Schroder Wholesale Australian January 2016 Monthly Report 1 mth

January 2016 Monthly Report

Total return % 8

Schroder Wholesale Australian Equity Fund (post-fee)

S&P / ASX 200 Accumulation Index

Relative performance (post-fee)

Schroder Wholesale Australian

Equity Fund

1 mth

-6.70

-5.48

-1.22

3 mths

-6.81

-3.57

-3.24

1 yr

-12.73

-6.13

-6.60

3 yrs p.a. 5 yrs p.a.

1.62

4.29

5.45

-3.83

5.73

-1.44

10 yrs p.a.

5.12

4.68

0.44

Inception Date: 01 Jul 2002, 13 years and 7 months.

Market cap

ASX 1 - 50

ASX 51 - 100

ASX 101 - 300

Non Index

Cash

Top ten holdings %

National Australia Bank Limited

Commonwealth Bank of Australia

BHP Billiton Limited

Westpac Banking Corporation

Woolworths Ltd

Telstra Corporation Limited

ANZ Banking Group Ltd.

Wesfarmers Limited

Rio Tinto Limited

Brambles Ltd

Total

Characteristics

No. of stocks

Portfolio turnover* (1 yr)

Sharpe Ratio (1 yr)

Volatility (5yr standard deviation)

Tracking error (3yr historic)

Portfolio

1

85.3%

7.0%

4.2%

1.1%

2.3%

Portfolio

1

8.6%

6.4%

6.1%

6.1%

5.4%

5.1%

5.0%

4.8%

4.3%

3.6%

55.4%

Benchmark

2

81.5%

11.8%

6.8%

Benchmark

2

5.6%

10.3%

3.8%

7.9%

2.4%

5.3%

5.4%

3.6%

1.3%

1.3%

46.9%

Portfolio

1

50

15.1%

-0.85

12.3%

2.7%

Benchmark

2

200

-0.53

12.5%

1 The 'Portfolio' is the Schroder Wholesale Australian Equity Fund

2 Benchmark is the S&P / ASX 200 Accumulation Index

Unless otherwise stated all figures are as at the end of January 2016

Please note numbers may not total 100 due to rounding

*Turnover = ½(Purchases + Sales - ∑Cashinflows + ∑Cashoutflows) / ½(Market

Value(T0)+ Market Value(T1) - ∑Cashflows)

Please refer to www.schroders.com.au for post-tax returns

Past performance is not a reliable indicator of future performance

Commentary

The S&P / ASX 200 Accumulation Index fell by 5.5%, while the Schroder Wholesale Australian

Equity Fund (post-fee) fell by 6.7%, underperforming by 1.2% for the month.

We had a poor year in 2015, and January 2016 just continued the trend of “growth” stocks overwhelming “value” stocks. The issue in the Australian market now is twofold. Putting cycles aside, in the long run how much difference in growth is there between a “growth” and a

“value” stock; and, secondly, what multiple differential is appropriate for this difference.

To us, a growth stock is not one with momentum, whether that is share price or earnings. A growth stock is simply one able to reinvest valuably, which is at above its cost of capital, for a sustained period. This is how economic value for a shareholder is created, and ultimately, as

Martin highlighted last month, the trailing verification of how much growth has been created is reflected in the growth of net tangible assets, adding back dividends, for each share in a company (assuming gearing is held in a sustainable range). Similarly, our value for a company is simply the forward projection of the same factors. A value stock is hence not one with a low multiple, per se, but rather is one where the gap between this assessed value and the market value of the company exists. In each case, we believe the best investments arise when we are forming a considered view of sustainable earnings, not just spot earnings, and where our views on “growth” and “value” are formed accordingly.

The nature of the Australian market is that cycles are deep and pervasive.

Through “stronger for longer” to now, commodities have reminded us of their cyclical nature in an aggressive fashion through the past decade. It would be an error to think that the commodities cycle is the only one at play in the ASX, however; the interest rate cycle is actually a far stronger presence, especially currently, although because it is at a cyclical high it attracts little critical attention. To give this some perspective, through the past forty years, the Materials sector has represented between 12% and almost 60% of the ASX200; whilst Financials including

Property has represented between 10% and a little more than 50%. That is, the amplitude of the cycle as represented by market value of the equity in the ASX index is both extremely wide, and close to the same in magnitude through time for each of Materials and Financials.

Currently, Materials is close to a forty year low on this measure (i.e. very close to 10%), whilst

Financials are within a few percent of a forty year high. Given this, what is a “neutral” position for an investor in each sector? This is the context in which we argue that a 10% overweighting to materials through the past year, and a similar underweighting to Financials and other bond sensitive stocks on the ASX, is not extreme, even though it has led to a seemingly extreme outcome for our investors through the past year.

Simply put, earnings and price momentum have been the kings of equity market performance.

There is a perfect correlation between earnings momentum and sector performance through the past year, and this trend has been compounded by ratings; that is, those with modestly upgraded earnings have also received large re-ratings, and vice versa.

This is logical if there is large divergence in the “growth” characteristics of stocks within the universe, and secondly that the starting multiples do not reflect this difference in growth profile. Unfortunately, neither is the case. For example, since 2003, the relative growth difference between the (unloved) BHP and the (loved) CSL is approximately 1% per annum compound (on a book value and dividends basis, and even after BHP’s large write offs). That sounds low, but remember that CSL has directed most of its investment in recent years into share buybacks, which currently offers a return of circa 5%. CSL has been and is a well managed company; BHP’s record is clearly mixed. We are not comparing which company is

“good/better” and which one is “bad/worse”. We are simply using history and current actions as a guide as to what the true “growth” history of the two companies is, and dimensioning that even if the future sees those returns diverge to some extent, the starting base in terms of cashflow growth has been far more similar than different. We are using actual numbers for

BHP and CSL to illustrate the principle; “growth” should be defined by economic value, and not anchored to most recent share price performance, which so often colours investment perception.

Schroder Wholesale Australian Equity Fund

Monthly Report

January 2016

Fund objective

To outperform the S&P/ASX 200 Accumulation Index after fees over the medium to long term by investing in a broad range of companies from

Australia and New Zealand.

Investment style

Schroders is a bottom-up, fundamental, active growth manager of

Australian equities, with an emphasis on stocks that are able to grow shareholder value in the long term.

Fund details

APIR code

Fund size (AUD)

Redemption unit price

Fund inception date

Buy / sell spread

Minimum investment

Distribution frequency

Management costs (p.a.)

SCH0101AU

$1,821,216,779

$0.9536

July 2002

0.25%/0.25%

$25,000

Normally twice yearly - June and Dec

0.92%

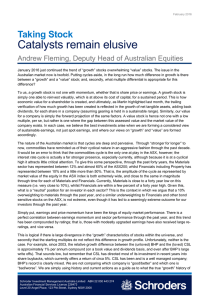

Sector exposure versus the benchmark %

Energy

Chemicals

Construction Materials

Containers & Packaging

Metals & Mining

Paper & Forest Products

Industrials

Consumer Discretionary

Consumer Staples

Health Care

Information Technology

Telecommunication Services

Utilities

Capital Markets

Consumer banks

Diversified Fin Services

Insurance

Real Estate Mgmt & Dev

Property Trusts

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

-4.5

-5.2

-3.8

-3.1

-1.4

-1.5

-0.2

0.0

-1.5

0.3

0.0

0.6

0.5

0.1

1.7

1.1

2.6

3.9

8.4

Commentary Continued

The second limb of the equation is the far more problematic one, today, and that is the multiples investors are now paying for these cashflow streams, which have diverged to their widest levels ever, by some margin. In 2003, both BHP and CSL were trading at 1.5x book value. BHP is now trading at or about 1x book value (even after large write offs) whereas

CSL is trading at almost 9x book value. The former is priced to achieve very low returns on average, into perpetuity; the latter the reverse, with little or no scope for adverse surprise without shareholders incurring a large derating. Recency bias is overwhelming, but history is instructive; going back every year through the past decade will show that the winners and losers across the market in any given year tend not to persist, either because of executional issues or changes in regulation, which prompt a change in the perception of duration attaching to the returns profiles. AGL, for example, was one of the worst performers in

2014, and yet has rerated more aggressively through the past 18 months than the changes in the underlying cashflows generated by the business would suggest should have been the case.

Our underlying core belief is that the sustainable return on investment generated by a company is the single most important driver for long run equity returns. This belief has been challenged as the market has continued to rerate stocks where earnings have been buoyed and derate stocks where earnings have been challenged by cyclical factors through the back half of last calendar year, and this theme continued into January 2016. We appreciate growth will be lower for longer, and that secular breaks are occurring and will occur in the earnings power of industries, however the multiple attaching to the implications of this thematic is objectively at forty year extremes now; we continue to believe it is well beyond being priced in.

Portfolio outlook & strategy

Through the past decade, we have looked to arbitrage price and value in each ASX sector, such that we are underweight when expensive and overweight when cheap. With the exception of property, this has seen us, at different times, overweight or underweight every sector in the market. Rarely have these positions been co -incident with market favour. It is fair to say, though, that our current sectoral positioning feels more isolated than before, and it has been painful for our investors. We can, however, but continue to rely upon the process which has otherwise proven useful through time. We have and are looking to redouble our efforts on forecasting robustly, using fact rather than bias, and have structurally changed resources in our team to that end. We have also made errors (our energy price assumption was too high) but the constants, however, are resolute. Catalysts remain as elusive as ever, but a reliance upon the sustainable cashflow returns generated by a company, for its shareholders, as the basis for our valuation, and the belief that an investment process predicated upon the difference between a share price and this valuation will ultimately produce a better return than one ignoring valuation, remains.

Andrew Fleming

Unless otherwise stated all figures are as at the end of January 2016

Benchmark is the S&P / ASX 200 Accumulation Index

Contact

www.schroders.com.au

E-mail: simal@schroders.com

Schroder Investment Management Australia Limited

ABN 22 000 443 274 Australian Financial Services Licence 226473

Level 20 Angel Place, 123 Pitt Street, Sydney NSW 2000

Phone: 1300 136 471 Fax: (02) 9231 1119

Investment in the Schroder Wholesale Australian Equity Fund ('the Fund') may be made on an application form accompanying the current Product Disclosure Statement available from the Manager, Schroder Investment Management Australia Limited (ABN 22 000 443 274 AFSL 226473) (“Schroders”).

This Report is intended solely for the information of the person to whom it is provided by Schroders. It should not be relied on by any person for the purposes of making investment decisions. Total returns are calculated using exit price to exit price, after fees and expenses, and assuming reinvestment of income. Gross returns are calculated using exit price to exit price and are gross of fees and expenses. The repayment of capital and performance of the Fund is not guaranteed by Schroders or any company in the Schroders Group. Past performance is not a reliable indicator of future performance. Unless otherwise stated the source for all graphs and tables contained in this report is Schroders. Opinions constitute our judgment at the time of issue and are subject to change. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation. For security reasons telephone calls may be recorded.