Proceedings of World Business, Finance and Management Conference

advertisement

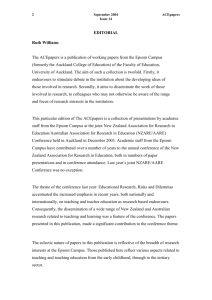

Proceedings of World Business, Finance and Management Conference 14 - 15 December 2015, Rendezvous Grand Hotel, Auckland, New Zealand ISBN: 978-1-922069-91-7 Direct versus Indirect Property Investment in New Zealand Fennee Chong1 This paper evaluates the prospect of direct versus indirect property investment in New Zealand. Monthly data of residential property returns and Real Estate Investment Trusts (REITs) listed on New Zealand Stock Exchange are used in the analyses. Results show that direct property investment in residential property in New Zealand and Auckland underperformed its indirect investment counterpart during the study period. This study also found that the higher return from REITs investments comes at a higher risk. JEL Codes: F65, G10 and D31 1. Introduction Property investment in New Zealand remains as one of the most controversial topics among policy makers and investors. The reasons behind the rapid increases in property prices are debated by many and measures involving monetary and fiscal policies have been taken to remedy the overheated market. According to the OECD (2015), New Zealand properties are overvalued with a price-to-rent ratio equals to seventy and the prediction that the bubble will burst anytime is reported by the media from time to time. This paper aims to provide some insights to investors on the direct versus indirect mode of venturing into this market. 2. Literature Review Direct Property Investment Direct property investment can be subdivided into residential and commercial property investment. Most direct property investors are investing in residential properties because i) the initial outlay required for commercial property such as office building and shopping malls is many times higher than residential property, ii) commercial property is difficult to sell off as there are limited buyers who are capable of paying multi-millions of dollars for high end commercial properties. On the other hand, residential property is highly in demand as home ownership is one of the most important aspects in one’s personal financial planning life cycle. Regardless of the size and location of the house, a home offers the sense of security and stability that ownership brings. iii) advice from professionals is required in commercial property investment for valuations and leasing while this can be minimised in residential property investment as information on valuation and leasing is readily available on websites. Investment in residential property is slightly different from home ownership as the ultimate aim of this transaction is for future cash flow in the form of rental income, and capital gain when the property is put up for sale in the market place rather than the psychological reward as a homeowner. Buying a property obviously requires more careful planning and analysis as it is a big-ticket item that involves larger capital outlay and is relatively illiquid in comparison with asset classes such as stocks and bonds. Apart from deciding on the location and the size of property, 1 Dr. Fennee Chong, Department of Finance, Auckland University of Technology, New Zealand. Email:fchong@aut.ac.nz Proceedings of World Business, Finance and Management Conference 14 - 15 December 2015, Rendezvous Grand Hotel, Auckland, New Zealand ISBN: 978-1-922069-91-7 factors such as the availability of mortgage, interest rates, down payment, insurance, management and maintenance fees, as well as tax planning, need to be taken into consideration. Location is important as it determines the turnover rate and the potential for higher profit margin. According to Quotable Value Limited (2015), the average residential house price in the Auckland area at May 2015 was NZD992227 while the average house price in South Waikato (200 km from Auckland) was reported at NZD129240 during the same period. Auckland, being the biggest city has almost two thirds of the total population of New Zealand and therefore, the turnover rate and the price growth are relatively higher due to a higher demand compared to any other locations in the country. Multi-offers for a house in auctions continue to inflate and accelerate the unaffordability of residential properties for the many average income earners in New Zealand. It is common for the rich to own a few properties at the same time. A related study by Cheung (2011) contends that the overwhelming popularity in housing investment in New Zealand in the past decade has caused a persistently large saving-investment imbalance whereby wealth is concentrated in one asset class i.e. property. Constant under-supply of houses coupled with the tax incentives have driven the market to greater heights and this phenomenon has amplified the desire to enter the property market by those who can afford the investment whilst pushing affordability towards its outer limit for those with lower incomes. The chart published by OECD (2015) shows that New Zealand housing was among the top five most over-valued in terms of both price-to-rent and price-to-income ratios. Figure 1: House prices across OECD (June, 2015) In order to help both the financial institutions and borrowers to hedge against the risk of possible property market downturn due to economic recession or increased interest rates, the Reserve Bank of New Zealand has imposed a loan-to-value restriction on 1 October 2013. This restriction was also meant to reduce the systemwide risks of the financial cycles which could be driven by fast credit growth, intensifying household debt or excessive liquidity (Reserve Bank of New Zealand, 2013). Under the loan-to-value restriction, direct property investors need to come up with 20% to 30% of the property price as a down payment depending on the location of the residential property. To cool the housing market further, apart from restricting the amount of high loan-to-value lending, the Reserve Bank of New Zealand also raised the Official Cash Rate by twenty-five basis points three times in 2014 Proceedings of World Business, Finance and Management Conference 14 - 15 December 2015, Rendezvous Grand Hotel, Auckland, New Zealand ISBN: 978-1-922069-91-7 (Reserve Bank of New Zealand, 2014). The rapid increases in the mortgage lending rates could lead to diminishing profit arising from direct property investment. Investors who opt for a floating rate will suffer the most when lending rates increase. Tax shelter is not a main concern in New Zealand at this point as no rebate is granted for property buyers on property purchases. On the other hand, after decades of slack capital gains tax policy, the government announced in its 2015 budget that a property gains tax will be levied on profit made at disposal of residential property sold within two years of buying with exemptions provided for family home, inherited estate or relationship settlement. Tighter rules are also introduced to control nonresident investors entering the New Zealand residential market for quick profit. Among others, overseas buyers will be required to provide an IRD number and a New Zealand bank account number for any property transactions done after October 2015. Residential rental investors are required to pay tax on the rental income based on the owner’s tax bracket. Other fees that property investors are required to pay are agent fees for rental management, council rates, maintenance fees and commission at sale. Agent fees are not regulated in New Zealand. Therefore, the commissions can vary and investors are advised to compare and negotiate commission to be paid. Agent fees in Auckland can range from 4 to 7.5% for rental management. For selling, as indicated in Table 1, a base fee of NZD13, 683 is charged for properties below $300,000. Other typical commissions for difference price ranges are as shown below. Selling price (NZD) Up to $300,000 400,000- 499,999 500,000 – 749,999 750,000 – 999,999 1,000,000 -1,499,999 1,500,000 – 1,999,999 2,000,000 – 2,999,999 3,000,000 – 4,999,999 5,000,000 Table 1: Agent fees Estimated percentage of agent fees (%) 4.56 4.30 4.00 3.50 3.24 3.00 2.86 2.73 2.63 Source: Barfoot and Thompson (2015) On top of commissions charged, property owners are also required to pay GST. Owners are also responsible for solicitors’ fees at the point of purchase and sale. Indirect Property Investment – Real Estate Investment Trusts (Reits) Indirect property investment is another form of property investment where the investors own a portion of property via a trust fund. Only two REITs are listed on the NZX50. The first listed REIT was the Goodman Property Trust (GMT), later followed by the Vital Healthcare Property Trust (VHP). The Goodman Property Trust (GMT) was listed in June 1999 with a portfolio value of NZD 145 million. GMT’s portfolio comprises of a mix of leasing and developing of industrial facilities, office assets and infrastructure investments in Auckland, Wellington and Christchurch. After 15 years, GMT’s net tangible asset per unit raised from $1 to $1.084 cents (GMT Annual Report, March 2015) and it has a market capitalisation of NZD1.473 billion as at June 2015. Proceedings of World Business, Finance and Management Conference 14 - 15 December 2015, Rendezvous Grand Hotel, Auckland, New Zealand ISBN: 978-1-922069-91-7 VHP was listed in September 1999 under the name of Calan Healthcare Properties Trust. It is a listed property fund investing in high quality health- and medical-related properties in NZ and Australia. The net tangible asset per unit for VHP was $1.03 in March 2015 while the total market capitalisation for VHP was NZD564.433 million in June 2015 (NZX, 2015). 3. Analysis and Findings This paper focuses on assessing the prospect of direct investment in residential property versus the investment of REITs listed on the New Zealand Stock Exchange. To provide some indications on the expected return and risk profile of these two types of property investments, the average return and the standard deviation of listed property trusts on the NZX and the monthly residential property returns (Auckland and New Zealand) for the past 77 months are calculated. Data of residential property returns were collected from the database of Quotable Value Ltd (QV), a State Owned Enterprise and the largest property and valuation company in New Zealand, while data of REITs i.e. Goodman Property Trust (GMT) and VHP were collected from the NZX. Descriptive statistics PERCENTAGE i) 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 0 -1 -2 -3 -4 -5 -6 -7 -8 -9 -10 -11 -12 Monthly Return MONTH Auckland Average Return Goodman Property Trust Return NZ Average Return VHP Property Trust Return Figure 2: Monthly Return of All NZ Residential Property, Auckland Residential Property, GMT Property Trust and VHP Property Trust from January 2009 – May 2015 Referring to the line graphs in Figure 2, Auckland’s monthly returns before adjustments was dominating and closely related to the national return. The highest monthly return (changes) was recorded in February 2015 with a surge of 21% compared to the previous month. On the other hand, the REITs under study generally reported more dynamic and volatile monthly returns compared to their direct property investment counterparts. Between the two REITs, monthly returns of VHP seem to be more unstable than GMT. Proceedings of World Business, Finance and Management Conference 14 - 15 December 2015, Rendezvous Grand Hotel, Auckland, New Zealand ISBN: 978-1-922069-91-7 ii) Returns Table 2: Returns Calculations Variables Gross yearly average return Gross yearly average return (capital and rental yield) Yearly average returns: After adjustment I Note 1 After adjustment II Note 1 After adjustment III Note 1 After adjustment IV Note 1 After adjustment V Note 1 After adjustment VI Note 1 After adjustment VII Note 1 After adjustment VIII Note 1 Yearly average return (REITs) Yearly average return of listed REIT Yearly average return of REIT after commission All NZ 7.23 11.65 Percentage Auckland 13.09 17.03 2.81 7.23 -3.44 -3.55 0.98 0.87 -3.52 -3.63 Goodman 11.64 11.28 8.67 12.61 2.57 2.89 6.508 6.835 2.00 2.34 VHP 14.45 14.39 Note 1: Adjustment I refers to adjustment after sales commission Adjustment II refers to adjustment after sales commission and rental yield Adjustment III refers to adjustment after floating rate and sales commission Adjustment IV refers to adjustment after fix rate and sales commission Adjustment V – after interest (floating), sales commissions and rental yield Adjustment VI – after interest (fix rate), sales commission and rental yield Adjustment VII – after adjustment V and rental agent fees at 4.5% Adjustment VIII – after adjustment VI and rental agent fees at 4.5% Note 2: capital gains tax for both direct and indirect property investment is not taken into consideration. Note 3: Rental yield was calculated using the bond submission data obtained from Ministry of Business. Innovation and Employment Table 2 shows the return calculations of all the proxies used in this study. The yearly average return during the study period of all New Zealand residential property was 7.23% while for Auckland was 13.09% before adjusting for interest charges, sales commission, rental yield and rental agent fees. With the inclusion of rental yield, these returns can range from 11.65% to 17.03% depending on location. Further analyses on the returns based on various scenarios were done and the results were as shown in Table 2. If direct property investors purchased the residential property with cash, it was likely they would gain 2.81% on average in New Zealand and 8.67% in Auckland after paying sales commissions. However, under the scenario where the residential property was purchased using external funding such as a loan, without rental yield investors are expected to make a loss of between 3.44 to 3.55% generally in New Zealand while making a profit of between 2.57 to 2.89% after adjusting for interest charges (floating or fixed) and sales commissions (see after adjustment III and IV in Table 2). On the other hand, if externally financed residential property was being rented out and managed by the owner, Auckland properties are estimated to bring in around 6.51 to 6.84% of return per annum whilst the national return was only marginal (see after adjustment V and VI in Table 2). These profits are expected to drop another 4 to 7.5% if a rental agent is used (see adjustment VII & VIII). Generally, the most lucrative return (12.61%) for direct residential investment happens when an investor purchases a property in Auckland using cash and manages to rent the property out without using a property agent. This level of performance however, cannot be attained at locations other than Auckland. Proceedings of World Business, Finance and Management Conference 14 - 15 December 2015, Rendezvous Grand Hotel, Auckland, New Zealand ISBN: 978-1-922069-91-7 REITs on the other hand reported a return of 11.64% and 14.45% per annum for GMT and VHP respectively. Commission for REITs transactions is 0.3% per trade using the internet, 0.7% via telephone and 1% for sale through a broker. If investors were to buy and sell via the internet, then the yearly average return would range from 11.58% to 14.39% after commissions. From the discussion above, investing in indirect property i.e. REITs, seems to be offering a higher return then most of the scenarios analysed on direct property investments during the same study period. To confirm on whether REITS investment returns are significantly better than direct property investment statistically, a test on mean equality was conducted based on the following hypotheses and the results are reported in Table 3: Ho: There is a no significant difference between the performance of direct property investment and indirect property investment Ha: There is a significant difference between the performance of direct property investment and indirect property investment Table 3: Equality of means between series test: Variables Wilcoxon/Mann- Probability Whitney statistics Returns of NZ and GMT 9.586391 0.0001 Returns of NZ and VHP 9.991735 0.0000 Returns of Auckland Residential Property and 9.755899 0.0000 GMT Returns of Auckland Residential Property and 9.394774 0.0001 VHP *Note: Returns of NZ and Auckland residential investment are adjusted for interest expenses, sales commission and rental yield. Returns for GMT and VHP are adjusted for commissions. Four tests were performed on different series as stated in Table 3. Findings show a significant difference between the adjusted returns of direct and indirect property investments on all the tests at 95% significance level. iii) Risk Nonetheless, analysis of returns is incomplete without taking the risk assumed into consideration. Standard deviation measures the dispersions of the return of a fund from the expected normal returns and it can be derived using the following formula: ∑ √ Where: 𝝈 = Standard deviation ri = Price returns m = Mean of all data points n = Number of data points Table 4: Risk Calculations: Standard Deviation Variables Standard deviation Return of NZ residential property 4.39 Return of Auckland residential property 9.08 Return of Goodman property trust 12.06 Return of VHP property trust 12.26 Proceedings of World Business, Finance and Management Conference 14 - 15 December 2015, Rendezvous Grand Hotel, Auckland, New Zealand ISBN: 978-1-922069-91-7 Referring to the results in Table 4, indirect property investments via REITs reported a higher standard deviation compared to direct property investment, indicating a higher risk in indirect property investment. VHP property trust is the riskiest among the four different types of property investment. 4. Conclusions Based on the analyses discussed above, direct property investment in residential property in New Zealand and Auckland underperformed its indirect investment counterpart during the study period. However, risk assessment shows that the higher return from REITs investments comes at a higher risk. From the findings, indirect property investment suits investors with a higher risk appetite whilst risk-cautious investors could be better off investing directly in Auckland residential properties. Nonetheless, since past research and recent government policies are hinting at an overheated property market, investors must exercise caution while investing directly in the New Zealand property market. A downturn in the property market will hurt direct property investors the most as a direct investment involves huge capital outlay and is associated with higher illiquidity. References Barfoot and Thompson (2015). Our commission rates. Retrieved from: http://www.bartfoot.co.nz/sell/our-commission-rates? Cheung, C. (2011). Policies to rebalance housing markets in New Zealand. OECD Economics Department Working papers No. 878. Good Man Property Trust (2015). Good Man Property Trust Interim Report. Retrieved from: http://www.goodmanreport.co.nz/financial-reports.zhtml. OECD (2015). Economic outlook, analysis and forecasts: Focus on house prices. Retrieved from: http://www.oecd.org/eco/outlook/focusonhouseprices.htm. OECD (2015). OECD Economic Surveys: New Zealand 2015, OECD Publishing, Paris. http://dx.doi.org/10.1787/eco_surveys-nzl-2015-en. Reserve Bank of New Zealand (2013). Why Loan-to-Value Ratios were introduced. Retrieved from: http://www.rbnz.govt.nz/news/ Reserve Bank of New Zealand (2014). RBNZ raises OCR to 3.5 percent. Retrieved from: http://www.rbnz.govt.nz/news/ NZX (2015). Vital Healthcare Property Trust Analysis. Retrieved from: http://www.nzx.com/markets/NXSX/securities/VHP/analysis Quotable Value Limited (2015). Residential house values. Retrieved from: https://www.qv.co.nz/resources/monthly-residential-value-index