Eco. 5 Supply Review

advertisement

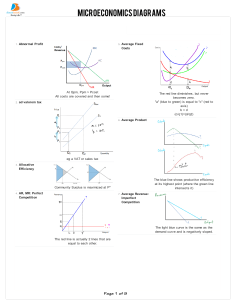

Chapter 5 Review *What is the definition of Supply? *What is the definition of the Law of Supply? *The Law of Supply takes into account what two groups of producers? *What is a Market Period? *Draw the Supply Curve for the following periods. Market Period Short Run Long Run *What is the definition of a Short Run? *What three things does a Short Run Supply Curve show? ####################################################### *Which definition matches up the three Elasticity of Supply? >when supply is very sensitive to price change. >when a percentage change in price is perfectly matched by an equal percentage change in QS >when supply is not responsive to price change. Unit Elastic Supply – Inelastic Supply – Elastic Supply ####################################################### *What determines whether the supply of a good will be elastic or inelastic? *In the Short Run, why would a firm be Inelastic? *In the Long Run, why would a firm be elastic? *What is the definition of Marginal Product? *What is the definition of Fixed Costs? *What is the definition of Variable Costs? *What are the four parts that make up the Fixed Costs for a producer? *What are the three parts that make up the Variable Costs for a producer? *What is the definition of Total Costs? What is the definition of Marginal Costs? *What is the definition of Marginal Revenue? *What is the definition of Total Revenue? *What formula does a company use to determine their Profit? *Which Stage of Production matches with the following descriptions? > total production keeps growing, but by smaller and smaller amounts. > too much input - total output decreases as input increases -MP is negative. > increasing returns as the number of workers increase they better use of their time, machinery, and resources. *What happens to Supply when a producer has a rise in the cost of an input? *What happens to Supply when a producer has *What five factors affect the movement of the Supply Curve? *What happens to the Supply Curve when the government places a tax on a product? *What is the definition of Inflation? Marginal Product Examples # or Workers 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Total 0 7 18 32 50 72 100 125 149 165 174 181 184 188 187 184 Marginal Product -7 Stage ---I Clayware’s Production Schedule # of Fixed Variable Total Bowls Cost Cost Cost Cost Revenue Revenue Profit 0 $22 $0 $22 ---- $0 $0 ($22) $5 $30 $30 ($3) 1 $5 2 $8 3 $10 4 $14 5 $19 6 $26 7 $36 8 $48 9 $65 10 $87 11 $100 *Sale of each Bowl is $ 30.00 Marginal Marginal Total