Economics definitions

advertisement

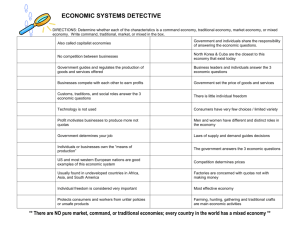

Economics Traditional Economies Basic economic questions answered by what has been done in the past. Traditions are maintained. The economic system in which resources are inherited, and which has a strong social network and is based on primitive methods and tools. It is strongly connected to subsistence farming. Ritual, Habit, and Custom. Individual roles and choices are defined by the customs of elders and ancestors. These economies are usually based in societies of hunter/gatherers. Sharing is a big part of these economies. They barter for goods, they don’t buy and sell. How do traditional economies answer the three basic questions? 1) What to produce? Whatever ritual, habit or custom dictates 2) How to produce? However ritual, habit or custom dictate 3) For whom to produce? For whomever ritual, habit or custom dictate Command Economies - The most important aspect of this type of economy is that all major decisions related to the production, distribution, commodity and service prices, are all made by the government or centralized authority. Basic economic questions answered by the government (central authority) How do command economies answer the basic economic questions? 1) What to produce? Whatever the government says to produce 2) How to produce? However the government tells you to produce 3) For whom to produce? For whomever the government tells you to produce Market Economies - In a market economy, national and state governments play no role. Consumers and their buying decisions drive the economy. Basic economic questions answered by consumers by deciding what to buy and private businesses by deciding what to make and sell How do market economies answer the basic economic questions? 1) What to produce? Whatever consumers will buy 2) How to produce? In whatever way is most cost effective to produce goods or services that consumers will buy 3) For whom to produce? For whomever will buy the product Specialization – “Do what you do best; trade for the rest!” • Attempting to produce everything single product you want inside your own nation is not the best use of your nation's resources. • By specializing in what you have the natural and human resources best suited to produce, you can do that "best", and use your profits to purchase things other nations are better suited at producing. • Specialization and trading goods services with others can help everyone. Specialization encourages trade and can be a positive factor in a country’s economy. Sometimes, specialization has not functioned as expected. Some potential problems of overspecialization include single-resource economies and lack of diversification. Currency Exchange Before people from different countries can buy or sell anything to each other, they have to solve a basic problem. Buyers have to be able to change their money from their country's currency to the seller’s national currency. Exchange rates provide a procedure for determining the value of one country’s currency in terms of another countries’ currency. Without a system for exchanging currencies, it would be very difficult to conduct international trade. Without a method of currency exchange, world trade would drop drastically. You wouldn't be wearing a shirt made in Asia, or eating an apple grown in New Zealand. Barriers to Trade A tariff is a tax placed on goods that one nation imports from another. Many nations use tariffs to protect their industries from foreign competition. Tariffs provide protection by acting to raise the price of imported goods. Thus, consumers will often buy the cheaper domestic products, and domestic industries will benefit. Import quotas offer another means of protectionism. These quotas set a limit on the amount of certain goods that can be a country and are more drastic than protective tariffs when consumers are willing to pay a higher price for an imported good. Quotas, because they limit supply, result in even higher prices, and the supply may even run out, leaving consumers with no choice but to purchase domestic goods. An embargo is an order designed to stop the movement of goods. An embargo, issued by the government of one country, may restrict or suspend trade between that country and another nation. A government may impose an embargo to hamper the military efforts of another government. For example, the United States prohibits the export of weapons to countries that sponsor terrorism. Sometimes a government imposes an embargo to express its disapproval of actions taken by another government. The embargo is intended to pressure the offending government to change its actions. Factors of Production There are four factors – land, labor, capital, and entrepreneurship - that influence economic growth. Economic growth is usually measured by calculating the percent increase in GDP from one year to the next. This is known as the GDP Growth Rate. These are the resources that influence economic growth: LAND: This category sometimes extends over all natural resources. Land is the basic raw materials—vegetation, animals, minerals, fossil fuels--that are needed for the production of goods. A material source of wealth, such as timber, fresh water, or a mineral deposit, that occurs in a natural state and has economic value LABOR: human effort used in production which. This is your human effort. Labor is the resource that does the "hands on" work of transforming raw materials into goods or provides a service. ENTREPRENEURSHIP: Entrepreneurship is a special sort of human effort that takes on the risk of bringing labor, capital, and land together and organizing production. Entrepreneurs combine the other factors of production, land, labor, and capital in an innovative way to make a profit. PHYSICAL CAPITAL (also known as CAPITAL RESOURCES or CAPITAL GOODS): human-made goods which are used in the production of other goods. These include machinery, tools, factories and other buildings and their furnishings, vehicles, and technology. HUMAN CAPITAL: education and training of workers whether formal or on-the-job Relationship of investment in capital goods and human capital to GDP Investment in improving a nation's capital resources (buying new machines, building new factories, etc.) and/or human capital (investing in improving your workers training and education) results in economic growth and improved GDP. Failure, or the inability, to improve these types of capital results in no growth of GDP. So, increasing literacy rates should improve GDP. Highly developed economies like the USA and Israel have smaller growth rates because the sizes of these economies are already so large. Nations which have valuable minerals such as diamonds, gold, uranium, and/or petroleum can profit from the income that the extraction and sale of these minerals, which will increase the national GDP. Sometimes this money is stolen by corrupt leaders, but when the income is used to improve the nation's infrastructure the citizens may benefit. Vocabulary Gross domestic product (GDP) - value of all goods and services produced within a country Industrialized countries – countries that rely more on industry than agriculture Literacy rate - percent of people who can read and write Developing countries – countries in different stages of moving toward development Free enterprise – another name for a market economy Market economy – an economy in which business owners and consumers make decisions about what to make, sell, and buy. An economic system in which people, not government, decide what to make, sell, or buy; Command economy – an economy in which the government owns most of the industries and makes most of the economic decisions Traditional economy – exchange of goods or services based on custom and tradition One-resource economy – economy based on a single resource or crop. Exports – products a country sells to other countries Imports – products a country buys from other countries Interdependence – depending upon another country for resources or goods and services Population density – the average number of people living within a set area Economics – Economics is the study of the production and distribution of goods and services, it is the study of human efforts to satisfy unlimited wants with limited resources.