Kaltenbrunner – Developing Countries in the Global Financial Crisis

advertisement

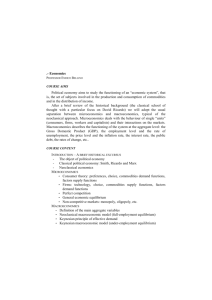

Developing Countries in the Global Financial Crisis: A Minskyan Account Annina Kaltenbrunner Lecturer in the Economics of Globalisation & The International Economy Leeds University Business School Motivation 1,800 17 1,600 15 1,400 13 1,200 11 1,000 9 800 7 600 5 400 3 200 0 1 Brazilian Real Mexican Peso Turkish Lira South African Rand Polish Zloty Korean Won (RHS) Outline Neoclassical Models of Financial (Foreign Exchange) Crisis Post Keynesian Theories of Financial Crisis Keynes: Chapter 12 of the General Theory Hyman Minsky: The Financial Instability Hypothesis > Policy Implications and Open Economy Applications Developing Countries (Brazil) in the Global Financial Crisis (September 2008) Neoclassical Models Overview First Generation Models (Krugman 1979) Rational speculators attack central bank in face of fundamental disequilibria (current account and/or fiscal deficit) Second Generation Models (Obstfeld, 1996) Self fulfilling expectations about deteriorating fundamentals – Government “Trade-off ” Third (Asian) Generation Models (e.g. McKinnon and Pill, 1996; Radelet and Sachs, 1998; Chang and Velasco, 2002) Concern about external repayment capacity Net short-term external debt (“original sin”) Neoclassical Models Assumptions Efficient markets Underlying “real” fundamentals run the show (dichotomy between monetary and real) Heterodox approaches to Asian crisis (foreign currency debt) Rational agents First Generation: No doubt Third Generation/Asymmetric information: Constrained information (moral hazard and adverse selection) (Behavioural Finance: Heterogeneous) Neoclassical Models Policy Recommendations Fix Fundamentals Current account, fiscal balance, inflation etc. Reduce net foreign currency debt Develop domestic financial markets Accumulate foreign exchange reserves Asymmetric Information: Transparency Further reduce State involvement in financial markets (e.g. “rule-bound”, flexible exchange rates) Further open capital account (macroeconomic discipline, liquidity for domestic financial market etc.) Post Keynesian Theories of Financial Markets/Financial Crisis Monetary Production Economy Creative agency/expectations Fundamental Uncertainty (non-ergodicity) “Rationality” pointless Inter-subjective nature of price formation John Maynard Keynes General Theory: Chapter 12 What determines Investment? Rate of interest and the schedule of the marginal efficiency of capital Rate of Interest (GT: Chapters 13-17) Reward for parting with the security provided by money in a world of fundamental uncertainty and historical time >> money as “secure abode of purchasing power” and medium of contractual settlement (Paul Davidson) Marginal Efficiency of Capital Relation between the supply-price of capital asset and its prospective yield Chapter 12 Prospective Yield “The considerations upon which expectations of prospective yields are based are partly existing facts which we assume to be known more or less for certain, and partly future events which can only be forecasted with more or less confidence”…. ”We may sum up the state of psychological expectation which covers the latter as being the state of long-term expectation...” Chapter 12 Speculation Conventions and State of Confidence Conventions: “Assuming that the existing state of affairs will continue indefinitely, expect in so far as we have specific reasons to expect a change” Speculation vs. Enterprise Stock Market (Secondary Market) “It is as though a farmer, having tapped his barometer after breakfast, could decide to remove his capital from the farming business between 10 and 11 in the morning and reconsider whether he should return to it later in the week” Precariousness of Conventions Musical Chair/Beauty Contest Displaces enterprise Chapter 12 Speculation “Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes a bubble on a whirlpool of speculation. When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done”. Chapter 12 Summary and Policy Implications Swings in asset prices detached from “fundamentals” inherent feature of capitalist economies Worse in more liquid markets Negative implications for investment and capital formation Animal Spirit: spontaneous urge to action rather than inaction Policy Implications: Stabilizing conventions? Investment permanent and indissoluble >> Illiquidity? “Force” socially beneficial investment State investment Chapter 12 Applications and Extension Keynes: stock market Paul Davidson, John T. Harvey: foreign exchange market Sheila Dow: financial markets in general Alves et al. (among others): Asian financial crisis But: Keynes not a theory of financial crisis >>> Minsky Hyman Minsky The Financial Instability Hypothesis “John Maynard Keynes” (1975); “Stabilizing an Unstable Economy” (1986) Missing link in General Theory is finance (credit) – liability side of balance sheets Theory of inherent and endogenous fragility of financial markets and capitalist economies Balance sheet/Wall Street view of capitalist economies Financial fragility and instability due to changing cash flow configurations over the business cycle (profits vs. debt payments) >Financial Instability Hypothesis The Financial Instability Hypothesis Building Blocs 1. (Subjective) Expectations change over course of the cycle: stability breeds instability Rising investment > higher profits and rising asset prices > feedback to investment > boom/euphoria 2. Increasingly fragile financial structures - match between cash flow commitments (debt service and principal) and cash income (investment yields) Hedge: income meets interest rates and principal Speculative: income meets interest rates but not principal Ponzi: income does not cover interest rates >> Margin of safety falls >> Increased vulnerability to changing (financial) market conditions The Financial Instability Hypothesis Building Blocs 3. Endogenous “shock” (rise in interest rate) which turns fragility into instability Central bank raises interest rate to cool economy Banks raise interest rate reacting to high demand for external finance 4. Debt deflation (Fisher (1933)) Rising interest rates > higher borrowing costs, falling net-worth, lower credit ratings > inability to meet cash flow requirements Falling profits and asset prices Defaults > banking crisis The Financial Instability Hypothesis Summary and Policy Implications Financial instability and crisis inherent feature of capitalist economies with “mature” financial markets Financial crisis not due to misaligned fundamentals but increasingly fragile financial structures – balance sheets and cash flow requirements Policy Implications: Big Government > stabilize firm profits Big Bank > stabilize asset prices Regulate Finance The Financial Instability Hypothesis Applications and Extensions Capitalist firm > banks, households, states Open economy/Emerging Markets Exogenous shock? Exchange rate > “super-speculative” units (Arestis and Glickman, 2002) Developing Countries in the Global Financial Crisis 1,800 17 1,600 15 1,400 13 1,200 11 1,000 9 800 7 600 5 400 3 200 0 1 Brazilian Real Mexican Peso Turkish Lira South African Rand Polish Zloty Korean Won (RHS) Neoclassical Models Fundamentals and Foreign Currency Debt Table 1: Domestic Economic Fundamentals Current Account (%GDP) Primary Fiscal Surplus (%GDP) Public Sector Net Debt (%GDP) Inflation Index (CPI-IPCA) FX Reserves/Total External Debt (%) FX Reserves/Short-term External Debt (%) Dec06 1.3 3.8 45.9 3.1 49.7 211.7 Jun07 0.8 3.6 45.0 3.7 76.9 216.3 Dec07 0.1 3.9 43.9 4.5 93.3 289.9 Jun08 -1.0 3.9 41.8 6.1 97.7 312.2 Sources: BCB Economic Indicators and Brazilian Treasury Sep08 -1.7 4.1 40.9 6.2 98.2 296.8 Dec08 -2.2 3.6 38.5 5.9 104.3 349.8 Jun09 -1.2 3.0 41.2 4.8 104.7 349.7 Dec09 -1.3 2.6 42.1 4.3 120.6 455.2 Jun10 -2.1 2.9 40.0 4.6 110.7 367.6 Dec10 -2.1 3.0 39.2 5.9 112.4 371.4 Jun11 -2.0 3.0 38.6 6.7 115.1 437.7 Sep11 -2.1 3.1 36.3 7.3 117.3 474.9 Post Keynesian/Minskyan Account Unprecedented Amount of Capital Flows 80,000 Emergence of the Eurozone Crisis Emergence of the Global Financial Crisis 60,000 40,000 20,000 - Deepening of the Eurozone Crisis (20,000) (40,000) Global Crisis hit EME (60,000) Current Account Portfolio Flows Banking Flows Post Keynesian/Minskyan Account In complex, very short-term domestic currency assets 45 40 35 30 25 20 15 10 5 0 Derivatives - US$ Futures Derivatives - DI Futures Stock Exchange Domestic Public Debt Post Keynesian/Minskyan Account Which created Balance Sheet Vulnerabilities 150,000 100% 100,000 90% 80% 50,000 70% 0 60% -50,000 50% -100,000 40% -150,000 30% -200,000 20% -250,000 10% -300,000 0% Share of Local Currency Claims (RHS) International Investment Position (IIP) Short-Term Funding Gap International Investment Position (IIP) Strongly Short-Term Post Keynesian/Minskyan Account The Crisis “Shock” (rising interest rates and increased risk aversion in developing financial markets) Rising funding costs for international banks Speculative and Ponzi Units need to make position Do so in overexposed and liquid assets > Brazil Falling asset prices and exchange rate depreciation exacerbate financing difficulties > Stampede and exchange rate depreciation by 60% unrelated to Brazilian fundamentals Conclusions Neoclassical vs. Post Keynesian: Different Ontological assumptions of how financial markets (economic dynamics generally) work Neoclassical: stable underlying fundamentals which will be aligned with expectations as long as frictions are removed (government, noise traders etc.) Post Keynesian: Symbiotic relationship between real and finance; no underlying fundamentals; inherent fragility of financial markets and economic systems >>> State and Government Control