Simple Interest period of the investment.

advertisement

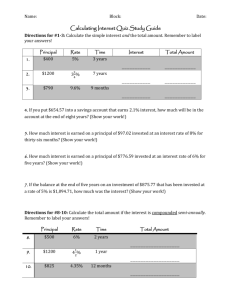

Simple Interest Interest is computed one time at the end of the whole time period of the investment. A(t)=P(1+rt) where r is the annual interest rate in decimal form. t is in years. Example: If $10,000 is invested at annual interest 4% for 6 months then the accumulated amount at the end of 6 months is A(t) = 10000(1+.04(.5)) = 10200. If the $10,000 is invested for 2 years, the accumulated amount at the end of 2 years is A(t) = 10000(1+.04(2))=10800. Compound Interest Interest is computed m times per year at regular intervals and added to the principal, so the interest earns interest for the rest of the time period. A ( t ) P (1 r ) mt m Continuous Compound Interest Interest is compounded continuously. A ( t ) Pe rt lim m P (1 r ) mt m In all formulas: P=the amount at the beginning of the time period, also called present value r=annual interest rate as a decimal t is in years m is the number of times interest is compounded per year In the tvm-solver: N=mt=the total number of compoundings I%=annual interest rate as a % PV=present value=amount at the beginning of the time period PMT=the amount of each regular payment at the end of each compounding period FV=the balance in the account at the end of N interest periods, also called future value C/Y=m P/Y=m Begin End End should be highlighted In the calculator, r is entered in % form. In all formulas, r is in decimal form. Effective Rate: The effective rate is the annual interest rate compounded yearly that is equal to the given interest rate compounded at the given times. It is the interest earned on $1 in 1 year. In the finance application in the calculator, it is EFF(r as a %, m) but do not type the %sign. The formula for effective rate is (1 r m ) 1, m where r is the decimal form of the interest and interest is compounded m times per year. 1. Find the effective rate of interest for each. Give each answer as a percent rounded to 4 decimal places. a) 6.5% compounded quarterly b) 6.5% compounded daily 2. Find the future value of a single investment of $1250.00 at interest rate 4 % compounded monthly for 5 years. 3. A car dealership offers a lease on an $18000 car. The lessee will pay $2000 down and $200 per month for 36 months. He then has the option to purchase the car for $13000. Instead, he could borrow from a bank the $16000 at 6.5% compounded monthly. Assuming his payments to the bank will also be $200 per month for 36 months, answer each of the following: (He will not be paying off the bank loan in 36 months, but will still owe money. Use N=36 for each.) a) Find the interest rate the car dealership is charging. b) What is the total amount paid to the car dealership in the lease agreement? How much of this is interest? c) How much is still owed on the bank loan at the end of 36 months? d) How much of the 37th payment to the bank would be interest? Mortgage 1. a) A family wants to buy a $200,000 home. They can make a $40,000 down payment. The bank charges 4.8% annual interest compounded monthly. If they pay off the loan by making equal monthly payments for 30 years, what will be their monthly payment? b) If the compounding and payments were quarterly, what would their quarterly payment be? Sinking Fund 2. The family now wants to set up a college fund for their newborn. They want the child to be able to withdraw $750/month for 4 years beginning 18 years from now. How much should they deposit each month for the next 18 years beginning now? Assume all the money still in the fund earns annual interest of 3.6% compounded monthly. i) Determine the amount they should have in the fund 18 years from now. ii) Determine what payments will accumulate this amount over the 18 years.

![Practice Quiz Compound Interest [with answers]](http://s3.studylib.net/store/data/008331665_1-e5f9ad7c540d78db3115f167e25be91a-300x300.png)