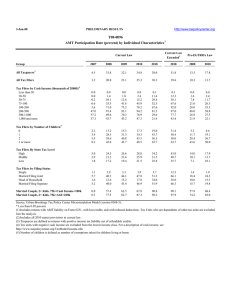

Group 2004 2005 2010

advertisement

T04-0118 AMT Participation Rate (percent) by Individual Characteristics Current Law 2 Extended Current Law Group 1 Pre-EGTRRA Law 2004 2005 2010 2014 2014 2005 2010 3.5 12.9 29.9 19.4 38.8 5.9 12.0 2.5 9.3 22.2 15.2 29.1 4.5 9.3 * * 0.5 1.0 6.2 50.5 39.3 27.0 * 0.7 3.7 16.9 39.4 78.0 41.3 29.2 * 2.8 16.0 52.3 80.2 93.8 62.7 35.5 0.1 4.8 18.6 33.7 39.0 61.2 19.4 17.4 0.1 6.5 30.1 64.3 89.2 95.4 65.3 36.9 * 0.9 4.0 12.4 13.9 26.9 18.6 17.4 * 2.3 11.0 23.2 24.4 44.8 18.5 17.0 1.6 2.2 4.6 7.6 4.1 9.9 23.6 32.0 15.2 27.4 40.3 47.2 5.6 21.1 41.1 55.7 22.0 35.0 47.3 56.1 1.3 2.9 11.2 29.6 2.7 9.2 27.8 46.7 2.3 1.0 0.6 11.0 7.8 5.5 23.4 22.2 18.0 18.6 15.3 11.3 30.2 29.6 25.3 5.7 3.6 2.9 11.6 8.5 6.7 Tax Filers by Filing Status Single Married Filing Joint Head of Household Married Filing Separate 0.7 4.6 0.9 5.6 1.3 18.7 3.5 18.2 2.8 47.1 7.7 45.0 1.9 31.0 10.7 26.3 4.7 62.0 12.8 59.9 0.6 8.5 2.9 10.6 1.1 18.4 6.2 17.3 Married Couple, 2+ kids, 75K<Cash Income<100k Married Couple, 2+ Kids, 75k<AGI<100k 1.1 2.4 42.6 55.3 80.2 93.8 89.7 93.5 90.7 97.7 39.6 41.6 76.0 80.6 All Taxpayers 3 All Tax Filers Tax Filers by Cash Income (thousands of 2003$) Less than 30 30-50 50-75 75-100 100-200 200-500 500-1,000 1,000 and more Tax Filers by Number of Children 0 1 2 3 or more Tax Filers By State Tax Level High Middle Low 4 5 6 Source: Urban-Brookings Tax Policy Center Microsimulation Model (version 0304-3). * Less than 0.05 percent. (1) Includes returns with AMT liability on Form 6251 and those with lost credits. Tax Units who are dependents of other tax units are excluded fom the analysis. (2) Includes all 2010 sunset provisions in EGTRRA and all non-AMT provisions in JGTRRA. (3) Taxpayers are defined as returns with positive income tax liability net of refundable credits. (4) Tax units with negative cash income are excluded from the lowest income class. For a description of cash income, see http://www.taxpolicycenter.org/TaxModel/income.cfm (5) Number of children is defined as number of exemptions taken for children living at home. (6) State codes are not provided on the SOI public-use file for individuals with 1999 AGI above $200,000. Figures here include only those taxpayers for which we have state-of-residence information.