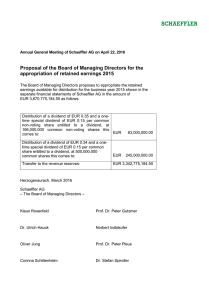

CONSOLIDATED FINANCIAL STATEMENTS 2013 IBH GROUP INA Beteiligungsgesellschaft mit beschränkter Haftung

advertisement