UNCTAD Multi-Year Expert Meeting on Commodities and Development 2013

advertisement

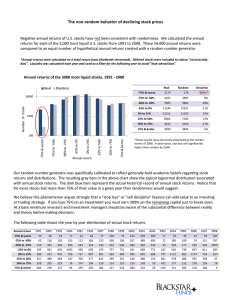

UNCTAD Multi-Year Expert Meeting on Commodities and Development 2013 Recent developments and new challenges in commodity markets, and policy options for commodity-based inclusive growth and sustainable development Room XXVI Palais des Nations Geneva, Switzerland Food commodity markets – trends and future challenges Boubaker Ben-Belhassen Trade and Markets Division, FAO 20 MARCH 2013 This material has been reproduced in the language and form as it was provided. The views expressed are those of the author and do not necessarily reflect the views of UNCTAD. Food commodity markets – trends and future challenges Boubaker Ben-Belhassen Trade and Markets Division, FAO UNCTAD, 20 March 2013 Outline • High vs. volatile prices –causes and effects • Medium-term market outlook • Key messages and future challenges • AMIS –what and what not 2 FAO Food Price Index, 2002-2004=100 Food prices –FAO Food Price Index more than doubled from 2002 to 2012 300 250 200 150 100 50 0 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 Food Price Index Cereals Meat Dairy 3 Why are food prices high and volatile? Why prices are high Market fundamentals – S&D • Strong growth in demand: emerging economies, population growth, changing diets, biofuels • Weak growth in production: slowdown in yield growth, high petroleum prices, natural resources constraints (land, water) • Low stocks Why prices are volatile • Production variability, due to weather and climate change • Increasing trade role by less resilient regions/countries • Low stock levels • Growing links with energy and financial markets • Policy impacts and panic • Macroeconomic factors (exchange rates, interest rates) 4 The importance of stocks, PQ space Price Without stocks Demand for consumption When stocks are low, prices become very sensitive to shocks in supply Different impact on prices Market demand, inclusive of storage With stocks Quantity Source: Brian Wright Equivalent shocks 5 Why food prices matter? • Food security • Agricultural development (uncertainty, suboptimal investment) • Economic growth and development • Macroeconomic stability (inflation, exchange reserves, government budgets) • Political and social stability 6 billion US$ Food imports bills –more than doubled for developing countries since 2005 500 450 400 350 300 250 200 150 100 50 0 $427 billion $235 billion $200 billion $75 billion Developing countries LIFDCs 7 A look at the current situation.. Cereal production, utilization and stocks Wheat production, utilization and stocks 8 A look at the current situation.. Coarse grain production, utilization and stocks Rice production, utilization and stocks 9 A look at the medium term.. • OECD-FAO Agricultural Outlook, 2012 edition • Integrated system of partial equilibrium models of the main food commodities • Combining model-generated projections and expert knowledge • Assumptions: population, macroeconomics, policy, and weather 10 World GDP growth assumptions – a multispeed world 11 World population –rapidly populating cities 12 Per capita consumption growth –flat to falling in developed countries, rising elsewhere 1.40 2000 = 1 1.35 1.30 N. America 1.25 W.Europe 1.20 N.Afr&ME 1.15 Asia 1.10 L. America 1.05 E.Europe&C.Asia 1.00 SSA 0.95 0.90 Index based on constant 2004-06 dollars 13 Shift in global consumption from staple foods to value-added products continues 14 Global ethanol and biodiesel production to almost double in the next decade 15 Agricultural production: growth to slow 1961-70 1971-80 1981-90 1991-00 2001-10 2011-20 All Agriculture Production 2.7 2.4 2.3 2.5 2.6 1.7 2.7 2.4 2.3 2.5 2.6 1.7 2.9 2.5 2.4 2.2 2.2 1.8 Crops Production Livestock Production 16 Agricultural production index Growth dominated by Latin America, slowest is W. Europe 2 Index, 2000 = 1 1.8 1.6 1.4 W. Europe L. America MENA SSA N. America 1.2 1 E. Eur & C. Asia Other Asia 0.8 0.6 17 Trade patterns: Latin America largest net exporter, Asia largest net importer Billions constant US, $2004-06 50 40 L.America 30 N.America 20 Other Asia 10 MENA 0 -10 SS Africa -20 E.Europe&C.Asia -30 W.Europe -40 Oceania -50 18 Real crop prices down from recent peaks, but to stay on a higher plateau 19 Key messages • Production growth slowing in developed countries, growing faster in developing countries • Consumption patterns changing rapidly • Food security remains first concern – Repeated price spike risks remain high – International policy coherence is increasingly important • Are we on track to feed the world? – Higher and more volatile prices indicate need for change – Investment in agriculture, higher productivity and sustainability are the viable policy response • Price incentives for investment in agriculture have increased • Emerging Issues: – Confidence in markets, market transparency, policy responses, supply-side constraints, sustainability 20 How can we eradicate hunger? • Link hunger eradication to poverty eradication • Achieve sustainable intensification of agriculture (FAO’s “Save and Grow” paradigm) • Reduce food losses and waste • Boost investment in agriculture • Put smallholders at the centre of action • Put in place effective food governance and trading systems (policies and institutions) • Build effective partnerships • Create markets that are transparent, efficient and inclusive 21 Thank you for your attention! UN Food and Agriculture Organization (FAO)