Inventories: Measurement

advertisement

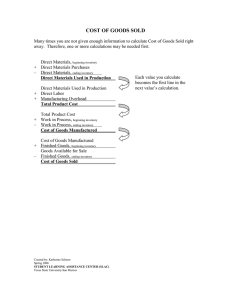

Inventories: Measurement RECORDING AND MEASURING INVENTORY TYPES OF INVENTORY There are two types of inventories depending on the kind of business operation. • Merchandise Inventory A merchandising concern buys and resells inventory in the ordinary course of business. Merchandise inventory is reported in the balance sheet as a current asset. • Manufacturing Inventory A manufacturing concern purchases raw materials (Raw Materials Inventory), combines it with labor and factory overhead (Work in Process Inventory) and then sells the finished product (Finished Goods Inventory) to its customers. At the end of each accounting period each category of inventory is reported as a current asset in the balance sheet. CONTROL There are two types of inventory systems that are used in maintain accounting records and report inventory in the financial statements. • Perpetual System Under the perpetual inventory system the entity maintains a continuous record of the balance in the Inventory account and the Cost of Goods Sold account through out the accounting period. a) Raw materials or merchandise purchases are charged to Raw Materials or Merchandise Inventory respectively as the purchases are made. b) Freight-in, purchase returns and allowances and purchase discounts are recorded in the inventory account. c) As each sales transaction is recorded the Inventory account is credited for the cost of the item and the Cost of Goods Sold account is debited. d) Inventory is a control account, which is supported by a detailed subsidiary ledger. • Periodic System Under the periodic inventory system the inventory account reflects the beginning balance of inventory. Throughout the accounting period purchases, freight-in, purchase returns and allowances and purchase discounts are recorded in separate expense accounts. At the end of the accounting period a physical inventory is taken and the inventory account is adjusted to reflect the correct ending inventory. Example of the year-end adjusting journal entries: Date Account Debit Beginning inventory End of year Income summary Credit Beginning inventory Inventory To remove beginning inventory from general ledger inventory account. F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 1 Inventories: Measurement Date Account Debit Ending inventory End of year Inventory Credit Ending inventory Income summary To record ending inventory in general ledger inventory account. Both the debit and credit are entered in the income summary account because we need both amounts in order to prepare a multi-step income statement. The debit and credit balances in the income summary account combined with the temporary expense accounts result in the computation of cost of goods sold as reported in the income statement at year-end. In the income summary account the debit reflects beginning inventory and the credit reflects ending inventory. PHYSICAL QUANTITIES INCLUDED IN INVENTORY • Goods in Transit The “passage of title” is the key to determining whether goods in transit are part of ending inventory. ¾ f.o.b. destination The title to the goods transfers when received by the buyer. Therefore, goods in transit year-end should be reported in the ending inventory of the seller. ¾ f.o.b. shipping point The title to the goods transfers when the seller delivers the goods to a common carrier. Goods in transit at year-end shipped f.o.b. shipping point should be included in the ending inventory of the buyer. • Consigned Goods The consignor is the seller of the merchandise who ships the goods on consignment to the consignee. The consignee is just an agent in the selling process and does not actually own the goods. Therefore, at year-end the consignor (seller) should include the consigned goods in its inventory even though it may still be in the physical possession of the consignee. • Sales Returns and Allowances When returns and allowances are material the company must estimate an allowance to the amounts reflected in the balance sheet and income statement at year end. In preparing the adjusting journal entry for this allowance the amount of anticipated inventory that will be returned after year end is included in the ending inventory in the balance sheet. EXPENDITURES INCLUDED IN INVENTORY Product Costs Product costs are all of the costs required to obtain inventory and are included in the ending inventory and/or the cost of goods sold. They include • Direct cost of the product • Freight-in • Other direct costs of acquisition F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 2 Inventories: Measurement • Labor and factory overhead applied to raw material to produce finished goods Period Costs Period costs are those costs that are allocated to the accounting period and are not included in inventory. They include • Selling expenses • General and administrative expenses • Interest expense Manufacturing Costs Manufacturing costs include all of the costs directly involved in the production of a product that becomes finished goods. They include • Direct materials • Direct labor • Manufacturing overhead costs ¾ Indirect material ¾ Indirect labor ¾ Depreciation ¾ Taxes ¾ Insurance ¾ Heat ¾ Electricity Freight-In As indicated above freight-in on merchandise purchases are added to the cost of the merchandise inventory. Under the perpetual method the amount is added to inventory along with the cost of the merchandise. Using the periodic method a company would set up a nominal account, “Freight-In” and would book all freight-in charges to this account. At the end of the year this account becomes part of the multi-step income statement analysis that determines cost of goods available for sale, ending inventory, and cost of goods sold. Purchase Returns and Allowances Purchase returns and allowances are the counter part to sales returns and allowances. Under the perpetual method the purchasing company removes the amount returned from inventory and accounts payable. Using the periodic method a company would set up a nominal account, “Purchase Returns and Allowances” and would book all returns to this account. At the end of the year this account becomes part of the multi-step income statement analysis that determines cost of goods available for sale, ending inventory, and cost of goods sold. Purchase Discounts There are two methods of recording purchase discounts (1) Gross Method Under the gross method a purchase discounts account is used. The purchase and related account payable is recorded at the full invoice amount. If the purchaser makes payment by the discount date, the credit for the discount is recorded in the “purchase discounts” account. F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 3 Inventories: Measurement Example: On September 15, 2001, Spencer Company purchases $100,000 of merchandise with terms of 2/10, n/30. The company pays the invoice on September 23, 2001 (within the discount) and takes the 2% discount. Using the gross method Spencer Company would record the purchase and payment as follows: Date 9/15/01 Date 9/23/01 Account Debit $100,000 Inventory Accounts payable To record purchase of merchandise inventory, terms 2/10, n/30 Account Debit $100,000 Credit $100,000 Credit Accounts payable Purchase discounts $2,000 98,000 Cash To record the payment net of the 2% cash discount on merchandise (2) Net Method Under the net method a “purchase discounts lost” account is used. The purchase and related account payable are recorded at net of the discount. It is assumed that the purchaser will always take advantage of the cash discount. If the purchaser fails to make payment by the discount date the debit is charged to a “purchase discounts lost” account. Special Sale Agreements There are special circumstances where the legal title to the goods might have changed hands but there is a high degree of uncertainty as to whether the sale has been completed. • Sales with Buyback Agreement ¾ Product Financing Agreement The buyer takes title to the merchandise but has the option to return the merchandise for a full refund including holding costs. Under these circumstances the seller should report the inventory and related liability on its books. ¾ Parking Transaction There are certain industries where it is common for the seller to ship merchandise to the buyer. The buyer holds the merchandise for a short period of time (through year-end) and then returns the merchandise. This is sometimes called window dressing with respect to the preparation of year-end financial statements. No matter what it is called, based on historical facts or agreements between the parties, the seller should continue to report the inventory on its year-end financial statements. • Sales with High Rates of Return In some industries the buyer is allowed to return unsold merchandise for a partial or full refund. If the returns can be estimated then a provision (an allowance account) should be made and the goods should be treated as sold to the buyer. If it is not possible to determine F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 4 Inventories: Measurement the estimated amount of returned goods, the seller should continue to report the inventory on its books. COST FLOW ASSUMPTIONS The physical flow of movement of goods and the cost flow assumptions used to maintain accounting records are not always the same. Specific Identification This is the only cost flow assumption where the physical flow and the cost flows are identical. Under this method each item of inventory is accounted for separately and the actual cost of that item is recorded in the cost of goods sold account when the item is sold. This is only practical for high-ticket items and relatively low sales volume in terms of the number of units. Average Cost Under this method ending inventory and cost of goods sold are priced based on the average cost of the goods available for sale during the accounting period. • Periodic inventory system If the entity is using a periodic inventory system the calculation is based on the weightedaverage of the number of units and their respective costs at the end of the accounting period. This is called the weighted-average method. Example: The following inventory transactions took place in September 2000. Spencer Company Inventory Transactions For the Month of September 2000 Periodic Inventory System, Weighted Average Date 9/1/00 9/10/00 9/25/00 Transaction Beginning inventory Purchase of merchandise Purchase of merchandise Units 2,000 500 1,000 Price $10.00 11.00 12.50 Total $20,000 5,500 12,500 The company sold 2,800 units of merchandise inventory during the month. The following provides an analysis of the cost of goods sold and the ending inventory using the weightaverage method of assigning costs. F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 5 Inventories: Measurement Spencer Company Inventory Transactions For the Month of September 2000 Periodic Inventory System, Weighted Average Date 9/1/00 9/10/00 9/25/00 9/30/00 9/30/00 • Transaction Beginning inventory Purchase of merchandise Purchase of merchandise Goods available for sale Cost of goods sold: Merchandise sold in September Ending Inventory: Merchandise on hand Analysis of weighted average: Goods available for sale: Total cost Total units Weighted average Units 2,000 500 1,000 3,500 Price $10.00 11.00 12.50 $10.86 Total $20,000 5,500 12,500 $38,000 2,800 $10.86 $30,400 700 $10.86 $7,600 $38,000 3,500 $10.86 Perpetual inventory system If the entity is using the perpetual inventory system the calculation is based on the movingaverage of the number of units and their respective costs after each purchase. This is called the moving-average method. Example: Using the same information as above but assuming that Spencer Company uses the perpetual inventory system the calculation of cost of goods sold and ending inventory is much different. Each time the company purchases merchandise the new moving weighted average has to be recalculated. This average cost is then used to calculate the cost of goods sold on any subsequent sales transactions. F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 6 Inventories: Measurement Pepetual Inventory System, Moving Average Cost of goods available Cost of goods sold Date Transaction Units Price Total Units Price Total Beginning 9/1/00 9/10/00 Purchase 500 $11.00 $5,500 9/15/00 Sold 9/25/00 Purchase 9/30/00 Sold 9/30/00 Ending Ending inventory Units Price Total 2,000 $10.00 $20,000 2,000 $20,000 500 5,500 2,500 $10.20 $25,500 800 $10.20 $8,160 2,500 $25,500 (800) ($8,160) 1,700 $10.20 $17,340 1,000 $12.50 $12,500 1,700 17,340 1,000 12,500 2,700 $11.05 $29,840 2,000 $11.05 $22,104 2,700 29,840 (2,000) (22,104) 1,500 $18,000 2,800 $30,264 700 $11.05 $7,736 First-In, First-Out (FIFO) Under FIFO it is assumed that the cost of goods sold are recorded based on the order that the merchandise was purchased. The best way to think about FIFO is to think about the sale of milk. The grocery store puts the oldest milk in front so that it will be sold first. The milk that was purchased most recently will be part of ending inventory whereas the older milk will be part of the cost of goods sold. Using the FIFO cost flow assumption the cost of goods sold and ending inventory are identical under the perpetual and periodic inventory systems. Ending inventory is based on the most recently purchased merchandise. Cost of goods sold is based on the oldest inventory and ending inventory is based on the merchandise purchased most recently. In many cases the FIFO method approximates the physical flow of goods. The balance sheet reflects an ending inventory that is valued at current costs. The major disadvantage to the FIFO assumption is that in inflationary times the cost of goods sold can be materially distorted. If the costs in beginning inventory are substantially lower than current costs, gross profit is overstated by the amount of inflation that took place during the accounting period. Example: Assuming the same facts as above the cost of goods sold and ending inventory using the FIFO cost flow assumption is as follows: F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 7 Inventories: Measurement Spencer Company Inventory Transactions For the Month of September 2000 FIFO Cost Flow Assumption Date Transaction 9/1/00 Beginning inventory 9/10/00 Purchase of merchandise 9/25/00 Purchase of merchandise 9/30/00 Goods available for sale Cost of goods sold: 9/1/00 Beginning inventory 9/10/00 Purchase of merchandise 9/25/00 Purchase of merchandise Cost of goods sold Ending Inventory: 9/25/00 Purchase of merchandise Units 2,000 500 1,000 3,500 Price $10.00 11.00 12.50 Total $20,000 5,500 12,500 $38,000 2,000 500 300 2,800 $10.00 $11.00 $12.50 $20,000 5,500 3,750 $29,250 700 $12.50 $8,750 Last-In, First-Out (LIFO) Under LIFO it is assumed that the cost of goods sold reflect the most recently purchased merchandise. The ending inventory in the balance sheet contains costs that reflect beginning inventory and possibly merchandise purchased early in the accounting period. The inventory method has an impact on the calculation of ending inventory and cost of goods sold. • Periodic inventory system If the entity is using a periodic inventory system cost of goods sold is calculated based on the most recently purchased merchandise. Example: Assuming the same facts as above the cost of goods sold and ending inventory using the Periodic Inventory and applying the LIFO cost flow assumption is as follows: F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 8 Inventories: Measurement Spencer Company Inventory Transactions For the Month of September 2000 Periodic Inventory System - LIFO Cost Flow Assumption Date Transaction 9/1/00 Beginning inventory 9/10/00 Purchase of merchandise 9/25/00 Purchase of merchandise 9/30/00 Goods available for sale Cost of goods sold: 9/25/00 Purchase of merchandise 9/10/00 Purchase of merchandise 9/1/00 Beginning inventory Cost of goods sold Ending Inventory: 9/1/00 Beginning inventory • Units 2,000 500 1,000 3,500 Price $10.00 11.00 12.50 Total $20,000 5,500 12,500 $38,000 1,000 500 1,300 2,800 $12.50 $11.00 $10.00 $12,500 5,500 13,000 $31,000 700 $10.00 $7,000 Perpetual inventory system If the entity is using the perpetual inventory system cost of goods sold is calculated at point of each sale based on the most recently purchased merchandise at that date. Example: Assuming the same facts as above the cost of goods sold and ending inventory using the Perpetual Inventory and applying the LIFO cost flow assumption is as follows: F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 3/12/2007 9 Inventories: Measurement Pepetual Inventory System, LIFO Cost Flow Assumption Cost of goods available Cost of goods sold Date Transaction Units Price Total Units Price Total Beginning 9/1/00 9/10/00 Purchase 500 $11.00 $5,500 9/15/00 Sold 9/25/00 Purchase 500 $11.00 300 10.00 800 1,000 $12.50 $12,500 9/30/00 Sold 9/30/00 Ending $5,500 3,000 $8,500 1,500 F:\Teaching\3321\web\module4\c8\tnotes\c8a.doc 1,000 $12.50 $12,500 1,000 10.00 10,000 2,000 $22,500 $18,000 5,600 $62,000 3/12/2007 Ending inventory Units Price Total 2,000 $10.00 $20,000 2,000 $10.00 $20,000 500 $11.00 5,500 2,500 $25,500 2,500 $25,500 1,700 $10.00 $17,000 1,700 $10.00 $17,000 1,000 $12.50 12,500 2,700 $29,500 700 $10.00 $7,000 10