Evolution of Macro

advertisement

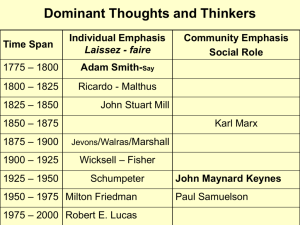

Adam Smith: The division of labor is limited by the extent of the market Division of labor Increasing Returns to Scale ...by directing [his] industry in such a manner as its produce may be of the greatest value, he intends only his own gain, and he is in this … led by an invisible hand to promote an end which was no part of his intention. Laissez -faire Jean Baptiste Say: Supply creates its own demand Thomas Robert Malthus: Theory of gluts Knut Wicksell: “Natural rate” …cumulative causation Irving Fisher: Debt deflation depression Keynes and the Great Depression The history of modern macroeconomics starts in 1936, with the publication of Keynes’s General Theory of Employment, Interest, and Money. Keynes The Great Depression was an intellectual failure for the economists working on business cycle theory— as macroeconomics was then called. Keynes emphasized effective demand, now called aggregate demand. Keynes and the Great Depression In the process of deriving effective demand, Keynes introduced many of the building blocks of modern macroeconomics: The relation of consumption to income, and the multiplier. Liquidity preference (the term given to the demand for money). The importance of expectations in affecting consumption and investment; and the idea that animal spirits are a major factor behind shifts in demand and output. The Neoclassical Synthesis Paul Samuelson wrote the first modern economics textbook: Economics Samuelson The neoclassical synthesis refers to a large consensus that emerged in the early 1950s, based on the ideas of Keynes and earlier economists. The neoclassical synthesis was to remain the dominant view for another 20 years. The period from the early 1940s to the early 1970s was called the golden age of macroeconomics. The Neoclassical Synthesis Progress on All Fronts The IS–LM Model The most influential formalization of Keynes’s ideas was the IS-LM model, developed by John Hicks and Alvin Hansen in the 1930s and early 1940s. Discussions became organized around the slopes of the IS and LM curves. The Neoclassical Synthesis Progress on All Fronts Theories of Consumption, Investment, and Money Demand In the 1950s, Franco Modigliani and Milton Friedman independently developed the theory of consumption, and insisted on the importance of expectations. Modigliani James Tobin developed the theory of investment based on the relation between the present value of profits and investment. Dale Jorgenson further developed and tested the theory. Tobin 7 of 34 The Neoclassical Synthesis Growth Theory In 1956, Robert Solow developed the growth model—a framework to think about the determinants of growth. It was followed by an explosion of work on the roles saving and technological progress play in determining growth. Solow Macroeconometric Models Lawrence Klein developed the first U.S. macroeconomic model in the early 1950s. The model was an extended IS relation, with 16 equations. Klein Keynesians versus Monetarists Milton Friedman was the intellectual leader of the monetarists, and the father of the theory of consumption. He believed that the understanding of the economy remained very limited, and questioned the motives and ability of governments to improve macroeconomic Friedman outcomes. In the 1960s, debates between Keynesians and monetarists dominated the economic headlines. The debates centered around three issues: (1) the effectiveness of monetary policy versus fiscal policy, (2) the Phillips curve, and (3) the role of policy. Friedman challenged the view that fiscal policy could affect output faster and more reliably than monetary policy. In a 1963 book, A Monetary History of the United States, 1867-1960, Friedman and Anna Schwartz reviewed the history of monetary policy and concluded that monetary policy was not only very powerful, but that movements in money also explained most of the fluctuations in output. They interpreted the Great Depression as the result of major mistake in monetary policy. Keynesians versus Monetarists The Phillips Curve Phelps The Phillips curve had become part of the Neoclassical synthesis, but Milton Friedman and Edmund Phelps argued that the apparent trade-off between unemployment and inflation would quickly vanish if policy makers actually tried to exploit it. By the mid 1970s, the consensus was that there was no long-run trade off between inflation and unemployment. The Role of Policy Skeptical that economists knew enough to stabilize output, and that policy makers could be trusted to do the right thing, Milton Friedman argued for the use of simple rules, such as steady money growth. Friedman believed that political pressures to “do something” in the face of relatively mild problems may do more harm than good. The Rational Expectations Critique In the early 1970s, Robert Lucas, Thomas Sargent, and Robert Barro led a strong attack against mainstream macroeconomics. Lucas Sargent Barro They argued that the predictions of Keynesian macroeconomics were wildly incorrect, and based on a doctrine that was fundamentally flawed. The Three Implications of Rational Expectations Lucas and Sargent’s main argument was that Keynesian economics had ignored the full implications of the effect of expectations on behavior. The Lucas Critique Robert Lucas argued that Keynesian macroeconomic models did not incorporate expectations explicitly so the models captured relations as they had held in the past, under past policies. They were poor guides to what would happen under new policies…regime change Rational Expectations and the Phillips Curve In Keynesian models, the slow return of output to the natural level of output came from the slow adjustment of prices and wages through the Phillips curve mechanism. Within the logic of the Keynesian models, Lucas therefore argued, only unanticipated changes in money should affect output. Optimal Control versus Game Theory The theory of policy had to be redesigned, using the tools of game theory. The Rational Expectations Critique The Integration of Rational Expectations The Implications of Rational Expectations Robert Hall showed that if consumers are very foresighted, then changes in consumption should be unpredictable. Hall Consumption will change only when consumers learn something new about the future. Since news about the future cannot be predicted, changes in consumption are highly random. This consumption behavior, known as the random walk of consumption, has served as a benchmark in consumption research ever since. The Integration of Rational Expectations The Implications of Rational Expectations Rudiger Dornbusch developed a model of exchange rates that shows how large swings in exchange rates are not the result of irrational speculation but, instead, fully consistent with rationality. Dornbusch Dornbusch’s model, known as the overshooting model of exchange rates, has become the benchmark in discussions of exchange-rate movements. The Rational Expectations Critique The Integration of Rational Expectations Wage and Price Setting Stanley Fischer and John Taylor showed that the adjustment of prices and wages in response to changes in unemployment can be slow even under rational expectations. Fischer Taylor They pointed to the staggering of both wage and price decisions, and explained how a slow return of output to the natural level can be consistent with rational expectations in the labor market. New Classical Economics and Real Business Cycle Theory Edward Prescott is the intellectual leader of the new classicals—a group of economists interested in explaining fluctuations as the effects of shocks in competitive markets with fully flexible prices and wages. Prescott Their real business cycle (RBC) models assume that output is always at its natural level, and fluctuations are movements of the natural level of output. These movements are fundamentally caused by technological progress. New Keynesian Economics The new Keynesians are a loosely connected group of researchers working on the implications of several imperfections in different markets. One line of research focuses on the determination of wages in the labor market. George Akerlof has explored the role of “norms,” or rules that develop in any organization to assess what is fair or unfair. Akerlof New Keynesian Economics Another line of new Keynesian research has explored imperfections in credit markets. Ben Bernanke has studied the relation between banks and borrowers and its effects on monetary policy. Ben Bernanke Yet another direction of research is nominal rigidities in wages and prices. The menu cost explanation of output fluctuations, developed by Akerlof and N. Gregory Mankiw, attributes even small costs of changing prices to the infrequent and staggered price adjustment. N. Gregory Mankiw New Growth Theory Robert Lucas and Paul Romer have provided a new set of contributions under the name of new growth theory, which take on some of the issues initially raised by growth theorists of the 1960s. Paul Romer New growth theory focuses on the determinants of technological progress in the long run, and the role of increasing returns to scale. Recent Developments New Growth Theory Andrei Shleifer (from Harvard University) has explored the role of different legal systems in affecting the organization of the economy, from financial markets to labor markets, and, through these channels, the effects of legal systems on growth. Andrei Shleifer Daron Acemoglu (from MIT) has explored how to go from correlations between institutions and growth— democratic countries are on average richer—to causality from institutions to growth Darin Acemoglu Recent Developments Dynamic Stochastic General Equilibrium Woodford, Gali, and a number of co-authors have developed a model, known as the New-Keynesian model, that embodies utility and profit maximization, rational expectations, and nominal rigidities. Michael Woodford Interest and Prices Inflation targeting Jordi Gali This model has proven extremely useful and influential in the redesign of monetary policy. It has also led to the development of a class of larger models that build on its simple structure, but allow for a longer menu of imperfections and thus must be solved numerically. These models, which are now used in most central banks, are known as dynamic stochastic general equilibrium (DSGE) models. Common Beliefs Most macroeconomists agree that: In the short run, shifts in aggregate demand affect output. In the medium run, output returns to the natural level. In the long run, capital accumulation and the rate of technological progress are the main factors that determine the evolution of the level of output. Monetary policy affects output in the short run, but not in the medium run or the long run. Fiscal policy has short-run, medium-run, and long-run effects on output. Some of the disagreements involve: The length of the “short run,” the period of time over which aggregate demand affects output. The role of policy. Those who believe that output returns quickly to the natural level advocate the use of tight rules on both fiscal and monetary policy. Those who believe that the adjustment is slow prefer more flexible stabilization policies.