Convergence results for the flux identification in a scalar conservation law ∗

advertisement

Convergence results for the flux identification in a

scalar conservation law∗

François JAMES†

Mauricio SEPÚLVEDA‡

November 10, 2011

Abstract

Here we study an inverse problem for a quasilinear hyperbolic equation. We start by proving the existence of solutions to the problem which

is posed as the minimization of a suitable cost function. Then we use

a Lagrangian formulation in order to formally compute the gradient of

the cost function introducing an adjoint equation. Despite the fact that

the Lagrangian formulation is formal and that the cost function is not

necessarily differentiable, a viscous perturbation and a numerical approximation of the problem allow us to justify this computation. When the

adjoint problem for the quasilinear equation admits a smooth solution,

then the perturbed adjoint states can be proved to converge to that very

solution. The sequences of gradients for both perturbed problems are also

proved to converge to the same element of the subdifferential of the cost

function. We evidence these results for a large class of numerical schemes

and particular cost functions used in the identification of isotherms for

chromatography. They are illustrated by numerical examples.

Keywords:

Inverse problem – Scalar conservation laws – Adjoint state –

Gradient method

AMS classification: 35R30, 35L65, 65K10, 49M07

1

Introduction

In this paper, we are interested in the following inverse problem: consider the

scalar hyperbolic conservation law

∂t w + ∂x f (w) = 0,

∗ This

x ∈ IR, t > 0,

(1)

work has been partially supported by the Program A on Numerical Analysis of

FONDAP in Applied Mathematics and the Universidad de Concepción (P.I. 97.13.09-1.2 and

97.013.011-1.In).

† Mathématiques,

Applications et Physique Mathématique d’Orléans,

UMR

CNRS 6628, Université d’Orléans, B.P. 6759, F-45067 Orléans Cedex 2, FRANCE

(james@cmapx.polytechnique.fr).

‡ Departamento de Ingenierı́a Matemática, Facultad de Ciencias Fı́sicas y Matemáticas,

Universidad de Concepción, Casilla 4009, Concepción, CHILE (mauricio@ing-mat.udec.cl).

1

FLUX IDENTIFICATION IN CONSERVATION LAWS

2

together with the Cauchy data

w(x, 0) = w0 (x) ∈ BV (IR) ∩ L∞ (IR).

(2)

It is well-known that there exists one and only one entropy solution in L∞ (IR+ , BV (IR))

∩ L∞ (IR × (−∞, +∞)) of (1)-(2) (see [6], [18]), and we emphasize the fact that

the unique entropy solution to (1) depends continuously (in a sense which we

shall precise) on the smooth function f by denoting it wf . The question we

address is whether, an observation wobs at time T > 0 being given, one can

identify the non linearity f such as wf at time T is as close as possible to wobs .

It is quite natural to formulate this problem more or less like an optimal

control problem: for any function v : IR → IR we define a cost function J(v),

and we look for an f solving

min J(wf (., T )),

f

(3)

thus giving a precise meaning to the sentence “as close as possible”. Therefore

we are led to the constrained optimization problem of minimizing J(w(., T ))

under the constraint for w to satisfy the partial differential equation (1)-(2).

This problem can be viewed as well as an unconstrained minimization problem:

˜ ) = J(wf ), then problem (3) boils down to minimizing J˜ on a

if we set J(f

suitable set of functions.

In theory, this inverse problem is in general ill-posed in uniqueness when

there are discontinuities in the solution. For instance, a well-known undesirable

case appears when we try to identify f over a shock wave with a propagation

speed equal to σ : there are infinitely many functions f giving the same entropic

solution wf of (1)-(2) equal to the shock wave (see [4] for more details). Yet,

as far as applications are concerned some interesting practical problems can be

found: it is possible to resolve the identification of f (or “a part of f ”) via a

˜ This

gradient technique in order to compute numerically the minimum of J.

was achieved in a preceding paper [9] in which we considered the identification problem arising from a model of diphasic propagation in chromatography.

Therefore we dealt with a system of conservation laws, and we obtained successful numerical results because the function f was given a precise analytic form,

so the minimization occurred on IRn , and we chose adequate criteria for the cost

function linked to the physical parameter of the problem.

˜

The classical gradient technique used in order to obtain the gradient of J,

consists in writing a Lagrangian formulation for the constrained problem and

in introducing the adjoint state. This has to be done at two levels.

We first consider a formal level, that is we take a solution of the continuous

equation (1), and perform the computations. We obtain a backward linear

hyperbolic equation for the adjoint state. The trouble is that this equation is

ill-posed as soon as the solution of (1) is not smooth – which is of course the case

in most of the applications. This is related to the fact that the inverse problem

is ill-posed in uniqueness when there are discontinuities in the solution. Thus,

in general, the computation of the gradient of J˜ remains formal. Furthermore,

it is easy to find some counterexamples where the gradient does not exist.

FLUX IDENTIFICATION IN CONSERVATION LAWS

3

On the other hand, we can perform the same computations at a discrete

level, that is when both the equation (1) and the cost function J are discretized.

This introduces a “discrete adjoint state” which we call adjoint scheme, and we

˜ which is well-defined. Thus we

obtain the gradient for the discretization of J,

are able to perform numerical computations, using standard conjugate gradient

techniques, and the numerical evidence is that the method seems to converge

(see [9], Section 5 and [11] for application on real data).

The aim of this paper is to interprete and justify the convergence of the

method in the scalar case, and in a particular case, namely when the solution

of the adjoint state is Lipschitz continuous. We shall consider two modified

problems : first we add a viscous term to (1), then we turn to the discretized

problem. In both cases, we prove that the perturbed adjoint states converge

to the solution of the original problem. That enables us to pass to the limit

in the approximation of the gradient, and we prove that both approximations

tend to the same limit. This limit is not necessarily the gradient of the cost

function because the gradient does not exist a priori. In fact, we also prove by

˜

means of convexity hypotheses that it is an element of the sub-differential of J.

This result gives an interpretation of the formal computation of the gradient

for continuous cost functions including some cases when the gradient does not

exist.

Therefore the paper is organized as follows. First we precisely state the

problem, in particular concerning the cost function we consider, which is not

the standard least square function. Then we consider the identification problem

for a parabolic regularization of the conservation equation, and in particular, we

prove the differentiability of the cost function. We also prove the convergence of

the sequence of the perturbed gradients to an element of the sub-differential of

˜ Finally we prove that we can obtain the same element of the sub-differential

J.

via a discretized problem and for a large class of numerical schemes, and we

illustrate these results by a numerical application on experimental data.

2

2.1

The identification problem

The cost function

A classical example of cost function J arises in the well-known output least

square method (see [4] for instance) :

Z

1

|w(x, T ) − wobs (x)|2 dx.

(4)

J0 (w) =

2 x∈IR

For practical reasons, in [9] the following modified cost function Jρ was used :

ρ

Jρ (w) = J0 (w) + |µ1 w(·, T ) − µ1 (wobs )|2 ,

2

(5)

4

FLUX IDENTIFICATION IN CONSERVATION LAWS

where ρ is a constant parameter to be adjusted, and where µ1 (X) is the first

moment of the function X : IR → IR:

Z

µ1 (X) =

xX(x)dx.

(6)

IR

Roughly speaking, the advantage of Jρ over J0 is that it is more sensitive to the

localization of the observed signal on the x-axis, whereas J0 essentially takes

into account the shape of the signal, independently of its localization.

Notice that we shall always consider initial data with compact support so

that, by the finite velocity of propagation, the solution at any time t > 0 will

also have a compact support. Thus all the integrals in the definitions of J0 and

of Jρ have a meaning as soon as w is in L∞ (IR).

For practical reasons, what follows is essentially focused on the study of

criteria (4) or (5)-(6).

2.2

Existence and Lipschitz continuous dependence

We can assure the existence of at least one solution f of our identification problem (3) when we search it in a compact of the Lipschitz continuous functions.

In fact, this is a consequence of the following theorem, the proof of which is

contained in a paper by B. Lucier ([13]):

Theorem 1 The application f 7→ wf is Lipschitz continuous from the space of

Lipschitz functions to L1 , that is

kwf (., t) − wg (., t)kL1 ≤ tkf − gkLip kw0 kBV .

(7)

Corollary 1 The function Je is Lipschitz continuous from Lip(IR) to IR+ .

Proof. Concerning the function J0 , the estimate follows immediately from

the L∞ estimate which holds uniformly in g:

∀t > 0,

kwg (., t)kL∞ ≤ kw0 kL∞ .

(8)

Indeed we have

|J0 (wg ) − J0 (wf )| ≤

≤

1

2

Z

|(wg − wf )(x, T )| |(wg + wf )(x, T ) − 2wobs (x)| dx

IR

max(kw0 kL∞ , kwobs kL∞ ) kwg (, .T ) − wf (., T )kL1

by Hölder’s inequality. The result follows by (7). Now for the momentum

criterion, if we assume all the supports included in [−L, L] for some L large

enough, we get, using again (8):

|J1 (wg ) − J1 (wf )| ≤

≤

1

|µ1 (wg (., T )) − µ1 (wf (., T ))| |µ1 (wg + wf (., T )) − 2µ1 (wobs )|

2

L3 max(kw0 kL∞ , kwobs kL∞ ) kwg (, .T ) − wf (., T )kL1 .

FLUX IDENTIFICATION IN CONSERVATION LAWS

5

By considering a minimizing sequence for Jρ , we easily deduce from Corollary

1 the following existence result:

Corollary 2 If f ∈ F a compact set of the Lipschitz continuous functions, then

there exists at least one solution of the identification problem (3), with the cost

function defined by (4) or (5)-(6).

Remarks. The compactness of the set F is a necessary hypothesis, but it

is not a restrictive condition for a lot of practical identification problems : the

function f can have a precise analytic form so that the minimization occurs on

a bounded subset of IRn (for instance, see [9]). Another way to obtain Lipschitz

compactness is to seek f for instance in W 2,∞ (IR).

We cannot ensure the uniqueness of the solution in the corollary 2 for the

reasons exposed in the introduction. Obviously, we can try to modify the cost

functions to obtain a strictly convex functional and, for instance, search the flux

f with minimal W 2,∞ (IR) norm. Yet in general, this is an arbitrary mathematical condition. Thus we prefer to deal with the cost functions defined by (4),

(5) and (6), which have a realistic physical sense, and to leave the uniqueness

problem as an open problem.

2.3

Remarks on differentiability

˜ ) = Jρ (wf ) with

Since we are concerned with the problem of minimizing J(f

respect to f , differentiability is of course of crucial importance: optimality con˜ the problem is open in

ditions, gradient algorithms rely on it. For the function J,

general, and we are going to point out precisely the difficulties. These will come

of course from the operator f 7→ wf , since the functions J0 and J1 are smooth

convex functions. Let us first consider this operator in the nice case where all

the involved functions are smooth. Indeed, if w0 ∈ C 1 (IR) and f ∈ C 1 (IR), then

there exists T > 0 such that wf ∈ C 1 (IR × [0, T ]). Let us use the notations of

the calculus of variations, denoting by δw the variation of wf corresponding to

some variation δf of f . Then δw has to solve

∂t δw + ∂x [f ′ (wf )δw] + ∂x [δf (wf )] = 0

(9)

δw(., 0) = 0.

Under the above assumtions, we are faced with a standard linear conservation

equation with smooth coefficients. Actually, applying the inverse functions theorem to

F

: C 1 (IR × [0, T ]) × Lip(IR)

(w, f )

→ C 0 (IR × [0, T ]) × C 0 (IR)

7→ (∂t w + ∂x f (w), w(., 0) − wobs )

6

FLUX IDENTIFICATION IN CONSERVATION LAWS

we can prove that f 7→ wf is differentiable in a strong sense from Lip(IR) to

C 1 (IR × [0, T ]). Thus J˜ is also differentiable, with

Z

J˜′ (f )δf

=

(wf (x, T ) − wobs (x))δw(x, T ) dx +

(10)

IR

+ ρ (µ1 (wf (., T )) − µ1 (wobs )) µ1 (δw(., T )).

This by the way justifies in this case the integrations by parts we perform in

the next section.

We would like to point out now that, if wf happens to be discontinuous, then

the resolution of (9) is much more difficult. Indeed it becomes a conservation

law with discontinuous coefficient (f ′ (wf )) and a measure-valued source term

(∂x [δf (wf )]). The solution has therefore to be seeked in the class of measures on

IR, generalizing the results obtained by Bouchut and James [2, 3] in the absence

of source term. Up to now, this is possible only if f is convex. In this context,

it is reasonable to hope for some very weak differentiability result, the involved

topology being the usual weak convergence of measures. The general case of a

non convex f is still completely open.

However, even the differentiability of f 7→ wf does not settle the problem

˜ ). Indeed since δw is a measure, (10) is meaningful if wf (., T ) − wobs ∈

for J(f

1

L (δw(., T )), which is a priori not obvious. In the same way, µ1 (δw(., T )) has

to be defined. We refer to the next section for an explicit example and further

comments.

For all these reasons, we leave the problem of a rigorous differentiation of

J˜ (and possibly the choice of theoretically more convenient cost functions) to a

future work. We focus in the sequel on the study of two approximated problems

where all the involved quantities are well-defined. We prove when it is possible

the convergence of these problems to the original one. We begin by a formal

˜ as it was done in [9]. The basic tool for

computation of the gradient of J,

that is to consider the constrained minimization problem and its Lagrangian

formulation.

2.4

Lagrangian formulation and adjoint problem

In [9] and [17], we formally obtain the gradient through the following Lagrangian

formulation for the constrained minimization problem:

def

L (w, p; f ) = J(w) − E (w, p; f ) ,

(11)

where E (w, p; f ) is a weak form of (1), defined by

E (w, p; f ) = −

Z

0

TZ L

0

(w∂t p + f (w)∂z p) +

Z

t=T

wp −

Z

t=0

w0 p.

(12)

FLUX IDENTIFICATION IN CONSERVATION LAWS

7

We are interested in cancelling ∂L . For that purpose, we take p solution to the

∂w

following backward adjoint problem

′

x ∈ IR, t ≤ T,

∂t p + f (wf )∂x p = 0,

(13)

p(x, T ) = pT (x),

where f ′ (wf ) represents the derivative of f with respect to w evaluated on the

solution wf of (1). The function pT depends on J, w, and wobs . More precisely,

we have

Z

pT δw = Dw J(wf )δw,

∀δw ∈ D(IR),

(14)

IR

where Dw Jδw represents the derivative of J in the direction δw. The problem

(13) is called the adjoint problem associated to the direct problem (1).

Thus we can compute the gradient of J˜ by the formula

Z T Z +∞

˜ )δf =

DJ(f

∂x p δf (wf )dxdt

(15)

0

−∞

where p is solution of equation (13).

Remark. Formula (15) is a formal result, since the derivative of function Je

does not necessarily exist, as a rule. For instance, consider the entropic solution

of the Riemann problem

1

if x ≥ kt,

wk (x, t) =

0

otherwise,

for the Burger’s equation – f (w) = kw2 – and suppose wobs (x) = wk0 (x, T ) for

some given k0 . Then we have that the cost function given by the criterion of

the norm L2 (4) is equal to

J˜0 (k) = J0 (wk ) = T |k − k0 |,

(16)

which is not differentiable in k0 . Moreover the backward equation defining p is

ill-posed as soon as discontinuities occur in the solution of the direct problem:

actually the solution is not uniquely defined by the characteristics.

If we assume that we are in the neighbourhood of a minimum, the function J˜

is locally convex, so the subdifferential ∂ J˜ is a non-empty set. We may hope that

˜ ) defined by (15) is an element of ∂ J˜ when the adjoint equation is ill-posed.

DJ(f

We are not going to answer this question here. We will restrict ourselves to the

particular case where there exists a smooth solution to the adjoint equation.

In this case we shall study whether (15) is well-defined and whether it is an

element of the subdifferential. First, we give an existence result for Lipschitz

solutions to the adjoint problem (13), then, conditions for the uniqueness.

Definition 1 The function a(x, t) verifies the One-Side-Lipschitz-Continuous

condition (OSLC) when there exists a function m ∈ L1 (0, T ) such as

+

a(x, t) − a(y, t)

def

+

≤ m(t)

(17)

L (a(x, t)) = ess sup

x−y

x6=y

FLUX IDENTIFICATION IN CONSERVATION LAWS

8

In other words, the condition (OSLC) means that the function a(·, t) must be

Lipschitz continuous for all t, when a(·, t) is increasing, and it allows decreasing

jumps a(x−, t) > a(x+, t). This condition has been used by several authors,

e.g. Oleinik [14], Conway [5], Hoff [8], Tadmor [19] to prove the existence

of at least one Lipschitz continuous solution to the adjoint problem (13), when

pT ∈ W 1,∞ (IR). A refined version of Oleinik’s entropy condition (Hoff [8]) states

that f ′ (w) verifies (OSLC) condition when w accepts only entropic shocks as

discontinuties and when f is convex. We need this result to make sense out

of solving p by the characteristics method. So far, we do not know a general

existence result for any f . The problem with this result is that its solution is

ill-posed in uniqueness : for instance, if we assume that f ′ (wf )(x, t) = −sign(x),

and kpT kW 1,∞ (IR) > 0, then it is easy to verify that

p(x, t) =

pT (x − sign(x)(T − t))

ϕ(t + |x|)

when t + |x| ≥ T,

otherwise ,

are Lipschitz continuous solutions of adjoint problem (13), for any ϕ(t) Lipschitz

continuous function such that ϕ(T ) = pT (0).

We recall briefly here the definition of the so-called “reversible solutions”

introduced in [2, 3], for which uniqueness holds. First define the set E of “exceptional solutions” as the space of all the Lipschitz continuous solutions of (13)

with pT = 0. Next, we introduce the open set called “support of exceptional

solutions”:

def

V = {(t, x) ∈]0, T [×IR | ∃pe ∈ E, pe (t, x) 6= 0},

(18)

The following result is obtained in [3]:

Theorem 2 Let p a Lipschitz continuous solutions of (13). Then, both properties are equivalent

(i) p is locally constant in V ;

(ii) there exists p1 and p2 in Liploc ([0, T ]×IR), verifying ∂t pi +f ′ (w)∂x pi = 0

and ∂x pi ≥ 0, such as p = p1 − p2 .

Furthermore, for all pT ∈ W 1,∞ (IR) there exist one and only one Lipschitz

continuous solution p of (13) verifying one of these properties and the following

estimate

(Z

)

T

kp(·, t)kW 1,∞ (IR) ≤ kpT kW 1,∞ (IR) · exp

m(τ )dτ

∀t ≤ T.

(19)

t

This function p is called the reversible solution of (13).

Remarks. According to property (i) of theorem 2, we can choose a constant

for p in each fan-wise set defined by all the characteristic straight lines which

converge to a discontinuity of w. This constant is equal to the value of pT (x),

where (x, T ) is a point in the discontinuity of w. Property (ii) is a monotonicity

property of the reversible solution.

FLUX IDENTIFICATION IN CONSERVATION LAWS

9

Choosing the reversible solution in counterexample (16) is equivalent to

choosing the characteristic element of the subdifferential of J˜0 (k0 ) equal to zero.

This is not an arbitrary choice. At the limit, we will see that we obtain an element of the subdifferential of J˜ characterized by the reversible solution, when

we consider viscosity approximation and some classical numerical schemes.

When we consider the cost function (4) or (6), the hypothesis pT ∈ W 1,∞ (IR)

is equivalent to (w(·, T )−wobs ) ∈ W 1,∞ (IR). In practice, this is a very restrictive

hypothesis in the sense that it means a regular solution w, or at least a solution

in which the shocks at t = T are cancelled with the shocks of the observation

wobs . When w is regular (without shocks), it is clear that we do not need the

notion of reversible solution: in this case we have seen that the cost function

is differentiable. The resolution of (13) when pT ∈

/ W 1,∞ (IR) remains an open

problem.

3

Artificial viscosity

We introduce the classical viscous regularization of the equation (1):

2

wε ,

x ∈ IR, t > 0

∂t wε + ∂x f (wε ) = ε∂xx

(20)

wε (x, 0) = w0 (x),

It is well-known that (20) admits a unique smooth solution which approaches

the entropy solution of (1) in the following sense (see e.g. Smoller [18]):

Theorem 3 We suppose that w0 ∈ BV (IR). Then,

(i) Problem (20) has a solution wε (·, t) ∈ BV (IR) for all t > 0. This solution is

C 1 on IR × (0, ∞). Furthermore, for all t > 0,

kwε kL∞ (IR) ≤ constant,

T V (wε (·, t)) ≤ T V (w0 )

(ii) The only accumulation point in L∞ (IR × (0, +∞))-weakly∗, and L1loc (IR ×

(0, +∞))-strong, of the sequence wε is the entropic solution w of (1).

Now we shall limit ourselves to the (restrictive) case where the final data

for the adjoint state is in W 1,∞ (IR), and consider the following minimization

problem

min Jeε (f ),

where J ε (f ) = Jρ (wfε )

(21)

f

wfε

and

is the solution of the parabolic problem (20), and the cost function Jρ

is defined by (5).

We are going to proceed in three steps. First we compute the exact derivative of the function Jeε . Then we shall prove that the adjoint equation is wellposed, which will give a characterization of the derivative. Finally, we are going

to prove the convergence of the adjoint state and of the derivative of the viscous

problem to the corresponding quantities for the hyperbolic problem, when ε

tends to 0.

FLUX IDENTIFICATION IN CONSERVATION LAWS

3.1

10

Derivative of the viscous cost function

We want to determine the Gateaux-derivative of Jeε . We shall prove that the

directional derivative

Jeε (f + hδf ) − Jeε (f )

,

(22)

DJeε (f )δf = lim δh Jeε (f ) = lim

h→0

h→0

h

exists for all Lipschitz continuous function δf (δf is called a Lipschitz direction).

We have

Proposition 1 Let wfε be the solution of the viscous problem (20). We suppose

that the flux f = f (wε ) is of class C 1 and Lipschitz continuous with respect to

wε with a Lipschitz constant CLip . Then the limit (22) exists for all Lipschitz

direction δf (which we can suppose with the same Lipschitz constant CLip ). It

is characterized by

DJeε (f )δf = Dw Jρ (wfε )w1ε ,

(23)

where w1ε is the solution in L2 (0, T, L2(IR)) ∩ C 1 (IR × (0, +∞)) of the following

linear parabolic problem

2

w1ε ,

∂t (w1ε ) + ∂x f ′ (wfε )w1ε + δf (wfε ) = ε∂xx

(24)

ε

w1 (x, 0) = 0,

Proof. Recall that Jρ = J0 + ρJ1 . Then we can write

Z

ε

ε

wfε (x, T ) − wobs (x) w1ε (x, T )dx,

D

J

(w

)w

=

w 0 f 1

IR

D J (wε )wε = µ wε (·, T ) − µ (wobs ) µ wε (·, T ),

w 1

1

1

1

f

1

f

1

(25)

and we remark that

Z wε + wε

f

fh

ε

obs

δh J0 (wf ) =

(x, T ) − w (x) δh wε (x, T )dx

2

IR

!

ε

ε

µ

(w

(·,

T

))

+

µ

(w

1

1

h (·, T ))

f

f

− µ1 (wobs ) µ1 (δh wε (·, T )),

δh J1 (wfε ) =

2

(26)

wfε h − wfε

h

ε

where f = f + hδf and δh w =

.

h

We first prove the convergence of the derivative of the L2 -criterion:

δh Je0 (wfε ) → Dw J0 (wfε )w1ε ,

when h → 0.

(27)

We have that wfε and wfε h are solutions of the parabolic problem (20) with the

respective non-linear flux f and f h . Thus, if we take the difference between the

equation in wfε and the equation in wfε h , we deduce that δh wε is solution of

!

f h (wfε h ) − f h (wfε )

ε

ε

2

∂t δh w + ∂x

+ δf (wf ) = ε∂xx

δh w ε .

(28)

h

11

FLUX IDENTIFICATION IN CONSERVATION LAWS

We multiply this equation by δh wε and we integrate by parts. Using classical

estimate arguments and the Gronwall lemma, we prove

kδh wε (·, t)kH 1 ≤ C(ε) ∀t ∈ (0, T ),

(29)

where C(ε) is a constant which does not depend on h. Thus, up to a subsequence, there exists w1ε (·, t), such that

δh wε (·, T ) ⇀ w1ε (·, T ) in H 1 (IR) − weak

when h → 0.

We can easily verify that wfε h (·, T ) → wfε (·, T ) in L2 (IR)−strong when h → 0.

Hence we deduce (27).

Next we prove the convergence of the derivative of the first moment criterion:

δh Je1 (wfε ) → Dw J1 (wfε )w1ε ,

when h → 0.

(30)

We deduce from the compact support of w0 , and from the maximum principle applied to the equations (20), (24) and (28) that the functions |wfε (·, T )|,

|wε (·, T )|, |δ wε (·, T )| and |wε (·, T )| are bounded by a function g(x) = C e−r|x|

fh

h

1

where C, r are constants which depend only on T and kw0 kL∞ , and thus are

independent of h. We obtain that

|µ1 (δh wε (·, T )) −

µ1 (w1ε (·, T ))| ≤

Z

Z R

ε

ε

|x (δh w − w1 ) (x, T )|dx +

−R

|xg(x)|dx.

|x|>R

Using the convergence L2 -weak of δh wε (·, T ) we have that the first term of the

right hand side converges to 0. The second term uniformly converges to 0 in h,

when R → ∞. This implies the convergence µ1 (δh wε (·, T )) → µ1 (w1ε (·, T )),

when h → 0. In the same way, and using the convergences L2 -strong of

wfε h (·, T ), we have that µ1 (wfε h (·, T )) → µ1 (wfε (·, T )), when h → 0. From

these convergences of the moments, we deduce the result (30).

Finally, we prove that w1ε is the solution of (24). Using (29) and the compact

1

injection Hloc

(IR) ֒→ L2loc (IR), we have the following strong convergence

δh wε (·, t) → w1ε (·, t) in L2loc (IR) − strong,

when h → 0.

(31)

We multiply the equation (28) by a test function ϕ ∈ C01 ([0, +∞) × IR) and we

integrate by parts. Hence, by passing to the limit in (28), we obtain that w1ε

is a weak solution of (24). Therefore, by the existence and uniqueness of the

solution of the linear parabolic problem (24), we have that function w1ε is the

strong solution in L2 (0, T, L2 (IR)) ∩ C ∞ (IR × (0, +∞)) of this equation.

3.2

Viscous adjoint problem

We showed that the Gateaux derivative of Jeε (f ) is well-defined for cost function

Jρ defined by (5). Now we shall use the Lagrangian formulation in order to give

12

FLUX IDENTIFICATION IN CONSERVATION LAWS

a characterization of this derivative. First we define the weak form associated

to (20) by

ε

ε

ε

E (w , p , f )

def

=

Z

T

Z

+∞

(wε ∂t pε + f (wε )∂x pε − ε∂x wε ∂x pε )

Z

Z

+

w ε pε −

w ε pε ,

−

0

−∞

t=0

t=T

and the Lagrangian by Lε (wε , pε , f ) = J (wε ) − E ε (wε , pε , f ), where pε is a

regular function in (x, t). We take pε equal to the solution of the following

backward parabolic equation (called viscous adjoint problem):

2 ε

p ,

x ∈ IR, t < T

∂t pε + f ′ (wε )∂x pε = −ε∂xx

(32)

ε

p (x, T ) = pT (x),

where the final condition pT is defined by (14). In this case, the derivative of

the Lagrangian with respect to wε is equal to zero, and the Gateaux derivative

of the cost function is characterized by

DJeε (f )δf =

Z

0

T

Z

+∞

−∞

∂x pε δf (wfε ).

(33)

Equation (32) is a parabolic linear equation, and it is known that it only admits

one solution in L2 (0, T, L2 (IR)) ∩ C 1 (IR × (0, ∞)) which depends on wε .

On the other hand, if β ≥ f ′′ ≥ α > 0, we can prove the following (OSLC)

estimate (see [19]) by a maximum principle argument applied on the equation

(20):

βL+ w0

+

′

ε

= m(t) ∈ L1 (δ, T ),

∀δ > 0.

(34)

L (f (w (x, t))) ≤

1 + αtL+ (w0 )

From this result, we shall deduce BV and W 1,∞ estimates on the adjoint state.

Theorem 4 We consider the solution pε (x, t) of linear parabolic problem (32),

with pT ∈ W 1,∞ (IR)∩BV (IR). We suppose β ≥ f ′′ ≥ α > 0, with α, β constants

independent of w. Then (x, t) 7→ f ′ (wf (x, t)) verifies the (OSLC) condition, and

kpε (·, t)kL∞ (IR)

ε

k∂x p (·, t)kL1 (IR)

k∂x pε (·, t)kL∞

≤ kpT kL∞ (IR) ,

(35)

T

≤ kp kBV (IR) ,

≤ kpT kW 1,∞ · exp

(Z

T

m(T − τ )dτ

t

for all t ≤ T , where m ∈ L1 (0, T ) is the function defined in (34).

)

(36)

,

(37)

FLUX IDENTIFICATION IN CONSERVATION LAWS

13

Proof. Estimates (35) and (36) are classical results of the theory of nonlinear hyperbolic equations, and the proofs can be found in [12] and [6]. The

proof of the estimate (37) is very similar to the arguments used by Tadmor [19].

Let us recall them briefly.

We consider p and pε solutions to the problems (13) and (32) respectively.

Let q ε (x, t) = pε (−x, T − t) and ψε (x, t) = ∂x q ε (x, t). We differentiate equation

(32), and we notice that the function ψε verifies

∂t ψε + f ′ (wε (−x, T − t))∂x ψε =

2

− (∂x f ′ (wε (−x, T − t))) ψε + ε∂xx

ψε

(38)

Let λ ≥ 2 be an even integer. We multiply (38) by λψελ−1 and we integrate

by parts. We obtain

Z

∂f ε

d

λ

∂x

kψε (·, t)kLλ = − (λ − 1)

(w (−x, T − t)) ψελ dx

dt

∂w

x∈IR

Z

(∂x ψε )2 ψελ−2 dx.

(39)

− ελ(λ − 1)

x∈IR

Using the (OSLC) inequality (34) and the Gronwall lemma in the equation (39),

we deduce ∀t ≤ T

(

)

Z

λ−1 T

kψε (·, t)kLλ ≤ kψε (·, 0)kLλ · exp −

m(T − τ )dτ, .

(40)

λ

t

We pass to the limit when λ tends to +∞ in (40). By the definition of ψε , we

deduce (37).

3.3

Convergence of the method

Now we prove that the artificial viscosity method converges in the sense that

the sequences wε and pε converge respectively to the entropy solution of (1) –

which is logical – and to the reversible solution of the adjoint equation. Moreover

the sequence of the derivatives of Jeε also converges towards an element of the

e Using these BV and W 1,∞ estimates we have the following

subdifferential of J.

convergence result concerning the adjoint state:

Theorem 5 We consider the solution pε (x, t) of the linear parabolic problem

(32). We suppose that the flux f satisfies β ≥ f ′′ ≥ α > 0, and pT a function

of W 1,∞ (IR) ∩ BV (IR). Then

pε → p

uniformly in Ω̄,

(41)

where Ω = ω × (0, T ), ω is a compact of IR, and p is the reversible solution of

(13) given by the theorem 2.

FLUX IDENTIFICATION IN CONSERVATION LAWS

14

Proof. The functions pε and ∂x pε are bounded in L∞ (by (35) and (37)).

We can extract a subsequence, still denoted by pε , and we have

pε (·, t) ⇀ p(·, t)

in W 1,∞ (IR) − weak∗,

(42)

By the Rellich-Kondrachov theorem (see R. Adams [1]) we deduce the strong

convergence in C 0,α (ω̄) for all 0 < α < 1, and ω compact set of IR, and using a

classical diagonalization argument (see for instance [6]), we obtain the uniform

convergence in Ω̄.

Now, in order to prove that p is a Lipschitz continuous solution of (13), we

multiply the backward parabolic equation (32) by a test function ϕ ∈ C0∞ (IR

× (0, +∞)), and we integrate by parts. We have

Z ∞Z

{pε ∂t ϕ − f ′ (wε )∂x pε ϕ − ε∂x pε ∂x ϕ} dxdt

0 = −

IR

Z0

T

p (x)ϕ(x, 0)dx.

(43)

−

IR

On the other hand, multiplying equation (32) by p(·, t), integrating by parts,

and using Gronwall’s lemma, we deduce that

1

ε 2 k∂x pε kL2 (IR×(0,T )) ≤ C,

(44)

where C is a constant independent of ε. That implies

2 ε

ε∂xx

p → 0,

in L2 (0, T, H −1 (IR)) − strong.

(45)

Now, we know by Theorem 3 that wε → w in L1loc (IR × (0, +∞))-strong, and

by Lebesgue’s dominated convergence theorem we have f ′ (wε ) → f ′ (w), in

L1loc (IR × (0, +∞)) − strong. Using the convergence W 1,∞ -weak∗ of pε (42), we

deduce

f ′ (wε )∂x pε ⇀ f ′ (w)∂x p in D′ (IR × (0, +∞)).

(46)

Using convergence results (45), (46), and the uniform convergence of pε , we let

ε → 0 in (43). We obtain

Z ∞Z

Z

′

pT (x)ϕ(x, 0)dx.

(47)

0=−

{p∂t ϕ − f (w)∂x pϕ} dxdt −

0

IR

IR

Thus the limit of pε is solution of the backward transport equation (13) in the

sense of distributions. In keeping with the W 1,∞ −weak∗ convergence (42), we

obtain that the limit p verifies p(·, t) ∈ W 1,∞ (IR), ∀t ≤ T . On the other hand,

by letting ε → 0 in (37), we obtain inequality (19).

In order to prove the convergence of the whole sequence pε , we will prove

that the limit of any converging subsequence is the unique reversible solution,

which we note pr . For that, we suppose that pε → p, and using the definition

(18) of the support of exceptional solutions, at first we have

p = pr

a.e. (x, t) ∈ IR × (0, T ) \ V,

(48)

15

FLUX IDENTIFICATION IN CONSERVATION LAWS

We set ψε (x, t) = ∂x pε (−x, T − t) and ψr (x, t) = ∂x pr (−x, T − t). Then, we

substract the equation (13) from (32) and we differentiate with respect to x.

We obtain

∂t (ψε − ψr ) = −∂x (aε (ψε − ψr )) − ∂x ((aε − a)ψr ) + ε∂xx ψε ,

where aε = f ′ (wε (−x, T − t)) and a = f ′ (w(−x, T − t)). We multiply this last

equation by 2(ψε − ψr ), and we integrate by parts. Using the (OSLC) inequality

(34), we deduce

o

d n

kψε (·, t) − ψr (·, t)k2L2 (IR)

dt

+ εk∂x ψε (·, t)k2L2 (IR)

≤ m(T − t)kψε (·, t) − ψr (·, t)k2L2 (IR)

Z +∞

(aε − a)(ψε − ψr )∂x ψr dx (49)

−

−∞

+∞

−

Z

−ε

(∂x aε − ∂x a)(ψε − ψr )ψr dx

−∞

Z +∞

−∞

2

∂xx

ψ ε ψr dx

From (42), (41), (45) and (46), we have that the 2nd and 4th terms on the right

hand side converge to 0 when ε → 0. On the other hand, from property (i) of

theorem 2 we have that ψr = 0 in Vt = {x | (−x, T − t) ∈ V}, and using the

equality (48), we deduce

Z

+∞

(∂x aε − ∂x a)(ψε − ψr )ψr dx =

−∞

Z

(∂x aε − ∂x a)(ψε − ψr )ψr dx → 0,

x∈IR\Vt

when ε → 0. Then, the 3rd term on the right hand side converges to 0. We can

pass to the limit in (49) and using Gronwall’s lemma, we obtain lim ψε = ψr

ε→0

and consequently p = pr .

Remark. Another way to prove this last result is to make use of the characterization (ii) of theorem 2. Indeed standard arguments allow us to prove that

if ∂x pT ≥ 0, then ∂x pε ≥ 0. Now, for any final data p we rewrite pT = pT1 − pT2 ,

with ∂x pT1 = (∂x pT )+ and ∂x pT2 = (∂x pT )− . We denote by pεi the solution of

(32) with final data pTi . Therefore we have pε = pε1 − pε2 , with ∂x pεi ≥ 0. We

know that pε → p, pεi → pi with ∂x pi ≥ 0, and pi solution of (13). Thus p is

reversible. A similar monotonicity argument will be used for numerical schemes.

Now we turn to the convergence of the derivative. A fundamental consequence of the convergence of the solution of the adjoint problem with artificial

viscosity is the convergence of DJeε when ε → 0. More precisely, we have

Theorem 6 Let Jeε : f 7→ J(wfε ) be the cost function (21) defined for all Lipschitz continuous function f , with wfε solution of the parabolic problem (32),

FLUX IDENTIFICATION IN CONSERVATION LAWS

16

and assume that w0 has compact support. We suppose that the flux f satisfies

β ≥ f ′′ ≥ α > 0, and pT a function of W 1,∞ (IR) ∩ BV (IR). Then we have, if

wf is the entropy solution of (1), and pf the reversible solution of (13),

Z T Z +∞

DJeε (f )δf →

∂x pf δf (wf )dxdt,

when ε → 0,

(50)

0

−∞

for all Lipschitz direction δf .

Proof. From theorem 5, and the continuity of δf , we obtain the following

result

δf (wfε ) → δf (wf ), in L1loc (IR × (0, +∞)) − strong,

(51)

kδf (wfε )kL∞ (IR×(0,+∞)) ≤ C,

for some constant C independent of ε. Let θ ∈ C0∞ (IR × (0, +∞)). In keeping

with the convergence W 1,∞ -weak of pε (42), and using (51), we obtain

Z T Z +∞

Z T Z +∞

θ∂x pεf δf (wfε )dxdt →

θ∂x pf δf (wf )dxdt

(52)

0

−∞

0

−∞

0

By hypothesis, w has a compact support. It is known that for finite propagation velocity, the function [∂x pf ]δf (wf ) stays in a compact support, for

T < ∞ (see Kružkov [12]). We have

Z T Z +∞

∂x pδf (wf )| ≤

|DJeε (f )δf −

−∞

R

0

Z

T

0

+

Z

Z

0

−R

T Z

|∂x pεf δf (wfε ) − ∂x pf δf (wf )|

|x|>R

|∂x pεf δf (wfε )|

(53)

for R large enough. Hence, by (52), the first term of the right hand side in (53)

converges to 0 when ε → 0, for all R large enough.

Let us prove the convergence of the second term. We deduce from the

compact support of w0 and from the maximum principle applied to the linear parabolic equation (32) that |pε (x, t)| ≤ C e−r|x| , where C, r are constants

which depend only on T and kw0 kL∞ , and thus are independent of ε. We deduce

that the second term of the right hand side of (53) uniformly converges to 0 in

ε, when R → ∞. This concludes the proof of (50).

e ) exists, then DJ(f

e ) is characterized by (15), and we

If the derivative of J(f

e )δf , when ε → 0. The troudeduce from the theorem 6 that DJeε (f )δf → DJ(f

e Nevertheless,

ble is that we have no result concerning the differentiability of J.

e

since we are interested in the behaviour of J near a minimum, we can assume

that Je is convex in a neighborhood of this point. Therefore, we can define its

e ).

subdifferential ∂ J(f

FLUX IDENTIFICATION IN CONSERVATION LAWS

17

Corollary 3 Assume that Je is a minimum at f , and that Je and Jeε are convex

in a neighborhood of f for all ε. Then, under the hypotheses of theorem 6,

˜ ) of J(f

e ), when

DJeε (f )δf converges to an element of the subdifferential ∂ J(f

ε → 0, that is,

Z T Z +∞

e )∋

∂ J(f

∂x pf δf (wf )dxdt.

0

−∞

Proof. From the definition of convexity we have

DJeε (f )f − Jeε (f ) ≥ DJeε (f )ν − Jeε (ν),

for all Lipschitz continuous function ν. We apply theorem 6, and we pass to the

limit when ε → 0. We obtain

Z T Z +∞

e ) − J(ν).

e

[∂x pf ] [(f − ν)(wf )] dxdt ≥ J(f

0

−∞

That is a characterization of the subgradient for convex functions (see Rockafellar [15]). Thus, the limit of sequence DJeε (f )δf is an element of the set ∂J(f )

4

Numerical approximation

Now we shall give similar convergence results for discretization of the identification problem, and we will remark that at the limit, both approximations

(artificial viscosity and discretisation) reach the same element of the subdifferential ∂J(f ) characterized by the reversible solution of the adjoint problem. We

shall prove these results for a large class of numerical schemes which contains

the schemes used to resolve the identification problem in [9].

First we discretize the cost function (denoted J∆ ) and the direct problem (1).

Next we compute a discrete Lagrangian, which will lead to a discrete adjoint

state, and finally to a discrete gradient of J∆ . This method of computing

the exact gradient of the discretized problem seems to have better properties

(concerning stability, for instance) than discretizing the exact adjoint state.

Moreover notice that we have no natural way to discretize it since the adjoint

equation is ill-posed.

4.1

Discretization and convergence for the direct problem

Let ∆z (resp. ∆t) be a positive space (resp. time) step. These parameters

will tend to 0, the ratio λ = ∆t/∆z remaining constant. For n = 0, . . . , N ,

j = 0, . . . , J, the sequence wjn is an approximation of solution w at the point

(zj = j∆z, tn = n∆t). In the same way, we discretize w0 (z), wobs (z), by wj0 ,

wjobs respectively. We consider a conservative (2K + 1)-points scheme for the

hyperbolic equation (1)

n

o

n

n

wjn+1 = wjn − λ gj+

(54)

1 (f ) − g

j− 1 (f ) ,

2

2

18

FLUX IDENTIFICATION IN CONSERVATION LAWS

n

n

n

gf being the numerical flux of the

where gj+

1 (f ) = gf (wj−K+1 , . . . , wj+K ),

2

scheme, consistent with f : gf (w, . . . , w) = f (w). Then the discretized identification problem becomes the following minimization problem

(55)

min J wf∆ ,

f

where wf∆ is the piecewise constant function defined by the sequence wjn (f ) ;

j = 0, . . . , J − 1, n = 0, . . . , N − 1 ∈ IRM , which was built out of (54).

To obtain the exact gradient of the discretized cost function, we follow exactly the same lines as in the formal computation and viscous regularization,

that is we build up a discrete Lagrangian L∆ using a “discrete weak form” of

the direct scheme (54), then we differentiate with respect to wjn , and we choose

the sequence pnj in order to cancel ∂L∆ /∂wjn for all j and n. This defines the

adjoint scheme. Finally, for the discrete gradient, the computations give:

X

n

(56)

pn+1

− pn+1

DJe∆ (f )δf = − ∆t

j

j+1 Dgj+ 1 (f )δf

2

n,j

where p∆ is solution of the adjoint scheme

K−1

X ∂

n+1

pn = pn+1 − λ

gn

− pn+1

1 (p

j

j

j+k+1 ),

∂wjn j+k+ 2 j+k

k=−K

∂J w∆

N

.

pj =

∂wjN

(57)

The complete computations are rather tedious, and we refer to [9] or [17] for

greater detail and for some examples as well.

First we show a convergence result of our discretized cost function, which

allow us to say that the continuous identification problem can be approximated

by the discretized identification problem. We consider a suitable set of functions

F , which we suppose bounded and closed for the Lipschitz continuous norm

k kLip . Next we suppose that the numerical flux g introduced in (54) is Lipschitz

continuous with respect to w−k , . . . , wk , and independent of f ∈ F , i.e. that

there exists a constant CLip independent of f , such that

|gf (w) − gf (v)|

≤ CLip ,

∀f ∈ F .

(58)

sup

|w − v|

w,v≥0

We also suppose that the scheme (54) satisfies

|wjn (f )| ≤ C∞ ,

for all j, n,

and for any f ∈ F ,

(59)

where C∞ is a constant independent of f . Condition (59) is verified for the

Lax-Friedrichs, Godunov [7], and Van-Leer [20] schemes, when the following

FLUX IDENTIFICATION IN CONSERVATION LAWS

19

CFL-condition is satisfied

λ

sup |f ′ (w)| < 1.

w≥0

f ∈F

(60)

This leads us to our convergence result:

Proposition 2 Let wf∆∆ built out of the conservative scheme (54) which we

suppose consistent with equation (1), and verifying hypotheses (58) and (59),

0

f∆ being the solution of (55). If the initial condition w∆

is bounded in L∞ (IR) ∩

∆

∞

BV (IR), then wf∆ is bounded in L (IR × (0, +∞)) and in L∞ (0, T, BV (IR)),

for all T > 0. Furthermore, if f∆k → f¯ ∈ F , for the Lipschitz continuous norm

k kLip , then

wf∆∆k

k

wf∆∆k

k

→ wf¯,

⇀ wf¯,

in L∞ (0, T, L1 (0, L)) − strong,

∞

in L (Ω) − weak∗,

(61)

(62)

Remarks. We can prove this proposition thanks to the continuity result

of Lucier [13], and by copying the proof of a convergence result for schemes

approximating scalar conservation laws in [6]. We omit the detail of this proof.

For instance, we consider the identification problem arising from the chromatographic model (see [9]), and we take a bounded subset of parameters

K ∈ IRN . Then we deduce the CFL-condition (60), and we have at least one

accumulation point of the sequence {f∆ }∆x,∆t.

We suppose that wobs and w0 have a compact support, so that for 0 < t < T ,

the support of the solution wf to equation (1), with f ∈ F , is in a compact set

Ω = (0, L) × (0, T ). Proposition 2 and a convergence result of [9] imply

Corollary 4 Let wf∆∆ be the solution of a conservative and TVD scheme (54),

consistent with equation (1). Then any accumulation point f¯ ∈ F of the sequence

{f∆ }∆x,∆t for the Lipschitz continuous norm, is solution of

J(wf ) = min J(wg ),

g∈F

where wf is the entropy solution of equation (1), with f ∈ F .

4.2

Monotone and TVD adjoint schemes

Here we study some properties of monotonicity and BV estimates for adjoint

schemes associated to the schemes in conservative form (54). We notice that

adjoint schemes cannot be put in conservative form, which is not surprising,

since the adjoint equation is not conservative. However, we shall prove that

a family of TVD difference schemes, including the Godunov and the Van-Leer

schemes, is associated to TVD adjoint schemes.

20

FLUX IDENTIFICATION IN CONSERVATION LAWS

First we define the function δx p∆ by

δx p∆ (x, t) =

p∆ (x, t) − p∆ (x + ∆x, t)

,

∆x

where δx p∆ is the piecewise constant function with value ∆pnj+ 1 /∆x in the

2

rectangle

1

1

Πnj = ((j − )∆x, (j + )∆x) × (n∆t, (n + 1)∆t).

2

2

On the other hand, we define the differences ∆pnj+ 1 = pnj − pnj+1 , for all j ∈ Z,

2

n ≤ N . Using the linearity of the scheme (57), we deduce the following scheme

for ∆pnj+ 1 :

2

K

X

∆pnj+ 1 =

2

,

Akj+k ∆pn+1

j+k+ 1

(63)

2

k=−K

where the coefficients Akj are defined by

n

∂

∂

Akj = − λ

gj+ 1 , for k 6∈ {−K, 0, K},

−

n

n

2

∂w

∂w

j−k

j−k+1

∂

∂

−K

n

AK

gn 1 ,

j = λ

Aj = − λ ∂wn gj+ 12 ,

n

∂wj−K+1 j+ 2

j+K

A0 = 1 − λ ∂ − ∂ g n .

j

∂w n

∂w n

j+ 1

j

j+1

(64)

2

Notice that by construction the coefficients Akj satisfy

K

X

Akj = 1,

∀j ∈ Z

(65)

k=−K

Now we wish the adjoint scheme to have the same property of monotonicity

preservation as the continuous equation. Thus, in view of (63), it is natural to

impose

Akj ≥ 0, for − K ≤ k ≤ K, j ∈ Z.

(66)

This is somehow the discrete analogous to the (OSLC) condition (34) used for

the convergence of the viscous perturbation.

Example. In the model of chromatography, the Godunov scheme is very

simple (it is just an upwind scheme). The adjoint scheme is given by (see [9])

pnj = pn+1

− λf ′ (wjn ) pn+1

− pn+1

(67)

j

j+1 .

j

In this case, the coefficients Akj are

′

n

A−1

j = λf (wj ),

A0j = 1 − λf ′ (wjn ),

A1j = 0.

FLUX IDENTIFICATION IN CONSERVATION LAWS

21

The CFL condition (60) implies that these coefficients are positive.

Similarly, the adjoint scheme associated to the Van-Leer difference scheme

verifies the hypothesis Akj ≥ 0 when we have CFL condition (60), and it is

a monotone and TVD scheme, whereas we can see that the adjoint scheme

associated to the Lax-Friedrichs difference scheme does not verify this hypothesis

of positivity and that it is an unstable scheme in BV (IR).

We have the following a priori estimates

Proposition 3 We consider a linear scheme in form (57), with its coefficients

defined by (64) and verifying the monotonicity property (66). Then we have for

all 0 < s, t < T the following estimates

T V (p∆ (., t)) ≤ T V (p∆ (., T )),

(68)

kp∆ (., t)kL1 (IR) ≤ kp∆ (., T )kL1 (IR) + CT T V (p∆ (., T )),

(69)

kδx p∆ (·, t)kL∞ (IR) ≤ kδx p∆ (·, T )kL∞ (IR) ,

(70)

kp∆ (., t) − p∆ (., s)kLp (ω) ≤ C

|t − s| + ∆t

|∆t|

p−1

p

kδx p∆ (·, T )kL∞ (IR) ,

(71)

where ω is a compact set in IR, 1 ≤ p ≤ +∞, and C > 0 is a constant independent of the discretization.

Remark. Estimates (68) and (69) are classical results of the theory of

approximation of non-linear conservation laws. They rely upon monotonicity

properties of the schemes, and are in particular independent of the conservative

form. The estimate (71) is a technical result allowing us to use a diagonalization

argument in order to pass to the limit, when ∆t, ∆z → 0.

Notice that the result of estimate (70) bears some resemblance to that of

the W 1,∞ estimate proved in theorem 4.

Proof of proposition 3. Let R ≥ K. Summing up (63) from j = −R

to j = R, and using the positivity of Akj and property (65), and passing to the

limit R → +∞, we obtain the estimate (68). On the other hand, using this BV

estimate, the L1 estimate (69) is obtained by an analysis that is similar to the

one made by Godlewski & Raviart ([6], chapter III) for the different schemes in

conservative form. Now, using the condition Akj+k ≥ 0, the estimate (70) results

from the monotonicity of

(H∆ (∆p))j =

K

X

k=−K

.

Akj+k ∆pn+1

j+k+ 1

2

In order to obtain the next estimate (71), we write the scheme (57) in the

form

K−1

X ∂

n+1

n+1

n

pj − pj

= −λ

gn

,

1 ∆p

j+k+ 12

∂wjn j+k+ 2

k=−K

22

FLUX IDENTIFICATION IN CONSERVATION LAWS

and by the Lipschitz condition of g, we have

|,

|pnj − pn+1

| ≤ λC sup |∆pn+1

j

j+ 1

2

j∈Z

with a constant C independent of the discretization. That implies

kp∆ (·, n∆t) − p∆ (·, (n + 1)∆t)kLp (ω) ≤ λ

p−1

p

1

1

|.

C|ω| p |∆t| p sup |∆pn+1

j+ 1

2

j∈Z

Let m > n. Applying successively this same result for n, n + 1, . . . , m − 1,

and using the triangular inequality of the norm k · kLp , we obtain

1

kp∆ (·, n∆t) − p∆ (·, m∆t)kLp (ω) ≤ C|∆t| p (n − m) sup |∆pN

j+ 1 |.

j∈Z

2

(72)

Let s, t such as n∆t ≤ s ≤ (n + 1)∆t, m∆t ≤ t ≤ (m + 1)∆t. We notice that

(m − n)∆t ≤ |t − s| + ∆t. Inequality (72) gives the desired result (71).

4.3

Convergence for adjoint schemes and derivatives

Now we shall evidence that the sequence of discrete gradients converges to the

same element of the subdifferential of the cost function given by the limit of

the viscous perturbation. First we have the following convergence result for the

solution of the adjoint scheme

Theorem 7 We consider the linear difference scheme in the form (57), where

the coefficients are defined in (64) and verify the monotonicity property (66).

We suppose pT ∈ W 1,∞ (IR) ∩ BV (IR), and the (OSLC) condition (34). Then,

p∆ → p

in L∞ (0, T, Lqloc (IR)) − strong,

1 ≤ q < +∞,

where p is the reversible solution of (13).

Proof. In accordance with the estimate (70) and in keeping with the

hypothesis pT ∈ W 1,∞ (IR), we have

sup |δx p∆ (x, t)| ≤ C.

(73)

x

Applying the theorem of Riesz-Fréchet-Kolmogorov (see Adams [1]) in the last

inequality, we deduce that we can take a subsequence ∆k x, ∆k t → 0 which we

still denote with ∆x, ∆t, such as

p∆ (·, t) → p(·, t)

in Lqloc (IR)) − strong,

∀t ∈ (0, T ),

for all 1 ≤ q < +∞. Using the estimate (71) and a classical diagonalization

argument (see [6]), we deduce the convergence in L∞ (0, T, Lqloc (IR)).

FLUX IDENTIFICATION IN CONSERVATION LAWS

23

In order to prove that the limit p is a Lipschitz continuous solution of (13),

we proceed by similar arguments to the proof of theorem 5. Next we notice that

the scheme in the form (57) preserves monotonicity as soon as Akj ≥ 0 (which

is satisfied for instance by the adjoints of Godunov and Van-Leer schemes).

Finally, we use the same arguments of the first remark following the proof of

theorem 5. That is,

q

p∆ → p in L∞ (0, T, Lloc (IR))

p∆ = p1∆ − p2∆ , with (pnj )i ≤ (pnj+1 )i , and pi∆ solution of the scheme (57)

implies that p is reversible.

It is easy to verify that Je∆ : f 7→ J(wf∆ ) have a continuous derivative if

n

n

the numerical flux g is of class C 1 with respect to (wj−K+1

, . . . , wj+K

). As a

consequence of theorem 7, we have

Corollary 5 Let Je∆ : f 7→ J(wf∆ ) be a discretized cost function defined for all

Lipschitz continuous function f , with wf∆ solution of the scheme in the conservation form (54). We suppose that the coefficients Akj in (64) satisfy Akj ≥ 0,

for −K ≤ k ≤ K, j ∈ Z, and that w0 has a compact support. Furthermore we

suppose that pT ∈ W 1,∞ (IR) ∩ BV (IR). Let wf be the entropy solution of (1),

and pf be the reversible solution of (13). Then we have

DJe∆ (f )δf →

Z

0

T

Z

+∞

∂x pf δf (wf )dxdt,

when ∆x, ∆t → 0,

(74)

−∞

for all Lipschitz direction δf .

Remark. We note that the theorem 6 and the corollary 5 make it clear that

a viscous perturbation or a numerical approximation of the gradient give the

same result at the limit.

We clarify this result by another corollary which reads as follows:

Corollary 6 Assume that Je is a minimum at f , and that Je and Je∆ are convex

for all (∆x, ∆t) in a neighborhood of f . Then, under the hypotheses of theorem

5, DJe∆ (f )δf converges to the same element of the subdifferential ∂J(f ) of J(f )

which we have obtained by a viscous perturbation in Corollary 3, when ∆x, ∆t →

0.

5

Numerical results

We illustrate in this section our results by a numerical application on real experimental data. We consider the propagation of a single, pure compound in a

column, which leads under several physical assumptions to a scalar conservation

law of the form (1). More precisely, the experimental data are concentration

FLUX IDENTIFICATION IN CONSERVATION LAWS

24

profiles obtained from the adsorption of gaseous n-hexane on graphite carbon

with helium vector gas. We refer to Rouchon et al. [16] for the complete description of the experiment, the discussion of the model and the original results.

A remarkable feature of this experiment is that we have an experimentally identified flux to compare with.

The observation here is a profile of concentration vs time, at a fixed L > 0,

where L is the length of the column. This is not quite the context of the previous analysis, but since in this kind of models the flux satisfies f ′ (w) > 0, a

slight modification is only needed. The direct problem is discretized through a

Godunov scheme, and we compute the exact gradient of the discrete functional

as indicated in section 4.1 (see also [9] for details). At this discrete level, all the

quantities are well-defined, so we are able to apply a gradient-based minimization algorithm. Thus we are left with the problem of non uniqueness for f which

was mentioned before. To handle this, we specify an analytic form for f , based

on physical arguments, which we do not detail here. We refer the interested

reader to [10] and the references therein fore more complete information. If c

denotes the concentration of the compound, then a family of fluxes depending

on a finite number of parameters is given by

f (c) = N

KcP ′ (Kc)

,

qP (Kc)

P (w) =

q

X

αi exp(−βEi )wi ,

(75)

i=0

where q ≥ 1 is an integer, αi and β are given constants involving temperature

and other fixed parameters of the experiment. The relevant parameters to

identify here are the so-called Langmuir coefficient K, N and Ei , 2 ≤ i ≤ q

(E0 = E1 = 0 by construction). The model obtained with q = 1 or equivalently

with Ei = 0 ∀i is the classical Langmuir model.

These parameters do not have the same influence on the concentration profiles. Roughly speaking, K and N act essentially on the position of the profile,

while Ei modify its shape. The minimization algorithm has therefore to be

carefully modified to handle this problem (see [9]). In the first application, we

chose as initial guess the Langmuir model, with a given value of K, and we fixed

the value of N = 2.19 10−2 .

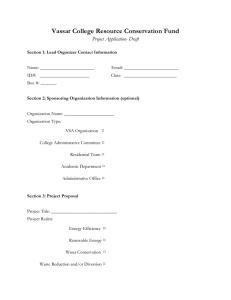

The coefficients of the initial guess and the identification result are given in

table 1, and the comparison between the experimental flux, the initial guess and

the identified flux is shown on figure 5. Finally, figure 5 shows the experimental

and identified concentration profiles.

These figures deserve a few remarks. The comparison between the profiles in

figure 5 proves that our identification is quite successful. Concerning the fluxes

themselves, we notice in figure 5 the good agreement with the experiment on

the whole domain of measurement, even though the domain of identification is

0 ≤ c ≤ 0.004 g./mol.

In order to illustrate the non uniqueness, we tried another identification.

Starting from an initial guess which has a convenient shape, we tried to identify

only the coefficients N and K, leaving the ratio K/N constant. The results are

shown in table 2. The resulting profile is identical to the one in figure 5.

25

FLUX IDENTIFICATION IN CONSERVATION LAWS

Parameters

K

E2

E3

E4

Initial Guess (Langmuir)

1596.

0.

0.

0.

Identification Result

1178.

-806.

-213.

-16.

Table 1: Initial and identified coefficients (1)

Langmuir (initial guess)

Identification

Experimental

0.004

concentration (g/mol)

0.003

0.002

0.001

0

0

50

100

150

time (seconds)

Figure 1: Comparison between experimental and identified profiles

26

FLUX IDENTIFICATION IN CONSERVATION LAWS

phase 2 (coverage rate)

1

0.5

Initial Guess

Identification

Experimental

0

0

0.05

0.1

0.15

0.2

0.25

phase 1 (g/mol)

Figure 2: Comparison between experimental and identified isotherm

FLUX IDENTIFICATION IN CONSERVATION LAWS

Parameters

N

K

E2

E3

E4

Initial Guess

2.19 10−2

1596.

214.

-1252.

1251.

27

Identification Result

1.42 10−2

2068.

214.

-1252.

1251.

Table 2: Initial and identified coefficients (2)

Figure 5 shows the preceding identification (labelled 1) and this one (labelled

2). We notice that indeed we obtain different functions, but however in the

domain of identification, they are virtually indistinguishable.

We would like to emphasize that the choice of a physically relevant model

for the flux is of great importance to obtain a good agreement with experiment.

But even in this case the problem of uniqueness is not solved, and the correct

choice of the flux has therefore to rely on physical arguments: the parameters

here have a precise meaning, which has not been explored in these experiments.

We refer to [11] for similar results on a binary mixture, or in terms of partial

differential equations, on a system of two equations.

28

FLUX IDENTIFICATION IN CONSERVATION LAWS

0.01

0.009

0.008

phase 2 (g/mol)

0.007

0.006

0.005

0.004

0.003

0.002

Langmuir

Identification 1

Identification 2

0.001

0

0

0.005

0.01

0.015

phase 1 (g/mol)

Figure 3: Comparison between two identified isotherms

FLUX IDENTIFICATION IN CONSERVATION LAWS

29

References

[1] R. Adams, Sobolev spaces, Pure and Applied Mathematics, 65, Acad.

Press, New York-London, 1975.

[2] F. Bouchut and F. James, Équations de transport unidimensionnelles à

coefficients discontinus, C.R. Acad. Sci. Paris, t. 320, Série I, p. 1097-1102,

1995.

[3] F. Bouchut and F. James, One-dimensional transport equations with

discontinuous coefficients, Nonlinear Analysis TMA, 32 (1998), no 7, 891933.

[4] G. Chavent, Identification of distributed parameter systems: about the

output least square method, its implementation, and identifiability Proceeding of the 5th. IFAC Symposium on Identification and System Parameter

Estimations, Pergamon Press, Vol 1 (1979), pp. 85-97.

[5] E.D. Conway, Generalized Solutions of Linear Differential Equations with

Discontinuous Coefficients and the Uniqueness Question for Multidimensional Quasilinear Conservation Laws, J. of Math. Anal. and Appl., 18

(1967), 238-251.

[6] E. Godlewski and P.A. Raviart, Hyperbolic systems of conservation

laws. Mathématiques et applications, no 3/4, Ellipses, Paris, 1991.

[7] S. K. Godunov, A finite difference method for the numerical computation

of discontinuous solutions of the equations of fluid dynamics, Math. Sb. 47

(1959), 271-290.

[8] D. Hoff, The Sharp Form of Oleinik’s Entropy Condition in Several Space

Variables, Trans. of the A.M.S. 276, 707-714 (1983).

[9] F. James and M. Sepúlveda, Parameter identification for a model of

chromatographic column, Inverse Problems 10 (1994) 1299-1314.

[10] F. James, M. Sepúlveda and P. Valentin, Statistical thermodynamic

models for multicomponent diphasic isothermal equilibria, Math. Models

and Methods in Applied Science, 7 (1997), n◦ 1, 1-29.

[11] F. James, M. Sepúlveda, F. Charton and G. Guiochon, Determination of binary competitive equilibrium isotherms from the individual chromatographic band profiles, Prépublication MAPMO, université d’Orléans,

octobre 1997.

[12] S.N. Kružkov, First order quasilinear equations in several independent

variables, Math. USSR Sb., 10 (1970), pp. 127-243.

[13] B. Lucier, A moving mesh numerical method for hyperbolic conservation

laws, Math. of Comp. 46 (1986), n◦ 173, pp. 59-69.

[14] O.A. Oleinik, Discontinuous Solutions of Nonlinear Differential Equations, Amer. Math. Soc. Transl. (2), 26 (1963), 95-172.

[15] R.T. Rockafellar, Convex Analysis, Princeton University Press, Princeton, New Jersey, 1970.

FLUX IDENTIFICATION IN CONSERVATION LAWS

30

[16] P. Rouchon, M. Schœnauer, P. Valentin and G. Guiochon, Numerical Simulation of Band Propagation in Nonlinear Chromatography in

Preparative-Scale Chromatography. Marcel Dekker, Inc., New York and

Basel (1989).

[17] M. Sepúlveda, Identification de paramètres pour un système hyperbolique.

Application à l’estimation des isothermes en chromatographie. Thèse de

l’Ecole Polytechnique, Palaiseau, France, 1992.

[18] J. Smoller, Shock Waves and Reaction-Diffusion Equations, SpringerVerlag, New York, 1983.

[19] E. Tadmor, Local error estimates for discontinuous solutions of nonlinear

hyperbolic equations, SIAM J. Numer. Anal. 28 (1991), n◦ 4, pp. 891-906.

[20] B. Van Leer, Towards the Ultimate Conservative Difference Scheme V. A

Second-order Sequel to Godunov’s Method Jour. Comp. Physics, 32 (1979),

pp. 101-136.