Annexure B - Cost Breakdown - The National School of Government

advertisement

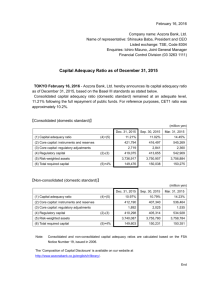

Cost Breakdown Matrix Annexure B to Terms of Reference Project Objective/Scope Partner/Director GENERAL MANAGEMENT OF THE INTERNAL AUDIT FUNCTION Rate Review of Internal Audit and Audit Committee Charters Rate Preparation of three year Strategic Plan and one year Internal Audit Plans Rate Facilitation of risk assessment workshops Rate Quarterly Reporting and Attendance of Audit Committee Meetings Rate Preparation and Attendance of Risk Committee Meetings Rate Attendance of EMC meetings Rate Liaison with Auditor General Rate Overall project management including client interaction EXECUTION OF INTERNAL AUDITS Rate Training Management Manager Assistant Manager Senior Internal Auditor Junior Auditor Total Y1 Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Evaluate the measures instituted by management to ensure the economical, efficient and effective use of resources. The reviews will cover the following areas: Quality of trainers and partnerships. Quality of training materials and response time to changes in public sector. Accessibility of resources from international partners. Monitoring and evaluation of training delivery. Change Management Review adequacy and effectiveness of controls on change management strategy. Review the adequacy and effectiveness of controls to ensure appropriate transitional structure to the NSG's requirements. Review the adequacy and effectiveness of controls to ensure compliance to the policies and regulatory requirements set for National Departments. Rate Total Y2 Total Y3 Cost Breakdown Matrix Annexure B to Terms of Reference Review the adequacy and effectiveness of controls to ensure transparent and effective communication with stakeholders within and outside NSG. Review the adequacy and effectiveness of controls to ensure monitoring and approval of implementation plan. Assets and Resources Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Review of Knowledge and information Management strategy: Obtain and review the adequacy and completeness of the Knowledge and Information Management Strategy. Perform interviews with the Business and ICT Management team to confirm their strategic direction and input to Knowledge and Information Management. Assess the logical access to Knowledge and Information Management infrastructure. Governance Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Review the adequacy and effectiveness of controls to ensure: Political support for the School of Government (Stakeholder Management). Government focus on skills development for Management staff and up in the Public Service. Governance committees are in place and are effective. Delegations of authority in place. Specific sectorial platform for engagement with HR Development practitioners across national provincial departments. National forum of public service trainers. Engagement through Governance and Administration cluster. Information and Integrity Reliability Review of Master Systems Plan: -Approval of plan Cost Breakdown Matrix Annexure B to Terms of Reference -MSP plan is aligned to ICT objectives and strategy -Plan is properly funded -The implementation of the plan is monitored by management. -The plan is reviewed on a regular basis to accommodate emerging risks relating to ICT. Financial Management Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Review the adequacy and effectiveness of controls in place to ensure adequate funds and skills to implement the approved strategy and the following: MTF process. Internal Budgeting process. Debtors’ management. In year monitoring of the budget (monthly Management accounts and reporting against revenue targets). Human Resources capacity including skills assessment. Information Technology(CAATs Review) Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Identify employees with banking details that match supplier’s banking details Identify duplicate suppliers accounts. Performance Information Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Review the Performance Information policies for adequacy, effectiveness and compliance with the relevant legislation e.g. the National Treasury Framework for Managing Programme Performance Information. Review of the SMART criteria assessment (as per the Framework for Managing Programme Performance Information issued by National Treasury) of the performance objectives, performance indicators and targets. Review of the alignment of the objectives, performance indicators and targets between the Strategic Plan, the Annual Performance Plan. Pre-Annual Auditing of Performance information evidence files using 1st and 2nd quarter reports. Human resources capacity which impacts on the achievement of set objectives. Cost Breakdown Matrix Annexure B to Terms of Reference Finance( Financial Discipline Controls Review) Review key controls implemented by management over the financial discipline Revenue and receivables o Review controls relating to the completeness, accuracy and validity of recorded revenue and related receipts; o Evaluate the controls around debtor’s management, including payment terms per contract, penalties charged on overdue accounts and monitoring of long outstanding debtors; and o Financial and operational controls in the following areas will be addressed: Credit control; Order processing; Invoicing; and Receipts from customers. Procurement and Accounts Payable o Evaluate the design and effectiveness of processes and controls to ensure that expenditure and related payments are valid, accurate and completely recorded. o Financial and operational controls in the following areas will be addressed: Ordering and procurement; Receiving; Supplier payments; Sundry expenses; Bank and Cash o Evaluate the design and effectiveness of processes and controls over cash and banking activities to ensure that they are valid, accurate and completely recorded; and o Financial and operational controls in the following areas will be addressed: Banking and cash receipts; Bank Reconciliations; EFT Payments; Petty cash Manual invoices Physical security. TOTAL Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Rate Hour Cost Cost Breakdown Matrix Annexure B to Terms of Reference