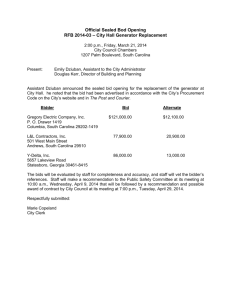

Lecture 4

advertisement

EC941 - Game Theory

Lecture 4

Prof. Francesco Squintani

Email: f.squintani@warwick.ac.uk

1

Structure of the Lecture

Juries and Information Aggregation

Auctions with Private Information

2

Juries

In a trial, jurors are presented with evidence on the guilt

or innocence of a defendant.

They may interpret the evidence differently.

Each juror votes either to convict or acquit the

defendant.

A unanimous verdict is required for conviction: the

defendant is convicted if and only if every juror votes

to convict her.

3

In deciding how to vote, each juror considers the costs

of convicting an innocent person and of acquitting a

guilty person, on the basis of her information.

When voting, she conditions her choice on being

pivotal, i.e. changing the outcome of the trial.

The event of being pivotal is informative: It gives the

juror information about the private information held by

the other jurors, as this determines their votes.

4

A Model of Jury Vote

Each juror comes to the trial with the belief that the

defendant is guilty with probability π.

Given the defendant’s status (guilty or innocent), each

juror receives a signal.

The probability that the signal is “guilty” when the

defendant is guilty is p, and the probability that the

signal is “innocent” if the defendant is innocent is q.

Jurors are likely to interpret the evidence correctly:

p > 1/2 and q > 1/2, and hence p > 1 − q.

5

Each juror wishes to convict a guilty defendant and acquit

an innocent one.

Each juror’s payoffs are:

−z if innocent defendant convicted

−(1 − z) if guilty defendant acquitted.

0 if an innocent defendant is acquitted,

or if a guilty defendant is convicted.

6

Let r be the probability of the defendant’s guilt, given a

juror’s information.

Her expected payoff if the defendant is acquitted is

−r(1 − z) + (1 − r) · 0 = −r(1 − z)

and her expected payoff if the defendant is convicted is

r · 0 − (1 − r)z = −(1 −r)z.

She prefers the defendant to be acquitted if r < z, and

convicted if r > z.

7

Bayesian Game of Jury Vote

Players The set of n jurors.

States The states are the set of all profiles (X, s1, . . . ,

sn) where X ∈ {G, I} and sj ∈ {g, b} for every juror j.

X = G if the defendant is guilty,

X = I if she is innocent.

si = g if player i receives the signal “guilty,”

si = b if player i receives the signal “innocent.”

8

Strategies The set of strategies of each player is

v = {C, Q}, where C is voting to convict,

and Q is voting to acquit.

Types Each player i’s type consists in a signal si together

with the set of all profiles (X, s-i), where s-i denotes i’s

opponents signals.

9

Beliefs Type g of a player i believes that the state is

(G, s1, . . . , sn) with probability πpk−1(1− p)n-k

and (I, s1, . . . , sn) with probability (1−π)qk−1(1− q)n-k,

where k is the number of players j (including i) with sj=g.

Type b believes that the state is

(G, s1, . . . , sn) with probability πpk(1− p)n-k-1

and (I, s1, . . . , sn) with probability (1−π)qn-k-1(1− q)k,

where k is the number of players j for whom sj = g.

10

Payoff functions The payoff function of each player i is:

ui(v, X) = 0

if v = (C,...,C) and X=I

or if v = (C,...,C) and X=G,

ui(v, X) = −z

if v = (C,...,C) and X = I

ui(v, X) =−(1 − z)

if v = (C,...,C) and X = G,

where X is the first component of the state,

giving the defendant’s true status.

11

Bayesian Nash Equilibrium

One juror Suppose there is a single juror with signal b.

To see if she prefers conviction or acquittal, we find the

probability Pr(G|b) that the defendant’s is guilty.

By the Bayes’ Rule:

Pr(G|b) = Pr(b|G)Pr(G)/[Pr(b|G)Pr(G)+Pr(b|I)Pr(I)]

= (1 − p)π /[(1 − p)π + q(1 − π)].

The juror votes Acquittal if and only if

z ≥ (1 − p)π / [(1 − p)π + q(1 − π)].

12

Suppose there are n jurors.

We show that truthful voting is not a Bayesian Equilibrium.

Suppose by contradiction that every juror other than 1

votes truthfully (acquit if her signal is b, convict if it is g).

Consider type b of juror 1. Her vote has no effect on the

outcome unless every other juror’s signal is g.

Hence, she votes Acquittal if the probability Pr(G|b,g,..., g)

that the defendant is guilty, given juror 1’s signal is b and

every other juror’s signal is g, is at most z.

13

Specifically,

Pr(G|b,g,...,g) = Pr(b,g,...,g|G)Pr(G)

/[Pr(b,g,...,g|G)Pr(G)+Pr(b,g,...,g|I)Pr(I)]

=(1 − p)pn-1π/[(1 − p) pn-1π + q(1 − q) n-1(1 − π)].

Hence, type b of juror 1 optimally votes for acquittal if

z ≥ (1 − p)pn-1π/[(1 − p)pn-1π+q(1 − q)n-1(1 − π)]

= 1 /{1 +q/(1 − p) [(1 − q )/p]n-1 (1−π)/π}.

Hence, unless z is large or n is small, voting truthfully is

not a Bayesian Nash Equilibrium.

14

Under some conditions there is a symmetric mixed strategy

equilibrium in which each type g juror votes for conviction,

and each type b juror randomizes.

Denote by β the mixed strategy of each juror of type b.

Each type b juror is indifferent between voting conviction

and acquittal.

Hence the mixed strategy β is such that:

z = Pr(G | signal b, n−1 votes for C)

15

Pr(b|G)(Pr(vote C| G))n−1Pr(G)

z=

Pr(b|G)(Pr(vote C|G))n−1Pr(G)+Pr(b|I)(Pr(vote C|I))n−1Pr(I)

(1−p)(p+(1−p)β) n−1π

(1−p)(p+(1−p)β)n−1π +q(1−q+qβ) n−1(1 − π)

The condition that this probability equals z implies

(1−p)(p+(1−p)β)n−1π(1 − z) = q(1 − q + qβ)n−1(1 − π)z.

hence:

where

β = [pX − (1 − q)] /[ q − (1 − p)X],

X = {π(1 − p)(1 − z)/[(1 − π)qz]}1/(n-1).

16

When n is large, X is close to 1, and hence β nears 1:

a juror who interprets the evidence as pointing to

innocence very likely nonetheless votes for conviction.

An interesting property of this equilibrium is that the

probability that an innocent defendant is convicted

increases as n increases: the larger the jury, the more likely

an innocent defendant is to be convicted.

I.e., Pr(C,n|I) = {1 – (1-β)(1-q)}n increases in n.

17

First-Price Auctions

In a sealed-bid second price auction, the winner pays a

price equal to second-highest bid.

In the case of complete information, this auction is

strategically equivalent to the “English” auction.

In a sealed-bid first price auction, the winner pays a

price equal to her bid.

This auction is equivalent to a “Dutch” auction.

18

In a Dutch auction, the ask price for a good is

decreased until the one bidder accepts to buy.

Under complete information, strategic choices are

equivalent in second-price auctions and Dutch auctions.

Each bidder decides, before bidding begins, the most

she is willing to bid.

To win, a bidder needs to bid the highest bid, and will

pay a price equal to her bid.

19

First-Price Auction Game

Players: n bidders. Bidder i’s valuation is vi, we order

v1> … > vn > 0, without loss of generality.

Strategies: bidder i’s maximal bid is bi.

Let bi = max {bj : j different from i}.

Payoffs: ui(b1, … ,bn) = vi - bi if bi > bi

0

if bi < bi

20

Nash Equilibrium

One N.E. is: (b*1,… , b*n) = (v2, v2, …, vn).

Bidder 1 wins the object, payoff: v1 - b*1 = v1 - v2 > 0.

If bidding b1 < v2, she loses the object, the payoff is 0.

If bidding b1 > v2, her payoff is v1 - b2 < v1 - v2 .

The payoff of bidders i = 2, …, n is 0.

If bidding bi > vi, the payoff is vi - bi < 0.

If bidding bi < v2, she loses the object, the payoff is 0.

21

There are many other Nash Equilibria.

In all equilibria, the winner has the highest valuation.

Take any profile (b1, ..., bn) such that player i = 1 wins.

If bi > vi, then i’s payoff is negative, i can improve her

payoff by bidding zero.

If bi < vi, then player 1 can increase her payoff from

zero to v1 - bi - e >0 by bidding bi + e.

22

Auction and Private Information

We use Bayesian games to model auctions in which

bidders do not know each others’ valuations.

If each bidder i’s type is simply her valuation vi,

we say that the bidders’ values are private.

If each bidder’s valuation depends also on other

bidders’ types, we say that values are common.

(E.g., auctions for natural resources exploitation rights).

23

Second Price Auctions

with Private Values

Players: n bidders.

Types: Each bidder i’s type is her valuation is vi.

Strategies: bidder i’s maximal bid is bi.

Payoffs: ui(b1, … ,bn, v) = vi - bi

if bi > bi

0

if bi < bi

where, bi = max {bj : j different from i}.

24

The profile (b*1,… , b*n) = (v1, …, vn) is the unique

weakly dominant solution.

Although valuations are now private information, the

unique weakly dominant solution is the same as in the

complete information case.

The proof is entirely analogous to the case of complete

information.

25

Weakly Dominant Solution

The strategy profile (b*1,… , b*n) = (v1, …, vn) is the

unique weakly dominant solution.

b < bi or

bi < bi < vi or

bi =bi & i wins bi=bi & i loses

b i > vi

bi < vi

vi - bi

0

0

bi = vi

vi - bi

vi - bi

0

26

bi < vi

bi = vi

vi - bi

bi > vi

vi - bi

vi < bi < bi or

bi > bi or

bi =bi & i wins

bi =bi & i loses

0

vi – bi (< 0)

0

0

In sum, bidding bi = vi yields at least as high a payoff as

bidding bi > vi or bi < vi for any opponents’ bids.

27

First Price Auctions

with Private Values

Players: n bidders.

Types: each bidder i’s type is her valuation vi.

Strategies: bidder i’s maximal bid is bi.

Payoffs: ui(b1, … ,bn, v) = vi - bi

if bi > bi

0

if bi < bi

where, bi = max {bj : j different from i}.

28

Nash Equilibrium

Say that each vi is independently drawn from a strictly

increasing and differentiable cumulative distribution

function F, with F(v-) = 0 and F(v+) = 1.

Focus equilibria with strategies that are differentiable,

increasing in the type, and symmetric across players.

To find the equilibrium, first find conditions satisfied

by the players’ best response functions, and then

impose that strategies are best response to each other.

29

Denote the bid of type vi of player i by b(vi).

The expected payoff of a player of type v who bids bid

b when every other player’s strategy is b is

(v-b)Pr{All other bids < b} = (v-b)F(b-1(b))n-1.

To find the best response when every other player’s

strategy is b, we take the first-order conditions

-F(b-1(b))n-1 +(v-b)(n-1) F(b-1(b))n-2 F’(b-1(b))/b’(b-1(b))=0

30

For (b,... , b) to be a Nash equilibrium, the bid b(v)

must be the best response for every type of v, when

every other player adopts the strategy b.

I.e., the bid b = b(v) must satisfy the previous first

order conditions.

Hence, the equilibrium condition is, for all v:

-F(v)n-1 +(v-b(v))(n-1)F(v)n-2 F’(v)/b’(v)=0

or

F(v)n-1b’(v)+b(v)(n-1)F(v)n-2 F’(v)=v(n-1)F(v)n-2 F’(v).

31

Integrating both sides of the differential equation,

v

F(v)n-1b(v)= x(n-1)F(x)n-2 F’(x) dx.

v Integrating by parts the right hand side,

v

F(v)n-1b(v) = - F(x)n-1 dx + vF(v)n-1.

v We verify that b*(v) is increasing: (b*,…, b*) is B.N.E.,

v

b*(v) = v- F(x)n-1 dx/F(v)n-1.

v

32

Revenue Equivalence

Suppose that n risk neutral bidders compete in a sealedbid auction, in which the highest bidder wins the good.

(These auctions include first-price auctions, secondprice auctions, all-pay auctions, etc.).

Suppose that each bidder independently receives a

signal from the same continuous and increasing

cumulative distribution, and has a valuation that

depends continuously on all the bidders’ signals.

33

Consider any symmetric Nash equilibrium with

differentiable, increasing strategies, and such that the

expected payoff of a bidder with the lowest possible

valuation is zero.

Given the opponent’s equilibrium strategies, each

player’s bid affects her winning probability p and

expected equilibrium payment e(p).

So, we can think of each bidder’s equilibrium bid choice

as just choosing a value of p.

34

The problem of a bidder with valuation v is:

maxp pv - e(p)

Let the solution be p*(v), the first-order condition gives

v = e’(p*(v)) for all v.

Integrating both sides of this equation, we have

v

e(p*(v)) = e(p*(v-)) + x dp*(x).

v35

Because the good is sold to the bidder with the highest

valuation,

p*(v) = Pr{vj < v, for n-1 bidders j}= Pr(X<v),

where X is the highest of n-1 independent valuations.

The probability of winning is independent of the

detailed rules of the auction.

Because the expected payoff of a bidder with valuation

v- is zero, e(p*(v-)) = 0; hence, the expected payment of

any player of type v is e(p*(v)) = Pr(X<v)E[X|X<v],

independently of the detailed rules of the auction.

36

We obtain the following result.

Theorem (Revenue Equivalence Principle). Suppose that

each bidder (i) is risk neutral, (ii) independently receives a signal

from the same continuous and increasing cumulative distribution,

and (iii) has a valuation that depends continuously on all the

bidders’ signals. Consider auctions in which the highest bidder wins

the good. Consider any symmetric Nash equilibrium with increasing

strategies, and such that the expected payoff of a bidder with the

lowest possible valuation is zero. The expected payment of a bidder

of any given type is the same regardless of the auction rules, and

hence also the auctioneer’s expected revenue is the same.

37

Summary of the Lecture

Juries and Information Aggregation

Auctions with Private Information

38

Preview of the Next Lecture

Definition of Extensive-Form Games

Subgame Perfection and Backward Induction

Applications: Stackelberg Duopoly, Harris-Vickers Race.

39