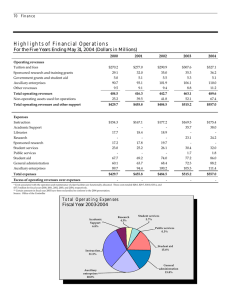

Financial Statements C.S. Mott Community College Flint,

advertisement