Using Financial

Information and Accounting

Chapter 14

I. Purpose of Accounting

A. Who uses financial reports and accouning information?

1. Financial reports give information about a company’s

past, present and future performance to:

a. Managers - use reports to make decisions about firm’s

operations

b. Employees - to see the financial wealth of the org., to see

how individual efforts helped

c. Investors and customers -use reports to make

investment and purchasing decisions

d. Suppliers, creditors, and government agencies - use reports

to determine their relationship with the org.

II. Types of Accountants

A. Public Accountants - independent accountant

who serves organizations & individuals on a fee

basis; offers a wide range of services

1. auditing

2. Tax returns

3. Financial statement preparation

4. consulting

B. Private Accountants

C. Fund and not-for-profit accountants

(charities, hospital, gov’t, schools)

III. Basic Accounting Procedures

A. The Accounting Equation

Assets = Liabilities + Owners’ Equity

–

–

–

–

–

–

–

assets

liabilities

owners’ equity

revenues

expenses

net income

double-entry bookkeeping (debits, credits)

B. The Accounting Cycle

1. Analyze business

transaction documents

2. Record business

transactions in journal

3. Post entries

to ledgers

4. Prepare trial balance

5. Prepare financial

statements &

management reports

6. Analyze reports

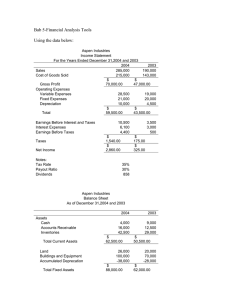

IV. The Balance Sheet

• Summarizes a firm’s financial position at a

specific point in time (on a specific date)

A. Assets (resources)

current, fixed, intangible, depreciation

B. Liabilities (obligations)

current, long-term

C. Equity(Assets minus obligations)

retained earnings

V. The Income Statement

• Summarizes the firm’s revenues & expenses

and shows total profit or loss over a period

of time

A. Revenues

gross sales, net sales

B. Expenses

cost of goods sold, operating expenses

C. Net profit or loss

VI. The Statement of Cash Flows

• Summarizes the money flowing into and out

of a firm for a period of time

A. Sources of cash flow:

1. operating activities

2. investment activities

3. financing activities

VII. Analyzing Financial Statements

A. Ratio analysis: calculating & interpreting financial

ratios taken from financial reports to assess a firm.

1. liquidity ratios - measures firm’s ability to

pay its short-term debt

a. current ratio

b. acid-test (quick) ratio

c. net working capital

Ratio Analysis (Cont’d)

2. Activity Ratios - indicates how efficiently the

firm uses its assets to generate revenue

a. accounts receivable turnover

b. inventory turnover

3. Profitability ratios - measures operating success

a. net profit margin

b. return on equity

c. earnings per share

4. Debt ratios - measures a firm’s ability to

pay its long-term debt

a. debt to equity ratio

VIII. Trends in Accounting

• Accountants expand their role

– more involvement in operations, advise clients

on systems, software, and acctg. regulations

• Valuing knowledge assets

– R&D, brands, trademarks, employee talent

• Tightening the GAAP

– reducing loopholes, cleaning up records

0

0