Indicator: Investment Returns - Resource Planning

advertisement

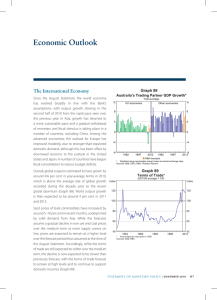

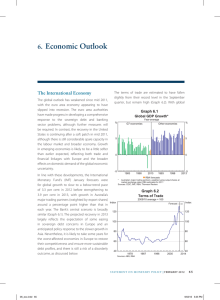

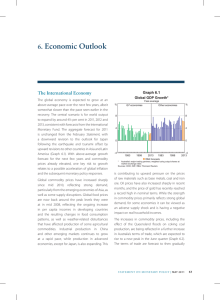

KEY BUDGET DRIVER FORECASTS 2013-14 to 2016-17 Key Budget Driver: Investment Returns Indicator: Interest Rates on Three-Month Treasury Bills Yields on Five-Year Government Bonds Foreign Equity and U of A Portfolio Returns Prepared by: Financial Services Section A: Industry/Sector Trends The Bank of Canada’s overnight target rate for the fiscal year was unchanged at 1.0%. The Bank of Canada has signaled future rate increases may be appropriate with firmer inflation numbers and reduced slack in the economy. During the year spreads on mid-term corporate bonds over government bonds widened out to recessionary levels. The yield curve flattened in the fiscal year as long term bond yields came down over 100 basis points. Inflation at March 31, 2012 was 1.9%, down from 3.3% a year earlier, as price gains in food and gasoline slowed. With the inflation rate below the Bank of Canada’s 2.0% target this will ease pressure on the Bank of Canada to hike interest rates. Strength of the Canadian dollar will also moderate imported inflation. With inflation in check, the Bank of Canada will consider economic performance and the employment rate when deciding on the direction of interest rates. The outlook is complicated by global developments, with continued political and economic uncertainty in Europe. Massive amounts of global fiscal stimulus are seen throughout the global economy, which could create a risk of future inflation, placing upward pressure on the long portion of the yield curve. However, given the present level of over- capacity in the economy the risk of inflation could be several years out. Canada’s real GDP declined to 2.5% in calendar 2011, following a 3.2% increase in 2010. The economy was affected by the earthquake and tsunami in Japan and declining Government of Canada capital spending. It is expected that the real GDP will grow at a moderate pace of 2.1% for the 2012 calendar year. With the U.S. economic recovery showing some resilience, the external headwinds on the Canadian economy have abated to a certain degree. The strong Canadian dollar, which has been trading near par with the US Dollar, will put a damper on the Canadian manufacturing sector. US real GDP is expected to grow by 2.3% in 2012. For the year ending March 31, 2012 fixed income markets and US equities posted gains, while Canadian and Non-North American equities had negative returns. Since March 31st, equity and commodity markets have retreated, the S&P/TSX is down 4.0% and the S&P 500 (in USD terms) is down 3.0% at May 4/12, partially from an economic uncertainty in the Eurozone and a slowdown in Asia. It is unclear as to whether this is a short term correction or signs of a prolonged market contraction. Section B: Trends within the University of Alberta The University has invested a portion of its outstanding cash in the Unitized Endowment Pool (UEP) and a proportion to mid-term bonds to capitalize on better returns from longer-term investments over the yields that can be earned on short-term money market products. Third party asset backed commercial paper (ABCP) which are now part of the mid-term strategy, were successfully converted into longer term notes that have a lower yield compared to other securities with comparable risk and duration characteristics due to associated administrative costs. In fact, the majority of the new notes pay interest at the 91-day Banker’s Acceptance rate less 50 basis points. The University of Alberta is forecasting a 7.25% return on the investment of its UEP based on collaborative work done over the past few years by the Board Investment Committee. Office of Resource Planning, University of Alberta 23/03/16 Section C: Key Budget Driver Forecasts Indicator: Investment Returns Annual Percentage Returns Indicator Interest Rates on 3 Month TB Forecast Yields on 5-Year Bonds Forecast Non-Endowed Return Forecast UEP Return Forecast 1 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 Actual Forecast Forecast Forecast Forecast Forecast 0.9%1 1.0% 1.6% 1.8% 2.0% 2.0% 1.76% 2.1% 2.7% 2.8% 3.0% 3.0% 2.11% 2.3% 2.8% 3.1% 3.3% 3.3% 3.0% 7.25% 7.25% 7.25% 7.25% 7.25% Bank of Canada average for the year Office of Resource Planning, University of Alberta 23/03/16