Chapter 4 PowerPoint

advertisement

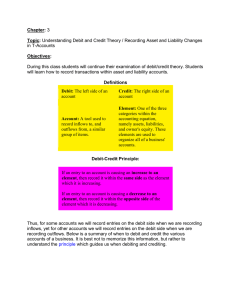

CHAPTER 4: Journalizing Transaction in a General Journal OBJECTIVES: Define accounting terms related to journalizing transactions. Identify accounting concepts and practices related to journalizing transactions. Record in a general journal transactions to set up a business. Record in a general journal transactions to buy insurance for cash and supplies on account. Record in a general journal transactions that affect owner’s equity and receiving cash on account. Start a new journal page. JOURNAL: Form used for recording transactions in chronological order. Provides a history of the business. Different types of journals - one we are using today is called a GENERAL JOURNAL. The process of recording transactions in a journal is called JOURNALIZING. Journal Entry Four parts: 1.Date 2.DR 3.CR 4.Source document – a business form that proves the transaction occurred Ch 4-1: Journals, Source Documents, and Recording Entries in a Journal GENERAL JOURNAL: A journal with two amount columns in which all kinds of entries can be recorded. *Entries are made in pen, and recorded in the order they occurred A GENERAL JOURNAL WHY use a journal??? •Accuracy DR=CR •Chronological Order •Store all info for transactions in one place •Columns (better than separate T-accounts) Lesson 4-1, page 66 Double-Entry Accounting – Every entry has two parts a debit and a credit. – Assures that debits equal credits. Source Document: Where the transaction came from – Describes each transaction. – Proof each transaction occurred. – Examples: • Check stub - C • Receipt - R • Calculator tape – T • Memorandum – M • Sales invoice - S Objective Evidence: (meaning, non-biased evidence) A source document is prepared for every entry. CHECKS - C ** USED FOR ALL CASH PAYMENTS ** Pre-numbered to account for all checks ** Prepare check stub at same time as check (Ch. 6) Lesson 4-1, page 67 SALES INVOICES - S ** Prepared when services are sold ON ACCOUNT ** AKA Sales ticket or sales slip ** Shows price, quantity, date, description ** Prepared in duplicate (2-part form) (Original –Customer; Duplicate – source document) Lesson 4-1, page 67 OTHER SOURCE DOCUMENTS – R, M, T Receipt (R) – business form giving written acknowledgement for cash received – Source doc for cash received from transactions other than sales • Ie: Cash from investment Memorandum (M) – form on which a brief message is written describing a transaction – Used when no other source doc is prepared or when an additional explanation is needed • Ie: buy supplies on account Calculator Tape (T) – total amount of all cash received from sales during a specific time period (day, week) – Single source doc for total sales – Figure comes from a printing electronic calculator – Numbered according to date cash is totaled OTHER SOURCE DOCUMENTS – R, M, T Lesson 4-1, page 68 Source Documents (Objective Evidence) Check KNOW THIS! – Paying cash Sales Invoice – Selling on account Receipts – When receiving cash for anything BUT sales Memorandum – Buying on account Calculator Tape – Summary of cash received RECEIVED CASH FROM OWNER AS AN INVESTMENT August 1. Received cash from owner as an investment, $10,000.00. Receipt No. 1. Lesson 4-1, page 69 RECEIVED CASH FROM OWNER AS AN INVESTMENT August 1. Received cash from owner as an investment, $10,000.00. Receipt No. 1. Cash 1. Which accounts are affected? Cash Barbara Treviño, Capital 2. How is each account classified? Cash is an asset account. Barbara Treviño, Capital is an owner’s equity account. Debit Normal Balance 10,000.00 Barbara Treviño, Capital 3. How is each classification changed? Assets are increased. Owner’s equity is increased. 4. How is each amount entered in the accounts? Assets increase on the debit side. Owner’s equity accounts increase on the credit side. Credit Normal Balance 10,000.00 Lesson 4-1, page 69 RECEIVED CASH FROM OWNER AS AN INVESTMENT August 1. Received cash from owner as an investment, $10,000.00. Receipt No. 1. 2 3 1 4 1. Write the date. 2. Debit Cash. 3. Credit Barbara Treviño, Capital. 4. Write the source document number. Lesson 4-1, page 69 PAID CASH FOR SUPPLIES Aug. 3. Paid cash for supplies, $1577.00. Check No. 1 1 4 2 3 Lesson 4-1, page 70 TERMS REVIEW journal journalizing entry general journal double-entry accounting source document check invoice sales invoice receipt memorandum TO DO: Audit your Understanding, pg 71 Work Together, pg 71 Lesson 4-1, page 71 On your own, pg 71 Chapter 4-2: Journalizing Buying Insurance, Buying on Account, and Paying on Account REVIEW SOURCE DOCS C R M T S PAID CASH FOR INSURANCE August 4. Paid cash for insurance, $1,200.00. Check No. 2. Prepaid Insurance 2. How is each account classified? Prepaid Insurance is as asset account. Cash is as asset account. 3. How is each classification changed? Assets are increased. Assets are decreased. Debit Normal Balance 1,200.00 Cash Debit Normal Balance 1,200.00 1. Which accounts are affected? Prepaid Insurance Cash 4. How is each amount entered in the accounts? Assets increase on the debit side. Journal – page 72 Assets decrease on the credit side. Lesson 4-2, page 72 BOUGHT SUPPLIES ON ACCOUNT August 7. Bought supplies on account from Ling Music Supplies, $2,720.00. Memorandum No.1. 4 2 1 3 1. Write the date. 2. Debit Supplies. 3. Credit Accounts Payable—Ling Music Supplies. 4. Write the source document number. Lesson 4-2, page 73 PAID CASH ON ACCOUNT August 11. Paid cash on account to Ling Music Supplies, $1,360.00, Check No. 3. Accts. Pay.—Ling Music Supplies Cash Debit Normal Balance 1,360.00 2. How is each account classified? Accts. Pay.—Ling Music Supplies is a liability account. Cash is an asset account. 3. How is each classification changed? Liabilities are decreased. Assets are decreased. Credit Normal Balance 1,360.00 1. Which accounts are affected? Accounts Payable—Ling Music Supplies Cash 4. How is each amount entered in the accounts? Liabilities decrease on the debit side. Assets decrease on the credit side. Lesson 4-2, page 74 PAID CASH ON ACCOUNT August 11. Paid cash on account to Ling Music Supplies, $1,360.00, Check No. 3. 4 1 2 3 1. Write the date. 2. Debit Accounts Payable—Ling Music Supplies. 3. Credit Cash. 4. Write the source document number. Lesson 4-2, page 74 TO DO: Work Together, pg 75 On your own, pg 75 CHAPTER 4-3: Journalizing Transactions That Affects Owner’s Equity and Receiving Cash on Account REVIEW SOURCE DOCS C R M T S RECEIVED CASH FROM SALES August 12. Received cash from sales, $325.00. Tape No. 12. Cash 1. Which accounts are affected? Cash Sales 2. How is each account classified? Cash is as asset account. Sales is as revenue account. 3. How is each classification changed? Assets are increased. Revenues are increased. 4. How is each amount entered in the accounts? Assets increase on the debit side. Revenues increase on the credit side. Debit Normal Balance 325.00 Sales Credit Normal Balance 325.00 Lesson 4-3, page 76 RECEIVED CASH FROM SALES August 12. Received cash from sales, $325.00. Tape No. 12. 4 1 2 3 1. Write the date. 2. Debit Cash. 3. Credit Sales. 4. Write the source document number. Lesson 4-3, page 76 SOLD SERVICES ON ACCOUNT August 12. Sold services on account to Kids Time, $200.00. Sales Invoice No. 1. Accounts Rec.—Kids Time 1. Which accounts are affected? Accounts Receivable—Kids Time Sales Debit Normal Balance 200.00 2. How is each account classified? Accounts Receivable—Kids Time is an asset account. Sales is as revenue account. 3. How is each classification changed? Assets are increased. Revenues are increased. 4. How is each amount entered in the accounts? Assets increase on the debit side. Revenues increase on the credit side. Sales Credit Normal Balance 200.00 Lesson 4-3, page 77 SOLD SERVICES ON ACCOUNT August 12. Sold services on account to Kids Time, $200.00. Sales Invoice No. 1. 1 4 2 3 1. Write the date. 2. Debit Accounts Receivable—Kids Time. 3. Credit Sales. 4. Write the source document number. Lesson 4-3, page 77 PAID CASH FOR AN EXPENSE August 12. Paid cash for rent, $250.00. Check No. 4. Rent Expense 2. How is each account classified? Rent Expense is an expense account. Cash is an asset account. 3. How is each classification changed? Expenses are increased. Assets are decreased. Debit Normal Balance 250.00 Cash Debit Normal Balance 250.00 1. Which accounts are affected? Rent Expense Cash 4. How is each amount entered in the accounts? Expenses increase on the debit side. Assets decrease on the credit side. Lesson 4-3, page 78 PAID CASH FOR AN EXPENSE August 12. Paid cash for rent, $250.00. Check No. 4. 1 1. Write the date. 2. Debit Rent Expense. 3. Credit Cash. 4. Write the source document number. 4 2 3 Lesson 4-3, page 78 RECEIVED CASH ON ACCOUNT August 12. Received cash on account from Kids Time, $100.00. Receipt No. 2. Cash 1. Which accounts are affected? Cash Accounts Receivable—Kids Time Debit Normal Balance 100.00 2. How is each account classified? Cash is an asset account. Accounts Rec.—Kids Time is an asset account. Accounts Rec.—Kids Time 4. How is each amount entered in the accounts? Assets increase on the debit side. Assets decrease on the credit side. Debit Normal Balance 100.00 3. How is each classification changed? Assets are increased. Assets are decreased. Lesson 4-3, page 79 RECEIVED CASH ON ACCOUNT August 12. Received cash on account from Kids Time, $100.00. Receipt No. 2. 1 4 2 3 1. Write the date. 2. Debit Cash. 3. Credit Accounts Receivable—Kids Time. 4. Write the source document number. Lesson 4-3, page 79 PAID CASH TO OWNER FOR PERSONAL USE August 12. Paid cash to owner for personal use, $100.00. Check No. 6. Barbara Treviño, Drawing Debit Normal Balance 100.00 2. How is each account classified? Barbara Treviño, Drawing is an owner’s equity account. Cash is an asset account. 3. How is each classification changed? Withdrawals are increased. (This results in a decrease in owner’s equity.) Assets are decreased. Cash Debit Normal Balance 4. How is each amount entered in the accounts? Owner’s equity accounts decrease on the debit side. Assets decrease on the credit side. 100.00 1. Which accounts are affected? Barbara Treviño, Drawing Cash Lesson 4-3, page 80 PAID CASH TO OWNER FOR PERSONAL USE August 12. Paid cash to owner for personal use, $100.00. Check No. 6. 1 4 2 3 1. Write the date. 2. Debit Barbara Treviño, Drawing. 3. Credit Cash. 4. Write the source document number. Lesson 4-3, page 80 TO DO: Work Together, pg 80 On your own, pg 80 Application Problems 4-2, 4-3 Chapter 4-4: Starting a New Journal Page A COMPLETED JOURNAL PAGE Lesson 4-4, page 82 STARTING A NEW GENERAL JOURNAL PAGE If only 1 line left on a journal page, record the ENTIRE transaction on the next journal page. Easier to verify debits and credits. First write in the page number in top right corner. Lesson 4-4, page 83 Standard Accounting Practices Errors – Cancel the error by neatly drawing a line through the incorrect item and writing the correct item immediately above the canceled item. Errors caught before next entry – Draw neat lines through the errors and write correct entry on next blank lines. Errors caught after other entries have been journalized – Draw neat lines through the errors and write in corrections above them. Abbreviations – Only permitted when space is limited. Dollars and cents signs not used in journalizing. Two zeros are written in cents column, despite whether your entry contains whole numbers. Use a ruler to draw lines for corrections. STANDARD ACCOUNTING PRACTICES 4 1 6 2 3 5 5 Lesson 4-4, page 84 TO DO: Work Together, pg 85 On your own, pg 85 Application Problems 4-1, 4-2, 4-3, 4-4, 4-5