 Average Income (Dollars) 5,723 15,533 25,808 36,190 46,615 64,099 90,195 141,257 296,062 704,969 3,114,004 76,169 Average Federal Tax Burden (Dollars) 309 822 2,757 5,357 8,055 12,465 19,425 34,702 80,820 201,075 1,053,607 17,826 Average After4 Tax Income (Dollars) 5,414 14,711 23,051 30,832 38,560 51,634 70,770 106,555 215,243 503,895 2,060,398 58,343 Average Federal Tax Rate 5 5.4 5.3 10.7 14.8 17.3 19.5 21.5 24.6 27.3 28.5 33.8 23.4 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 0.8 3.2 4.6 4.9 5.0 12.1 10.9 24.3 14.7 6.2 13.8 100.0 1.0 3.9 5.3 5.4 5.4 12.8 11.1 23.9 13.9 5.8 11.9 100.0 0.2 0.7 2.1 3.1 3.7 10.1 10.0 25.5 17.1 7.5 19.9 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-4). Number of AMT Taxpayers (millions). Baseline: 19.5 Proposal: 4.0 (1) Calendar year. Baseline is current law. The proposal would: (a) extend the higher EITC credit value for families with 3 children and higher phase-out thresholds for married couples and allow it against the AMT; (b) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (c) create automatic 401(k)s and IRAs; (d) extend the American Opportunity Tax Credit; (e) extend child tax credit refundability with a $3,000 refundability threshold, extend the $1,000 credit, and allow against the AMT; (f) extend the higher 35 percent child and dependent care tax credit rate, raise the phase-out threshold to $85,0 and allow against the AMT; (g) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (h) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (i) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (j) limit value of itemized deduction s to 28 percent; (k) maintain the estate tax at its 2009 parameters; (l) extend the 2001 and 2003 tax cuts for low and middle income individuals including marriage penalty relief, the 10,15, 25, 28 percent brackets, the 15 percent rate on capital gains and qualified dividends for taxpayers in those brackets. Business provisions included were making the research and experimentation tax credit permanent, taxing carried interest as ordinary income, repealing LIFO, international corporate tax reforms, and reforms affecting the tax treatment of financial institutions. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 8-Feb-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0032 Administration's FY2011 Budget Proposals Major Individual Income and Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Single Tax Units Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut With Tax Increase 18.4 54.9 76.0 91.3 96.5 97.9 98.1 97.6 91.9 55.6 36.2 69.5 10.0 10.3 11.1 5.2 2.7 1.5 1.5 1.9 8.0 44.4 63.8 7.4 Percent Change in After-Tax Income 4 1.7 1.5 2.1 1.9 1.9 2.2 2.9 3.7 4.1 2.1 -0.6 2.3 Share of Total Federal Tax Change 2.0 5.9 9.5 7.9 7.9 17.0 12.8 23.2 12.8 2.6 -1.6 100.0 Average Federal Tax Change Dollars Percent -87 -214 -459 -566 -715 -1,054 -1,930 -3,723 -8,805 -10,197 11,797 -787 -18.0 -15.4 -12.3 -8.5 -7.5 -7.3 -8.4 -10.0 -10.1 -4.6 1.1 -7.8 Share of Federal Taxes Change (% Points) -0.1 -0.3 -0.3 -0.1 0.0 0.1 -0.1 -0.4 -0.3 0.2 1.1 0.0 Under the Proposal 0.8 2.7 5.7 7.2 8.3 18.5 11.8 17.7 9.6 4.5 12.9 100.0 Average Federal Tax Rate5 Change (% Points) -1.5 -1.4 -1.8 -1.6 -1.5 -1.7 -2.2 -2.7 -2.9 -1.5 0.4 -1.8 Under the Proposal 7.0 7.7 12.7 16.9 18.9 21.3 23.6 24.4 26.0 30.2 37.1 21.1 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 12,161 14,889 11,204 7,555 6,018 8,766 3,599 3,384 787 138 75 68,932 17.6 21.6 16.3 11.0 8.7 12.7 5.2 4.9 1.1 0.2 0.1 100.0 Average Income (Dollars) 5,710 15,384 25,667 36,120 46,555 63,234 89,193 137,406 300,163 697,814 2,972,435 43,878 Average Federal Tax Burden (Dollars) 484 1,391 3,718 6,658 9,528 14,546 22,933 37,216 86,955 220,611 1,090,072 10,053 Average AfterTax Income 4 (Dollars) 5,227 13,993 21,949 29,462 37,027 48,688 66,260 100,190 213,208 477,203 1,882,363 33,825 Average Federal Tax Rate 5 8.5 9.0 14.5 18.4 20.5 23.0 25.7 27.1 29.0 31.6 36.7 22.9 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 2.3 7.6 9.5 9.0 9.3 18.3 10.6 15.4 7.8 3.2 7.3 100.0 2.7 8.9 10.6 9.6 9.6 18.3 10.2 14.5 7.2 2.8 6.0 100.0 0.9 3.0 6.0 7.3 8.3 18.4 11.9 18.2 9.9 4.4 11.8 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-4). (1) Calendar year. Baseline is current law. The proposal would: (a) extend the higher EITC credit value for families with 3 children and higher phase-out thresholds for married couples and allow it against the AMT; (b) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (c) create automatic 401(k)s and IRAs; (d) extend the American Opportunity Tax Credit; (e) extend child tax credit refundability with a $3,000 refundability threshold, extend the $1,000 credit, and allow against the AMT; (f) extend the higher 35 percent child and dependent care tax credit rate, raise the phase-out threshold to $85,000, and allow against the AMT; (g) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (h) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (i) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (j) limit value of itemized deduction s to 28 percent; (k) maintain the estate tax at its 2009 parameters; (l) extend the 2001 and 2003 tax cuts for low and middle income individuals including marriage penalty relief, the 10,15, 25, 28 percent brackets, the 15 percent rate on capital gains and qualified dividends for taxpayers in those brackets. Business provisions included were making the research and experimentation tax credit permanent, taxing carried interest as ordinary income, repealing LIFO, international corporate tax reforms, and reforms affecting the tax treatment of financial institutions. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 8-Feb-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0032 Administration's FY2011 Budget Proposals Major Individual Income and Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Married Tax Units Filing Jointly Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut With Tax Increase 22.1 44.6 68.8 72.8 80.4 94.8 98.9 99.4 98.6 68.2 38.7 85.4 17.5 15.5 10.7 14.1 11.6 3.7 0.8 0.6 1.4 31.8 61.3 6.3 Percent Change in After-Tax Income 4 2.9 2.7 4.1 4.0 3.7 3.1 3.4 4.1 3.3 0.6 -0.8 2.7 Share of Total Federal Tax Change 0.2 1.1 3.0 3.6 3.9 10.5 14.0 45.1 21.7 1.5 -4.6 100.0 Average Federal Tax Change Dollars Percent -129 -419 -996 -1,317 -1,506 -1,694 -2,442 -4,459 -7,020 -2,803 16,725 -2,607 -51.5 -76.0 -55.4 -36.0 -25.5 -16.1 -13.7 -13.0 -8.8 -1.4 1.6 -8.5 Share of Federal Taxes Change (% Points) 0.0 -0.1 -0.2 -0.3 -0.2 -0.5 -0.5 -1.5 -0.1 0.7 2.6 0.0 Under the Proposal 0.0 0.0 0.2 0.6 1.0 5.0 8.1 27.9 20.8 9.9 26.2 100.0 Average Federal Tax Rate5 Change (% Points) -2.7 -2.6 -3.8 -3.6 -3.2 -2.6 -2.7 -3.1 -2.4 -0.4 0.5 -2.1 Under the Proposal 2.6 0.8 3.1 6.5 9.4 13.5 16.9 20.9 24.7 27.7 33.9 22.4 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,172 4,097 4,842 4,391 4,095 9,883 9,149 16,193 4,941 876 435 61,357 3.5 6.7 7.9 7.2 6.7 16.1 14.9 26.4 8.1 1.4 0.7 100.0 Average Income (Dollars) 4,766 16,031 25,959 36,302 46,760 65,241 90,792 142,545 295,420 706,519 3,075,014 126,020 Average Federal Tax Burden (Dollars) 251 552 1,798 3,662 5,916 10,508 17,815 34,223 79,908 198,277 1,025,157 30,803 Average AfterTax Income 4 (Dollars) 4,515 15,479 24,161 32,640 40,844 54,734 72,977 108,322 215,512 508,242 2,049,857 95,217 Average Federal Tax Rate 5 5.3 3.4 6.9 10.1 12.7 16.1 19.6 24.0 27.1 28.1 33.3 24.4 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 0.1 0.9 1.6 2.1 2.5 8.3 10.7 29.9 18.9 8.0 17.3 100.0 0.2 1.1 2.0 2.5 2.9 9.3 11.4 30.0 18.2 7.6 15.3 100.0 0.0 0.1 0.5 0.9 1.3 5.5 8.6 29.3 20.9 9.2 23.6 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-4). (1) Calendar year. Baseline is current law. The proposal would: (a) extend the higher EITC credit value for families with 3 children and higher phase-out thresholds for married couples and allow it against the AMT; (b) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (c) create automatic 401(k)s and IRAs; (d) extend the American Opportunity Tax Credit; (e) extend child tax credit refundability with a $3,000 refundability threshold, extend the $1,000 credit, and allow against the AMT; (f) extend the higher 35 percent child and dependent care tax credit rate, raise the phase-out threshold to $85,000, and allow against the AMT; (g) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (h) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (i) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (j) limit value of itemized deduction s to 28 percent; (k) maintain the estate tax at its 2009 parameters; (l) extend the 2001 and 2003 tax cuts for low and middle income individuals including marriage penalty relief, the 10,15, 25, 28 percent brackets, the 15 percent rate on capital gains and qualified dividends for taxpayers in those brackets. Business provisions included were making the research and experimentation tax credit permanent, taxing carried interest as ordinary income, repealing LIFO, international corporate tax reforms, and reforms affecting the tax treatment of financial institutions. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 8-Feb-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0032 Administration's FY2011 Budget Proposals Major Individual Income and Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Head of Household Tax Units Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut With Tax Increase 61.9 74.9 93.1 97.2 97.8 99.3 99.1 99.4 94.4 59.6 32.5 88.6 4.1 2.1 2.1 1.3 1.0 0.4 0.5 0.4 5.6 40.4 67.5 1.8 Percent Change in After-Tax Income 4 5.4 5.2 5.1 4.6 4.0 3.7 3.8 3.0 2.1 0.2 -1.1 4.0 Share of Total Federal Tax Change 2.9 12.5 17.6 16.1 11.3 19.7 10.8 7.7 2.0 0.1 -0.7 100.0 Average Federal Tax Change Dollars Percent -390 -844 -1,259 -1,450 -1,569 -1,881 -2,628 -2,975 -4,553 -1,140 20,875 -1,384 75.8 114.0 -95.7 -32.1 -20.4 -15.2 -13.0 -8.9 -6.0 -0.6 2.1 -20.5 Share of Federal Taxes Change (% Points) -0.9 -3.8 -3.6 -1.5 0.0 1.8 1.6 2.6 1.3 0.7 1.9 0.0 Under the Proposal -1.7 -6.1 0.2 8.8 11.4 28.4 18.6 20.2 8.2 3.3 8.6 100.0 Average Federal Tax Rate5 Change (% Points) -5.9 -5.4 -4.9 -4.0 -3.4 -3.0 -3.0 -2.2 -1.6 -0.2 0.7 -3.3 Under the Proposal -13.6 -10.2 0.2 8.5 13.2 16.6 19.8 22.8 24.3 26.5 34.9 12.8 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,483 5,029 4,757 3,767 2,449 3,559 1,389 877 150 24 11 24,547 10.1 20.5 19.4 15.4 10.0 14.5 5.7 3.6 0.6 0.1 0.0 100.0 Average Income (Dollars) 6,647 15,579 25,971 36,157 46,569 63,082 89,214 132,993 294,130 686,382 2,985,055 41,760 Average Federal Tax Burden (Dollars) -514 -740 1,316 4,516 7,696 12,367 20,260 33,272 75,988 183,071 1,019,602 6,738 Average AfterTax Income 4 (Dollars) 7,161 16,319 24,655 31,641 38,873 50,716 68,953 99,721 218,142 503,311 1,965,454 35,022 Average Federal Tax Rate 5 -7.7 -4.8 5.1 12.5 16.5 19.6 22.7 25.0 25.8 26.7 34.2 16.1 Share of PreTax Income Share of PostTax Income Share of Federal Taxes Percent of Total Percent of Total Percent of Total 1.6 7.6 12.1 13.3 11.1 21.9 12.1 11.4 4.3 1.6 3.2 100.0 2.1 9.6 13.6 13.9 11.1 21.0 11.1 10.2 3.8 1.4 2.5 100.0 -0.8 -2.3 3.8 10.3 11.4 26.6 17.0 17.7 6.9 2.6 6.7 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-4). (1) Calendar year. Baseline is current law. The proposal would: (a) extend the higher EITC credit value for families with 3 children and higher phase-out thresholds for married couples and allow it against the AMT; (b) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (c) create automatic 401(k)s and IRAs; (d) extend the American Opportunity Tax Credit; (e) extend child tax credit refundability with a $3,000 refundability threshold, extend the $1,000 credit, and allow against the AMT; (f) extend the higher 35 percent child and dependent care tax credit rate, raise the phase-out threshold to $85,000, and allow against the AMT; (g) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (h) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (i) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (j) limit value of itemized deduction s to 28 percent; (k) maintain the estate tax at its 2009 parameters; (l) extend the 2001 and 2003 tax cuts for low and middle income individuals including marriage penalty relief, the 10,15, 25, 28 percent brackets, the 15 percent rate on capital gains and qualified dividends for taxpayers in those brackets. Business provisions included were making the research and experimentation tax credit permanent, taxing carried interest as ordinary income, repealing LIFO, international corporate tax reforms, and reforms affecting the tax treatment of financial institutions. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 8-Feb-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0032 Administration's FY2011 Budget Proposals Major Individual Income and Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Tax Units with Children Cash Income Level (thousands of 2009 2 dollars) Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut With Tax Increase 64.0 82.5 95.4 98.5 98.5 99.4 99.7 99.8 98.8 65.4 32.3 94.1 1.9 1.8 1.3 0.6 0.7 0.4 0.2 0.2 1.2 34.6 67.7 1.4 Percent Change in After-Tax 4 Income 6.1 6.0 6.8 6.2 5.5 4.4 4.4 4.7 3.3 0.4 -1.1 3.7 Share of Total Federal Tax Change 0.9 4.4 7.3 7.3 6.2 12.9 13.7 35.5 14.5 0.6 -3.3 100.0 Average Federal Tax Change Dollars Percent -422 -1,029 -1,700 -1,974 -2,146 -2,309 -3,133 -5,069 -7,021 -1,931 21,302 -2,710 59.8 79.9 -205.6 -47.8 -29.3 -19.5 -16.4 -14.6 -8.7 -0.9 2.0 -12.0 Share of Federal Taxes Change (% Points) -0.2 -0.7 -0.9 -0.7 -0.5 -0.7 -0.5 -0.9 0.8 1.1 3.2 0.0 Under the Proposal -0.3 -1.3 -0.5 1.1 2.1 7.3 9.6 28.4 21.0 9.4 23.3 100.0 Average Federal Tax Rate Change (% Points) -6.8 -6.5 -6.6 -5.5 -4.6 -3.6 -3.5 -3.6 -2.4 -0.3 0.7 -2.8 5 Under the Proposal -18.0 -14.7 -3.4 6.0 11.1 14.9 17.6 20.8 25.2 29.5 35.4 20.7 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,968 5,639 5,683 4,891 3,849 7,425 5,841 9,319 2,750 441 206 49,155 6.0 11.5 11.6 10.0 7.8 15.1 11.9 19.0 5.6 0.9 0.4 100.0 Average Income (Dollars) 6,252 15,769 25,918 36,161 46,701 64,368 90,740 142,137 293,742 705,334 3,105,769 95,419 Average Federal Tax Burden (Dollars) -706 -1,288 827 4,128 7,328 11,870 19,102 34,691 81,104 210,012 1,077,968 22,496 Average After4 Tax Income (Dollars) 6,958 17,057 25,091 32,033 39,373 52,498 71,638 107,447 212,638 495,322 2,027,801 72,923 Average Federal Tax Rate 5 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total -11.3 -8.2 3.2 11.4 15.7 18.4 21.1 24.4 27.6 29.8 34.7 23.6 0.4 1.9 3.1 3.8 3.8 10.2 11.3 28.2 17.2 6.6 13.7 100.0 0.6 2.7 4.0 4.4 4.2 10.9 11.7 27.9 16.3 6.1 11.7 100.0 -0.2 -0.7 0.4 1.8 2.6 8.0 10.1 29.2 20.2 8.4 20.1 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-4). Note: Tax units with children are those claiming an exemption for children at home or away from home. (1) Calendar year. Baseline is current law. The proposal would: (a) extend the higher EITC credit value for families with 3 children and higher phase-out thresholds for married couples and allow it against the AMT; (b) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (c) create automatic 401(k)s and IRAs; (d) extend the American Opportunity Tax Credit; (e) extend child tax credit refundability with a $3,000 refundability threshold, extend the $1,000 credit, and allow against the AMT; (f) extend the higher 35 percent child and dependent care tax credit rate, raise the phase-out threshold to $85,0 and allow against the AMT; (g) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (h) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (i) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (j) limit value of itemized deduction s to 28 percent; (k) maintain the estate tax at its 2009 parameters; (l) extend the 2001 and 2003 tax cuts for low and middle income individuals including marriage penalty relief, the 10,15, 25, 28 percent brackets, the 15 percent rate on capital gains and qualified dividends for taxpayers in those brackets. Business provisions included were making the research and experimentation tax credit permanent, taxing carried interest as ordinary income, repealing LIFO, international corporate tax reforms, and reforms affecting the tax treatment of financial institutions. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income. 8-Feb-10 PRELIMINARY RESULTS http://www.taxpolicycenter.org Table T10-0032 Administration's FY2011 Budget Proposals Major Individual Income and Corporate Tax Provisions Baseline: Current Law Distribution of Federal Tax Change by Cash Income Level, 2012 1 Detail Table - Elderly Tax Units Cash Income Level (thousands of 2009 2 dollars) Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Percent of Tax Units 3 With Tax Cut With Tax Increase 4.5 15.5 39.5 55.2 64.7 88.5 96.2 97.2 96.2 64.8 39.7 54.8 25.0 20.7 26.9 25.2 22.4 8.6 2.9 2.6 3.8 35.2 60.3 17.3 Percent Change in After-Tax 4 Income 0.2 0.3 0.8 0.8 1.8 2.1 2.8 4.0 4.3 1.6 -0.5 2.1 Share of Total Federal Tax Change 0.1 0.7 2.5 2.1 4.4 13.3 13.2 34.1 27.9 5.3 -3.5 100.0 Average Federal Tax Change Dollars Percent -10 -44 -191 -278 -759 -1,187 -2,077 -4,497 -9,724 -8,412 10,340 -1,289 -5.0 -10.1 -14.6 -11.4 -19.6 -15.4 -14.9 -15.0 -12.2 -4.3 1.0 -8.5 Share of Federal Taxes Change (% Points) 0.0 0.0 -0.1 -0.1 -0.2 -0.6 -0.5 -1.4 -0.8 0.5 3.1 0.0 Under the Proposal 0.1 0.6 1.3 1.5 1.7 6.8 7.0 18.0 18.6 11.0 33.4 100.0 Average Federal Tax Rate Change (% Points) -0.2 -0.3 -0.8 -0.8 -1.6 -1.8 -2.3 -3.2 -3.2 -1.2 0.3 -1.7 5 Under the Proposal 3.0 2.5 4.4 6.0 6.7 10.1 13.3 18.0 23.0 26.6 34.6 18.3 Baseline Distribution of Income and Federal Taxes by Cash Income Level, 2012 1 Cash Income Level (thousands of 2009 dollars) 2 Less than 10 10-20 20-30 30-40 40-50 50-75 75-100 100-200 200-500 500-1,000 More than 1,000 All Tax Units 3 Number (thousands) Percent of Total 2,305 6,471 5,084 2,999 2,259 4,405 2,504 2,986 1,128 245 132 30,543 7.6 21.2 16.7 9.8 7.4 14.4 8.2 9.8 3.7 0.8 0.4 100.0 Average Income (Dollars) 6,366 15,655 25,560 36,054 46,537 64,489 89,136 141,589 304,121 709,954 3,095,895 75,737 Average Federal Tax Burden (Dollars) 201 432 1,310 2,434 3,873 7,688 13,946 29,985 79,745 197,508 1,061,106 15,163 Average After4 Tax Income (Dollars) 6,166 15,223 24,250 33,620 42,664 56,802 75,190 111,605 224,376 512,446 2,034,789 60,574 Average Federal Tax Rate 5 3.2 2.8 5.1 6.8 8.3 11.9 15.7 21.2 26.2 27.8 34.3 20.0 Share of PreTax Income Percent of Total Share of PostTax Income Percent of Total Share of Federal Taxes Percent of Total 0.6 4.4 5.6 4.7 4.5 12.3 9.7 18.3 14.8 7.5 17.7 100.0 0.8 5.3 6.7 5.5 5.2 13.5 10.2 18.0 13.7 6.8 14.5 100.0 0.1 0.6 1.4 1.6 1.9 7.3 7.5 19.3 19.4 10.5 30.2 100.0 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0509-4). Note: Elderly tax units are those with either head or spouse (if filing jointly) age 65 or older. (1) Calendar year. Baseline is current law. The proposal would: (a) extend the higher EITC credit value for families with 3 children and higher phase-out thresholds for married couples and allow it against the AMT; (b) modify the saver's credit making it equal to 50% of the first $500 of retirement savings ($1,000 for couples) and fully refundable; (c) create automatic 401(k)s and IRAs; (d) extend the American Opportunity Tax Credit; (e) extend child tax credit refundability with a $3,000 refundability threshold, extend the $1,000 credit, and allow against the AMT; (f) extend the higher 35 percent child and dependent care tax credit rate, raise the phase-out threshold to $85,0 and allow against the AMT; (g) change the threshold for the 36-percent tax bracket to $250,000 less the standard deduction and two personal exemptions for married couples filing jointly and $200,000 less the standard deduction and one personal exemption for single filers, indexed for inflation after 2009; (h) set the thresholds for the personal exemption phase-out and limitation on itemized deductions to $250,000 of AGI (married) and $200,000 (single), indexed for inflation after 2009; (i) impose a 20 percent rate on capital gains and qualified dividends for taxpayers in the top two tax brackets and repeal the 8 percent and 18 percent rates for assets held for more than 5 years; (j) limit value of itemized deducti to 28 percent; (k) maintain the estate tax at its 2009 parameters; (l) extend the 2001 and 2003 tax cuts for low and middle income individuals including marriage penalty relief, the 10,15, 25, 28 percent brackets, the 15 percent rate on capital gains and qualified dividends for taxpayers in those brackets. Business provisions included were making the research and experimentation tax credit permanent, taxing carried interest as ordinary income, repealing LIFO, international corporate tax reforms, and reforms affecting the tax treatment of financial institutions. (2) Tax units with negative cash income are excluded from the lowest income class but are included in the totals. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (3) Includes both filing and non-filing units but excludes those that are dependents of other tax units. (4) After-tax income is cash income less: individual income tax net of refundable credits; corporate income tax; payroll taxes (Social Security and Medicare); and estate tax. (5) Average federal tax (includes individual and corporate income tax, payroll taxes for Social Security and Medicare, and the estate tax) as a percentage of average cash income.