Fund Appreciation Rights® What They Are and How They Can Work for Institutional Investors and Hedge Fund Managers

advertisement

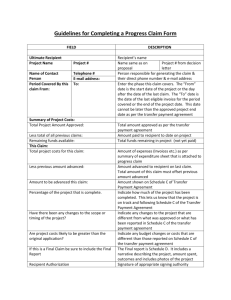

Fund Appreciation Rights® What They Are and How They Can Work for Institutional Investors and Hedge Fund Managers Panelists: Joel D. Almquist, K&L Gates Partner James E. Earle, K&L Gates Partner Rick Ehrhart, Optcapital Nicholas S. Hodge, K&L Gates Partner Thom Young, Optcapital FAR ® is a registered trademark of Optcapital FARs®: What and Why?” The Alignment Challenge “Alignment of interests is more important than alpha generation these days – according to investors in the industry’s top hedge funds” – Absolute Return: Hedge Fund Report Card “Performance fees should create alignment of incentives through timing mechanisms (e.g. deferments, holdbacks, and/or claw backs), appropriate hurdle rates, and egalitarian terms for all investors.” – URS Summary of Preferred Hedge Fund Terms “The present model provides the possibility of a hedge fund manager realizing a 20 percent performance fee at the end of a bonanza year. If the fund suffers a significant decline the next year, the manager could still have a large net gain at the end of the two years, but the investor may break even or even lose money.” – CalPERS Press Release March 27, 2009 3 Keys to Better Long‐Term Alignment Multi‐Year – Performance (incentive) compensation measured over life of investment (not year by year) Co‐Investment – Manager’s capital invested pre‐tax, tax‐deferred side‐by‐side with Investor’s Mutual Commitment – Investor and Manager commit capital for coterminous periods Transparency – Manager has ability to withdraw and thereby signal Investors Sustainability & Stability – Funding business Attracting and retaining human capital 4 How Did We Get Here? Traditionally, incentive comp measured and “banked” annually Annual fees (whether paid or deferred) Annual profit allocations (“carried interest”) Extent of alignment: Fees co‐invested pre‐tax, tax‐deferred (but annual measurement) A few large investors negotiated longer (multi‐year) performance periods or “claw backs” against previous year’s comp 2008 – New IRC Section 457A No more deferral of fees from offshore Funds and all existing deferred comp taxable no later than 2017 All comp from offshore funds must be taxed each year Result: multi‐year comp periods banned and claw backs unworkable thereby largely eliminating traditional techniques designed to achieve long‐term alignment 5 Funding Partners’ & Employees’ NQDC Fund Plan Level ABC Offshore Fund, Ltd ABC Offshore Fund 409A Plan ABC Manager LLC Manager Plan Level ABC Manager Partner Plan Partner A (60%) Partner B (40%) ABC Manager Employee 409A Deferred Compensation Plan Portfolio Manager 6 Trader Analyst Current State Current Alignment is Short‐Term Only Annual Incentives – Investors pay for unrealized returns Moral Hazard – single year comp periods and less co‐investment may lead to excessive risk‐taking Conflict of Interest – carried interest incents long‐term gains over short‐term, while Investors want highest return without regard to tax effects Institutional Investors Seek Better Alignment Annual “crystallization” causes Investors to pay more than agreed rate Investors seek multi‐year comp periods and co‐investment 7 A Long‐Term Alignment Solution – FARs® Stock Appreciation Rights (SAR) settled in Fund Shares or net‐settled call Option to buy Fund Shares (these are identical in operation) are exempt from 457A (and 409A) if properly structured Fund issues FAR® to Manager on percentage of Investor’s investment Manager’s benefit is “Spread” – excess of NAV over Strike Price Strike Price is equal to or greater than NAV on grant date Spread grows pre‐tax, tax‐deferred, at gross performance until FAR® exercised Manager can exercise at any time during the Exercisability Term Spread received is taxable as ordinary income 8 FARs® vs Annual Incentive Comp Year 1 Return: 50% Annual Comp: 20% of Annual Profits on 100% of Investment $10m $40m $100m FARs®: 100% of Cumulative Profits on 20% of Investment $40m $10m $80m $20m 0 1 Year 0 1 Year 9 Fundamental Difference Year 1 Return: 50% Year 2 Return: ‐30% $10m Annual Comp $40m ‐$42m $98m $100m With Annual Comp, Investor pays $7m on $2m cumulative loss ‐$3m $7m With FAR®, Investor claws back $6m of incentive comp earned in year 1 and pays exactly 20% of cumulative profit of $5m FARs® $40m $10m ‐$36m ‐$9m $80m $20m $84m $20m 0 1 Year 0 1 Year 1 2 Year 1 2 Year 10 $1m A Real Difference in 2008 Actual If FARs® $53m * Source: CSFB Tremont Long/Short Index. Returns grossed up for estimated annual performance fees. 11 As of end of 2008, Investor would have had 20% more profit Superior Attraction & Retention FARs® are ideal vehicle for financing Manager’s NQDC Plan for PMs, analysts and traders (“Participants”) Manager NQDC Plan can provide for Participant vesting and Participant accounts that mimic Spread of FARs® Because FARs® are tax‐deferred until exercise, Manager (i.e., Partners) incurs no cost from providing NQDC to Participants 12 Funding Partners’ & Employees’ NQDC Fund Plan Level ABC Offshore Fund, Ltd ABC Offshore Fund FAR® Plan ABC Manager LLC Manager Plan Level ABC Manager Partnership Agreement Allocating FARs® Partner A (60%) Partner B (40%) Partners are allocated FARs® ABC Manager Employee 409A Deferred Compensation Plan Portfolio Manager Trader Analyst Employees’ accounts mimic FAR® Spread 13 The FAR® Advantages Investor Benefits Compensation for performance for agreed upon period Claw back ensures compensation doesn’t exceed agreed rate Side‐by‐side co‐investment Transparency of manager compensation Manager Benefits An alignment solution that will attract capital from like‐minded, long‐term investors Effective tool to attract and retain top talent Pre‐tax, tax‐deferred accumulation of capital available for business continuity 14 FAR Tax Structure and Considerations Traditional Incentive Allocation (Carried Interest) and Incentive Fee Incentive Allocation made annually by domestic fund 20% of appreciation in each partner’s capital account. This ensures that only partners who have experienced gains since their admission are charged Allocation allows general partner/managing member to benefit from lower tax rate on long term capital gains generated by the fund. High water mark If the value of a capital account drops, the manager will not earn another incentive allocation until the value again rises above its last high point (the “high water mark”). Loss Recovery Account keeps track of this. Incentive Fee charged annually to offshore fund 20% of appreciation with respect to each class of shares This ensures that only shares that experience gains are charged Ordinary income Managers sometimes deferred receipt of fees and thereby deferred taxes 16 Legislative Developments Carried interest ‐‐ Proposed legislation (see H.R. 1935) would treat all allocations with respect to “investment services partnership interest” – which would include the GP’s interest in a fund – as compensation income Deferred incentive fees ‐‐ Ability to defer fees payable by an offshore fund has been eliminated by the 2008 enactment of Code Section 457A 17 New Section 457A Eliminates any deferral under a nonqualified deferred compensation plan of a nonqualified entity when there is no substantial risk of forfeiture of the rights to compensation Penalizes compensation deferral that results from a performance measurement period of longer than one year “Nonqualified deferred compensation plan” – has the meaning given that term under section 409A, “except that such term shall include any plan that provides a right to compensation based on the appreciation in value of a specified number of units of the service recipient” 18 Nonqualified Entity “Nonqualified entity” means Any foreign corporation unless substantially all of its income is Effectively connected with the conduct of a trade or business in the U.S., or Subject to a comprehensive foreign tax Any partnership unless substantially all of its income is allocated to persons other than Foreign persons with respect to whom such income is not subject to a comprehensive foreign tax, or Tax‐exempt organizations “Substantially all” = 80% (per Notice 2009‐8) 19 Notice 2009‐8 excludes from the definition of “nonqualified deferred compensation plan”: for both corporate and partnership nonqualified entities: options on service recipient equity with FMV exercise price with no deferral beyond exercise of option or vesting of equity for corporate nonqualified entities only: service recipient stock‐settled (by its terms and in fact) SARs with FMV exercise price 20 409A Compliance The exceptions under section 457A for options and SARs are based upon the regulations under section 409A. 409A regulations provide a comprehensive regulatory regime expressly intended to address the risk of using options/SARs as a form of "disguised" deferred compensation. • Key requirements: the option/SAR must be (i) granted with respect to “service recipient stock”, (ii) by an “eligible issuer of service recipient stock”, (iii) with a strike price not less than FMV on date of grant and (iv) includes no other deferral features (other than recognition of “spread” upon exercise). • Regulations include a specific provision regarding an “investment vehicle” service recipient and permits grant of an option/SAR by the investment vehicle to its direct service providers. 21 Common Stock – Offshore Fund 409A regulations describe options and rights with respect to service recipient stock “that, as of the date of grant is common stock for purposes of section 305 and the regulations thereunder of a corporation that is an eligible issuer of service recipient stock.” Are shares of an offshore fund ”common stock” for purposes of section 305? 22 Common Stock – Offshore Fund For purposes of section 305, common stock is any stock that is not preferred stock. “The term preferred stock generally refers to stock which, in relation to other classes of stock outstanding, enjoys certain limited rights and privileges (generally associated with specified dividend and liquidation priorities) but does not participate in corporate growth to any significant extent.” 409A regulations also provide that “service recipient stock” does not include a class of stock that has any preference as to distributions other than distributions of service recipient stock and distributions in liquidation of the issuer, nor any stock subject to a mandatory repurchase obligation (other than a right of first refusal) or subject to a put or call right that is not a lapse restriction if the price is other than fair market value. 23 Common Stock – Offshore Fund Which offshore fund shares are common stock? Offshore funds often have many “classes” of stock designed to take into account Timing of investment by different investors “new issues” eligible and ineligible investors Sidepockets Creation of preferred shares to provide SAR base SAR must be with respect to common shares Offshore fund stock is redeemable at net asset value (so it is not subject to a put or call right that is not a lapse restriction if the price is other than fair market value). 24 Is an offshore fund an eligible issuer? Generally, an “eligible issuer” is the corporation for which the service provider provides direct services on the date of grant of the stock right, and any corporation in a chain of corporations or other entities in which each corporation or other entity has a controlling interest in another member of the chain. In a master‐feeder structure, does the investment manager provide services to the master or to the feeder? Or to both? 25 Service Recipient Stock – Domestic Fund Notice 2009‐8 includes in the definition of “service recipient stock” an equity interest in a non‐corporate entity. So a nonqualified option on an equity interest in a partnership is also excluded from the application of section 457A. This treatment does not extend, however, to stock settled SARs. 26 “Stock Settled” Requirement for SARs Notice 2009‐8 permits FMV options. Notice 2009‐8 permits FMV SARs that by their terms at all times must be settled in service recipient stock and are in fact settled in service recipient stock. How long must the service recipient stock be held by the service provider following exercise of option or SAR? 27 Why are Options and SARs OK under 457A? House Report 110‐658 explains Section 457A Under 457A, nonqualified deferred compensation includes any arrangement under which compensation is based on the increase in value of a specified number of equity units of the service recipient. But nonqualified deferred compensation does not include an arrangement taxable under section 83 providing for the grant of an option on employer stock with an exercise price that is not less than FMV on the date of grant if such arrangement does not include a deferral feature other than the feature that the option holder has the right to exercise the option in the future. Notice 2009‐8 allows stock‐settled SARs because they are equivalent to stock options with a cashless exercise. Also, they are taxable under section 83. 28 Service Recipient Stock – Offshore Fund Option or SAR is with respect to PFIC stock Option to acquire PFIC stock is treated as PFIC stock for purposes of PFIC anti‐deferral provisions PFIC‐related considerations: purging election at time of option or SAR exercise Qualified electing fund (QEF) election following exercise 29 Service Recipient Stock – Domestic Fund Compensatory options on partnership interests Proposed Regulations – not final How is deduction allocated among partners? Valuation issues – FMV vs. liquidation value. Procedural requirements for using liquidation value. When does service provider become a partner? Capital accounts and partnership allocations. 30 Legislation affecting Domestic Funds H.R. 1935 – proposed Section 710 ‐‐ partners providing investment management services to partnership Ordinary income treatment, including any income or gain with respect to options and other disqualified interests with respect to partnership Should not impact options with respect to domestic fund 31 Corporate and Financial Institution Compensation Fairness Act, H.R. 3269 Passed by the House on July 31, 2009 Section 4 of that Act would require certain “covered financial institutions” to have compensation structures that (i) properly measure and reward performance, (ii) are structured to account for the time horizon of risks and (iii) are aligned with sound risk management. Options/SARs, properly designed and administered, can accomplish all three stated goals. 32 FARs®: How? FAR® Design Investor Objectives Multi‐year compensation Side‐by‐side Mutual commitment Transparency Sustainability & stability Manager Objectives Attract capital Retain talent Tax‐efficient wealth accumulation 34 Co‐Investment Commitments INVESTOR CAPITAL COMITTMENT – For agreed upon capital commitment period (“lock up”), Investor cannot redeem without penalty MANAGER COMMITMENT No exercises, OR In event of exercise, Investor can redeem without penalty AFTER LOCK UP – Investor can redeem without penalty and Manager can exercise SIGNALING – In any event, Investor may require Manager to give advance notice of any exercise so Investor can make redemption decision HOLDING PERIOD – After exercise, how long must Manager hold shares 35 Strike Price Design Strike Price can never be less than NAV of Underlying Security at date of grant Typically, initial Strike Price set to equal NAV at grant Investor moving from NAV that is below “high water” NAV may want initial Strike Price to be above NAV at grant Strike Price can be indexed to create hurdle rate or to cover financing costs in the event FARs® continue beyond redemption of Underlying Security 36 New Appreciation Grants Investor invests $100m and FAR® percentage is 20% End of Yr 1 50% Return Beginning of Yr 2 End of Yr 2 20% Return $22.4m $40m $80m $32m $32m $10m $10m $20m $20m Initial FAR® (20% of $100m contribution) $80m $8m New Appreciation FAR® (20% of $40m growth) 37 $20m $80m $1.6m $6m $10m $8m One Design Example Strike Price is indexed to management fee Staggered lock ups FARs® Available for Exercise Strike Price Growth (hurdle) NAV at Grant Year 0 Spread Year 1 Year 2 Year 3 38 Year 4 Strike Price Growth Initial Strike Price Summary: Complete Solution FAR® Fund 1 FAR® Fund 1 Plan FAR® Fund 2 FAR® Fund 3 FAR® Fund 2 Plan Fund Plan Level FAR® Fund 3 Plan Manager Partnership Agreement Employees 409A Plan Vestin g Class Partner A (60%) Mgr Plan Level Class Vestin g Class Class Vestin g Class Partner B (40%) Portfolio Manager Trader 39 Analyst Class Design Considerations Grant percentage on Contributions Grant frequency and percentage on New Appreciation Strike Price Initial Strike Price (can be equal to or greater than NAV) Strike Price Growth Rate initially and after redemption (if any) Co‐investment commitments Holding period after Exercise Rule governing action upon redemption – Exercise or Convert Shareholder notification of Exercises Integration with Manager’s 409A account balance Plans 40 Implementation Considerations Bolt on or start new? Shareholder notice MFN Trading Use of feeder fund to avoid expense erosion to FAR® Ensuring underlying shares are “service recipient” common stock Avoiding distribution preferences Ensuring FMV issuance – capital structure should avoid appearance of issuing FAR®s at less than FMV Integration with Manager’s 409A Plans 41 Operational Considerations Tracking FARs and Share Classes by Investor and in aggregate VUS, Strike Price and Spread Share Class NAVs (Common and Preferred) Contribution Grants, New Appreciation Grants and Replacement Grants Effect of redemptions on FAR®s ‐‐ limited to Investor’s FAR®s FAR® exercise methodology – Investor neutral FAR® exercise notifications PFIC filings Accounting treatment 42 Operational Considerations (cont’d) Integration with Manager’s 409A Plans or Partner Plans Self‐administration or third party administration FAR® Plan Manager’s NQDC Plans for Partners and Employees Coordination with Fund Administrator 43 Question and Answer Session For those attending via the webinar, please send your questions via the chat box on your screen. Our webinar host will relay the questions to the panel. 44 Webinar Recording For those of you who would like to listen to this program again, we will be distributing a link to a recorded version of the program. If you have any follow up questions, please feel free to contact Matt Prinn at 617-261-3143 or matt.prinn@klgates.com 45