A Nonprofit’s Roles and Responsibilities Donations:

advertisement

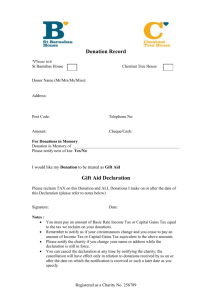

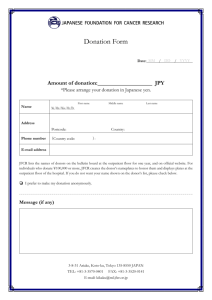

Donations: A Nonprofit’s Roles and Responsibilities As we have mentioned in previous Topics of the Month, the majority of donors do not contribute to an organization solely because they will receive a tax deduction. Furthermore, even though the majority of individuals (approximately 65%) do not itemize their taxes and therefore do not technically apply tax deductions, many will want to know if their gift is tax deductible. It is important for nonprofit organizations to know which types of donations may not be tax deductible as well as how to receipt different types of gifts. This Topic of the Month looks at donations from two different perspectives: the organization’s and the individual’s. It outlines the types of donations that nonprofit organizations receive, the organization’s internal and external responsibilities for each type of donation, as well as the criteria for individuals to determine whether a donation is tax deductible or not and, if so, the value of the donation. Examples of both cash and in-kind donations are also provided. 1 Different Types of Donations There are two types of donations: cash and in-kind (non-cash) donations. While cash gifts in the form of a check, credit card, or cash are by far the most popular type of gift, over the last few years donors have increasingly decided to give in-kind donations instead of or in addition to cash donations. An in-kind donation is essentially any non-cash item given to a nonprofit that is to be used for the benefit of the nonprofit. These can include items such as computers or books; property such as real estate or inventory; and financial assets such as stocks or bonds. Responsibilities of the Organization When Receiving Donations Charitable deductions are claimed by donors on their individual tax returns (IRS Form 1040), if they choose to itemize their deductions. Thus, it is up to the donor and his or her tax advisor to determine the value of the deductions, when to deduct it, and in what manner. The nonprofit must make sure that it complies with all substantiation and documentation requirements for the donations it receives. As a result, there are both external and internal steps to be taken after receiving a donation. External: A. Cash: The IRS mandates that anyone who makes a donation of $250 or more to a nonprofit must be provided with a receipt from the nonprofit that indicates that no gifts or services were received in exchange for the donation. A sample receipt is provided at the end of this paper. This 1 Please note that while Cathedral Consulting Group, LLC is in the operation and strategy consulting practice and does not hold itself out as tax and legal experts. We do, however, provide tax and legal insights when such observations may be relevant to operation evaluation. Therefore Cathedral recommends that all tax and legal comments be taken to your tax professional and/or legal counsel for full consultation and evaluation, before any action is taken. Cathedral Consulting Group, LLC Page 1 receipt should be issued within 72 hours of the organization’s receipt of the gift so that the donor knows that their contribution has been received and acknowledged. It is good practice to receipt any individual who makes a cash contribution regardless of the amount. An organization is required by the IRS to provide a written disclosure to any donation of $75 or more if the donor received any goods or services in exchange for the donation, such as receiving a dinner in exchange for purchasing a ticket to a special event. B. In-kind: To maintain the relationship with the donor and to fulfill IRS obligations to donors, a thank you letter should be sent as soon as possible (see sample on last page). When a charity receives an in-kind donation, the charity should never include a value of the inkind item received in the thank you letter since the donor is responsible for obtaining a proper valuation for in-kind contributions. If the IRS later disagrees with the amount of the charitable deduction taken by the donor, the donor must support the amount. Note: As with cash donations, the thank you letter must include the standard IRS language, which states in effect, “No goods or services were received in exchange for this donation.” For example, if a donor drops off a bag of clothes at a housing shelter, they cannot receive anything in exchange for this donation, such as a meal or item of clothing. C. Stock: A donor wishing to make a donation of stock must transfer the stock directly to the charitable donation, which is typically done through a broker. When the organization receives notification that stock has been received in their account, they must provide the donor with a receipt that indicates the day on which the stock was received in their account (which is often 2-3 days after the donor initiated the transfer) and the high and low price at which the stock traded that day. The organization does not provide a cash value of the stock other than listing the high/low prices per share. There are many sites where you can look up the historical high/low stock prices such as www.Investopedia.com or www.finance.yahoo.com. Enter the company’s symbol, and then click on the “history” or “historical prices” tab of the company’s stock prices. D. Professional Services: Many people assume that any gift they give to a nonprofit will be tax deductible, including time. But not all charitable contributions actually are tax deductible. Several factors go in to deciding whether a gift is tax deductible including: who the donation was given to, when it was given, the purpose, the giver’s tax situation, and regulation by the IRS. Each donor’s situation is unique. Therefore, the nonprofit should never give specific legal or tax advice. Doing so may make the organization liable if its counsel is incorrect. A volunteer for your organization can typically deduct any out-of-pocket expenses incurred during their volunteer activities with a charitable organization as well as mileage incurred for charitable purposes (currently set at $.14/mile for 2013 by the IRS). If requested, the organization must provide a receipt that indicates the expenses that were incurred by the volunteer and follow the format for a standard contribution. It is up to the individual to substantiate any and all documentation for volunteer-related deductions. Individuals who donate their time or services, even if they are professionals, are not allowed to deduct the value of this time2. (Please see IRS publication 526 for more information). 2 “IRS Publication 526: Charitable Contributions.” http://www.irs.gov/pub/irs-pdf/p526.pdf Cathedral Consulting Group, LLC Page 2 A receipt should always be provided for donations, both cash and in-kind. While a receipt may not always be necessary, they are often essential to donors for records and also provide an efficient way to thank donors for their contributions. E. Special Events: When an organization sells tickets for an event or hosts a charitable auction, it is important to remember the IRS regulations on “quid pro quo,” which essentially means that no goods or services are provided in exchange for a donation. From a practical standpoint the organization must deduct the value of anything the donor receives in exchange for a gift (e.g. dinner or gift bag) from the total amount of the ticket price in order to provide the value of the charitable donation to the donor. For example, if your organization is selling tickets to a dinner for $100, and the actual cost of the meal is $50, then you must issue a receipt indicating that the donor provided a check for $100, of which $50 is a charitable donation. If your event also includes a gift bag valued at $25, then the charitable donation drops to $25 out of the total $100 donation. If you sponsor an auction, the donor can only count the amount that is over the actual value of the item as a charitable donation. For example, if someone purchases a one-week vacation at a timeshare that is valued at $1,000, and they pay $750 for it, then they do not receive any charitable deduction, as what they are receiving (one week at a time share) is valued at more than what they paid. If the donor paid $1,500 for the same timeshare, then the $500 that is over the actual value of the items can be tax deductible. If an organization does not disclose goods or services provided in exchange for a donation, it can be subject to IRS fines of $10 per instance, up to $5,000 per event. Internal: A. Cash: Record the donation in the organization’s donor database as well as in the appropriate accounting system. Ensure that donations that were raised for a designated cause or program are properly recorded and tracked in the accounting system. B. In-kind: Determine a value of the donated item(s) for internal use. Many organizations rely on donations of food, clothing, and even space in order to run. If you did not receive these donations, particularly those critical to your program, you would have to purchase them. It is important to count the value of in-kind donations as revenue in your program. Donations should be recorded as support and are included in the revenue and support section of the activity statement. They should be recorded at their Fair Market Value (FMV) at the time of the donation. When they are used, they should be treated as expenses and recorded as such. For example, if you receive office space for free, and it is valued at $100/month or $1,200/year, you will list this as a revenue line as well as an expense line in your annual budget. Funders, particularly foundations, and major donors will want to see that you are utilizing a variety of resources, including in-kind donations. C. Stock Gifts: Every organization should have a policy on stock gifts that includes whether the stock is automatically sold or held. Most organizations choose to sell the stock as soon as it is received. The value of the stock on the day it is sold would need to be recorded as income. D. Time and Professional Services: Even though the IRS does not allow an individual to deduct the value of their time, it is a good practice for nonprofit organizations to track the total number of hours that are volunteered and to provide a general estimate of the value of this time to report to Cathedral Consulting Group, LLC Page 3 donors and stakeholders. While this information would not be added to the organization’s books, it can demonstrate to funders that the organization is maximizing the use of all resources. E. Special Events: When recording income and expenses for special events, be aware of how the IRS requires data to be reported on IRS form 990. Additional details on expenses must be provided for any single event that generates $5,000 or more in revenue or for all events if they total collected through all event is more than $15,000. Also note that events such as raffles and sweepstakes, even if they are part of a special event, are considered by the IRS to be charitable gaming activities and must be reported as such on the annual 990. Valuing In-Kind Donations When valuing cash donations, the value of the gift is the value of the cash, dollar to dollar. However, often gifts-in-kind are much more difficult to value. Generally, gifts-in-kind are valued at Fair Market Value (FMV) which is the price that the item would sell for on the open market. This is not always easy to find; therefore, some of the most common donations have generally accepted values from a few sources. While these guidelines are accurate, you should always consult your tax advisor, CPA, and IRS publications before valuing gifts-in-kind. Some companies value items independent of the IRS. These valuation types include: A. Common household goods and clothing: The Salvation Army provides a suggested guide to valuing commonly donated household items and clothing. Keep in mind that prices vary based on condition as well as geographic location of the organization. The guide can be found on The Salvation Army’s website here. B. Cars: The IRS heavily regulates the donation of cars; donors are encouraged to review the IRS publication on this so that they fully understand how they can value their donation. If your donation falls under the exception category, The Kelley Blue Book is often used to value a used car. Example of an In-Kind Receipt There are two parts to the receipt, the introductory/thank you and the receipt. [Date] [Name] [Address] [City State ZIP] Dear [Donor Name], On behalf of the students, staff and board of [Charity], we would like to extend our deepest gratitude for your recent in-kind donations, listed below. Your thoughtfulness is greatly appreciated by everyone here at [Charity]. Your contribution goes directly towards our ability to [mission of charity]. Just this year alone, we have provided [what the charity does – educate children, provide shelter to the homeless, feed the hungry]. Once again, thank you for your interest in and commitment to [Charity] as we serve [target population]. Sincerely, Cathedral Consulting Group, LLC Page 4 [Signature of CEO or Executive Director] ------------------[Name] [Title] [Email and/or Phone Number] [Name of Charity here] is a 501(c)(3) nonprofit organization. Your contribution is tax deductible to the extent allowed by law. No goods or services were provided in exchange for your generous donation. Donated Items [examples below] received on [insert date]: • Books, with a variety of titles, some for children, some religious and some for seniors. • Other items, such as a clock and bottles of lotion. Received at [list specific location, particularly if it is different from the organization’s main address/location]. Example of a Special Event Receipt [Date] [Name] [Address] [City State ZIP] Dear [Donor Name], On behalf of the students, staff and board of [Charity], we would like to extend our deepest gratitude for your participation in Save the Schools Annual Gala. This letter confirms your purchase of one ticket at $250. In exchange for your contribution, you received one dinner, with an estimated fair market value of $150. Your thoughtfulness is greatly appreciated by everyone here at [Charity]. Your contribution goes directly towards our ability to [mission of charity]. Just this year alone, we have provided [what the charity does – educate children, provide shelter to the homeless, feed the hungry]. Once again, thank you for your interest in and commitment to [Charity] as we serve [target population]. Sincerely, [Signature of CEO or Executive Director] ------------------[Name] [Title] [Email and/or Phone Number] Cathedral Consulting Group, LLC Page 5 [Name of Charity here] is a 501(c)(3) nonprofit organization. Your contribution is tax deductible to the extent allowed by law. In exchange for your contribution, you received one dinner with a fair market value of $150. Contribution received on [date]: Amount [$]: Purpose [name of special event]: Resources and Articles for Further Reading 1. “Tax Information for Charitable Organizations.” Internal Revenue Service. http://www.irs.gov/Charities-&-Non-Profits/Charitable-Organizations 2. Fishman, J.D., Stephen. Every Nonprofit's Tax Guide: How to Keep Your Tax-Exempt Status and Avoid IRS Problems. Nolo, Third Edition: November 2013. http://www.amazon.com/Every-Nonprofits-Tax-Guide-Tax-Exempt/dp/1413319297 3. “Tax Information for Contributors.” Internal Revenue Service. http://www.irs.gov/Charities-&Non-Profits/Contributors 4. “Charitable Contributions - Substantiation and Disclosure Requirements.” Internal Revenue Service. http://www.irs.gov/pub/irs-pdf/p1771.pdf In-Kind Donation Valuation Guides 1. The Salvation Army: commonly donated household goods and clothing. http://www.use.salvationarmy.org/use/www_usn20.nsf/vw-text-dynamicarrays/33CE09196410A2148825770B0054FF7A?openDocument&charset=utf-8 2. IRS Publication 561: Determining the Value of Donated Property (Rev. April 2007). http://www.irs.gov/pub/irs-pdf/p561.pdf 3. IRS Publication 4304: A Donor’s Guide to Car Donations (Rev. August 2013). http://www.irs.gov/pub/irs-pdf/p4303.pdf 4. IRS Publication 4302: A Charity’s Guide to Vehicle Donations (Rev. February 2009). http://www.irs.gov/pub/irs-tege/pub4303.pdf 5. The Kelley Blue Book. http://www.kbb.com/whats-my-car-worth/ Kimberly Reeve is a Managing Director, Michelle Fitzgerald is a former Senior Associate, and Sterling Clay is an Associate in the New York Office. Virginia Zignego is a Senior Associate in the Midwest Office. For more information, please visit Cathedral Consulting Group LLC online at www.cathedralconsulting.com or contact us at info@cathedralconsulting.com. Cathedral Consulting Group, LLC Page 6