0324585942_131635

advertisement

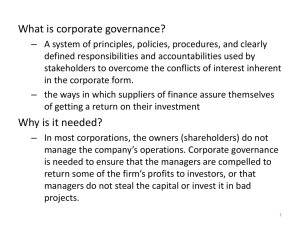

Chapter 16 Governing the Corporation LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Differentiate various ownership patterns around the world 2. Articulate the role of managers in both principal-agent and principal-principal conflicts 3. Explain the role of the board of directors 4. Identify voice- and exit-based governance mechanisms and their combination as a package 5. Acquire a global perspective on how governance mechanisms vary around the world 6. Articulate how institutions and resources affect corporate governance 7. Participate in two leading debates on corporate governance 8. Draw implications OWNERSHIP AND CONTROL concentrated ownership and control - founders start up firms and completely own and control them on an individual or family basis diffused ownership - publicly traded corporations owned by numerous small shareholders but none with a dominant level of control separation of ownership and control - dispersal of ownership among many small shareholders, in which control is largely concentrated in the hands of salaried, professional managers who own little (or no) equity FAMILY OWNERSHIP vast majority of large firms throughout continental Europe, Asia, Latin America, and Africa feature concentrated family ownership and control family ownership and control may provide better incentives for the firm to focus on long-run performance may also minimize the conflicts between owners and professional managers may lead to the selection of less qualified managers (who happen to be the sons, daughters, and relatives of founders), the destruction of value because of family conflicts, and the expropriation of minority shareholders STATE OWNERSHIP state-owned enterprises (SOEs) suffer from an incentive problem and often perform poorly in theory, all citizens (including employees) are owners, in practice, they have neither rights to enjoy dividends generated by SOEs (as shareholders would) nor rights to transfer or sell “their” property SOEs are de facto owned and controlled by government agencies far removed from ordinary citizens and employees there is little motivation for SOE managers and employees to improve performance, which they can hardly benefit from personally PRINCIPAL - AGENT CONFLICTS top management team (TMT) - group, led by the chief executive officer (CEO), that represents another crucial leg of the corporate governance tripod agency relationship - relationship between shareholders (principals) and professional managers (agents) principals - persons (such as owners) delegating authority agents - persons (such as managers) to whom authority is delegated PRINCIPAL - AGENT CONFLICTS agency theory - simple yet profound proposition: to the extent that the interests of principals and agents do not completely overlap, there will inherently be principal agent conflicts agency costs - result of principal-agent conflicts: principals’ costs of monitoring and controlling agents agents’ costs of bonding signaling that they are trustworthy information asymmetries - dynamic between principals and agents; agents such as managers almost always know more about the property they manage than principals do PRINCIPAL-PRINCIPAL CONFLICTS principal-principal conflicts - conflicts between two classes of principals: controlling shareholders and minority shareholders expropriation - activities that enrich controlling shareholders at the expense of minority shareholders tunneling - form of corporate theft that occurs when managers from the controlling family divert resources from the firm for personal or family use related transactions - legal means whereby controlling owners sell firm assets to another firm they own at below market prices or spin off the most profitable part of a public firm and merge it with another private firm of theirs BOARD OF DIRECTORS inside directors - top executives of a firm outside directors - nonmanagement members of the board CEO duality – when CEO serves as board chair interlocking directorate - one person affiliated with one firm sits on the board of another firm ROLE OF BOARD OF DIRECTORS control - effectively control managers service - advising the CEO resource - acquisition functions Boards’ effectiveness in serving the control function stems from their independence, deterrence, and norms GOVERNANCE MECHANISMS voice-based mechanisms - willingness of shareholders’ to work with managers, usually through the board, by “voicing” their concerns pay-for-performance link in executive compensation is usually not very strong boards may have to dismiss underperforming CEOs GOVERNANCE MECHANISMS exit-based mechanisms - means by which corporate control is gained from external sources when shareholders no longer have patience and are willing to “exit” by selling their shares threat of takeovers does limit managers’ divergence from shareholder wealth maximization private equity - acquisition of a significant portion or a majority control in a more mature firm leveraged buyouts (LBOs) - means by which private investors, often in partnership with incumbent managers, issue bonds and use the cash raised to buy the firm’s stock INSTITUTIONS AND CORPORATE GOVERNANCE given reasonable investor protection, founding families may over time feel comfortable becoming minority shareholders of the firms they founded when formal legal and regulatory institutions are dysfunctional, founding families must run their firms directly absent investor protection, bestowing management rights to outside professional managers may invite abuse and theft corporate governance ultimately is a choice about political governance RESOURCES AND CORPORATE GOVERNANCE VRIO framework ability to successfully list on a high profile exchange such as the NYSE and LSE is valuable, rare, and hardto-imitate managerial human capital - these resources, such as the social networks of executives, are unique and likely to add value top managerial talents are hard to imitate - unless they are hired away by competitor firms. within an organizational setting (in TMTs and boards) that managers and directors at the top of an organization can make a world of difference OPPORTUNISTIC AGENTS vs. MANAGERIAL STEWARDS Agency theory assumes managers are agents who may engage in self-serving, opportunistic activities if left to their own devices. However, critics contend that most managers are likely to be honest and trustworthy. Stewardship theorists agree that agency theory is useful when describing a certain portion of managers and under certain circumstances. If all principals view all managers as selfserving agents with control mechanisms to put managers on a “tight leash,” some managers, who initially view themselves as stewards, may become so frustrated that they end up engaging in the very self-serving behavior agency theory seeks to minimize. GLOBAL CONVERGENCE vs. DIVERGENCE Is corporate governance converging or diverging globally? Convergence advocates argue that globalization unleashes a “survival-of-thefittest” process by which firms will be forced to adopt globally best practices. Critics contend that governance practices will continue to diverge throughout the world.