Morgan Stanley European Banks and Financials conference Schroders plc Vice Chairman

advertisement

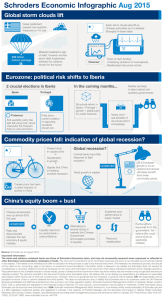

Morgan Stanley European Banks and Financials conference Schroders plc Vice Chairman Massimo Tosato 2 April 2008 trusted heritage advanced thinking Asset management – a changing landscape – Growth of individual and ‘instividual’ savings Channels – Decumulating investors outgrowing accumulating investors Demographic development Percentage of population, Europe 40 Accumulating (40- 59) 30 20 Decumulating (60+) 10 0 2000 Source: Mckinsey 1 2020 2040 Asset management – a changing landscape – Increasing demand for investment solutions Products – Outcome oriented products – The rise of alternatives – The rise of Asia and other emerging markets Markets – Sovereign Wealth Funds – Growth opportunities beyond domestic client base Business model 2 – Change in distribution dynamics Increasing demand for investment solutions Retail: high growth of outcome-orientated funds US Market, 2006 ($mn)* Risk-based life cycle 23 Target-date life cycle 65 Tax managed 33 Inflation indexed 65 Principal protected 11 Source: Mckinsey 3 CAGR% 04-06 Pre-retirement Investment solutions and outcome orientated products Post-retirement Income, absolute return, capital preservation The rise of alternatives Schroders Alternative clients conference March 2008 Investors expecting to increase their allocation in alternatives over the next 3 years* • 86% increased their weighting in alternatives in 2007 Hedge funds • 66% plan to increase their alternatives weighting in 2008 PwC/EIU survey – ‘Transparency vs Returns’* March 2008 4 • Higher alternative allocations expected • Growing focus on governance, quality & scope of reporting 33 40 Private equity 41 Property Infrastructure 35 Commodities 35 Product convergence Global product development continuum Market tracking Innovative products Structured products Above Average Growth ETF Private Equity Real Estate Index funds Hedge funds Quantitative Below average growth Active equities Active bonds Money market ‘Traditional’ products Revenue margin Source: Putnam Lovell, TABB Group estimate 5 Value chain convergence Manufacturing Packaging/design Distribution Future battleground or partnership? Strategic advice, insurance, risk management, provision of beta, etc. 6 End client Schroders: a Company in motion Strength of international business A Company in motion • £139.1 billion total funds under management • Income diversified by channel: 51% retail, 37% institutional and 12% PB • Income diversified by geography: UK £52.7bn 70% of total income outside the UK 37 offices in 28 countries Continental Europe £29.8bn Investment operations in 16 locations 4 in Americas 5 in Europe North America £13.8bn South America £3.4bn 7 in Asia £3.8bn China joint venture 2007 funds under management: Investment by client domicile China joint venture funds under management are not reported within Group funds under management 8 Middle East £3.4bn Asia Pacific £36.0bn Increasing capabilities in alternatives A Company in motion • Property Alternative FUM £15.9bn – December 2007 0.9 • Hedge funds of funds 1.7 • Commodities & Agriculture • Private Equity • Multi-manager 2.2 8.8 2.3 property funds of hedge funds private equity funds of funds 9 emerging market debt commodities Schroders A Company in motion Record results in 2007 £mn • Strength of international business 1200 • Diversity of product range • 400 1000 300 800 392.5 Focus on high margin products 600 • 200 Growth in Retail 400 • Repositioning in Institutional • Transformed profitability in Private Banking 290.0 230.3 200 0 0 2005 Income (lhs) 10 100 2006 Costs (lhs) 2007 PBT (£mn) Forward-Looking Statements These presentation slides contain certain forward-looking statements and forecasts with respect to the financial condition and results of the businesses of Schroders plc These statements and forecasts involve risk and uncertainty because they relate to events and depend upon circumstances that may occur in the future There are a number of factors that could cause actual results or developments to differ materially from those expressed or implied by those forward-looking statements and forecasts. Nothing in this presentation should be construed as a profit forecast 11