trendsinbanking-partii-150818173855-lva1-app6891

advertisement

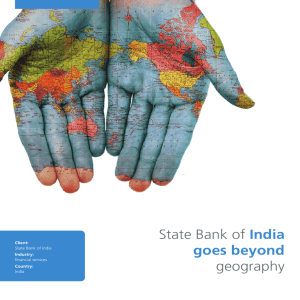

Trends in banking (Part-2) SBI to spend 4,000 Crores on Digital Services Upgrade SBI to go ‘Digital’ The country’s largest lender State Bank of India(SBI) has raised its Information Technology budget by a third this Financial Year as part of its strategy to improve its digital offerings SBI will spend nearly Rs.4000 Crores before March 2016 & significantly upgrade its IT back-end while also investing in new equipment for the “250 In Touch Lite Branches” SBI In Touch Lite branches will have devices for customers to help themselves while opening a new account, getting a new Debit Card, transferring/depositing money, planning for savings & applying for new loans According to Sunil Srivastava, Deputy MD(Corporate Strategy & New Business),about 69% of SBI’s Txns are done via, the Bank’s Alternative Channels like ATM, Internet & Mobile Banking SBI’s part of the Bank’s expenditure is going into setting-up the 385 Tech Learning Centers across the country which train customers in Mobile & Internet Txns every month While Mobile Banking operations are currently focused on retail customers, SBI intends to go a step further & launch Corporate Banking facilities through a Mobile Application called “Saral” According to Boston Consulting Group’s(BCG) September 2014 report, the IT spends of Indian Banks have been rising to touch nearly 4% of their revenue. However, most of this spending has been to buy self-service machines which is hardly enough for Public Sector Banks to hold their position The share of txns through alternative channels at SBI is lower than private sector peers such as HDFC Bank where about 85% of the txns happen through Non-branch channels with Mobile & Internet banking contributing about 55% of total txns according to June 10th 2015 report by Citi Research A financial service institution will always incur a very high cost in its technology spend because for 2 main reasons; •To adhere to the IT Security requirements as prescribed by the regulators(RBI/IDBRT) •To differentiate itself from its peers in terms of txn being given effect to accurately & instantaneously SBI has clarified that the emergence of alternative channels does not mean that the bank will reduce focus on traditional branches .The Bank will continue to manage & expand its 16,000 strong branch network to offer Banking Services to customers who may prefer face-to-face interaction in dealing with a Bank. As of 31 March 2015,SBI had 16,333 branches across India(an increase of 464 branches since the same period a year ago).The rate of expansion has slowed down considerably .For the year ended March 2014,SBI had added 1,053 new branches Digital as a Service In an interview last month, Aditya Puri, MD & CEO of HDFC Bank had noted that more than half the bank’s customer acquisition is likely to move to the digital side even as the other half may continue to prefer brick-and-mortar branches to open their accounts SBI is also expanding its network of Point-of-Sale(PoS)terminals to 1 million within next 3 years from about 2,20,000 such terminals currently as a way to encourage the use of Debit & Credit Card Txns To capture the increased preference for Mobile Txns private sector banks such as HDFC Bank, ICICI Bank, Axis Bank & Kotak Mahindra Bank have all launched Multiple Digital Payment Solutions including Mobile Applications & Payments through Social Media Applications SBI might have been slow in adopting technology when compared to other small organization but its ability to fund innovation in future is far higher than competition Digital as a Service Union Bank to open 100 Digital branches in 2015 Arun Tiwari,CMD(Union Bank of India) believes that digital will be among the top 3 differentiators with for the bank. He says transformation to a digital bank began with him when the bank had done away with the piles of files on his desk & replaced it with a tablet. Now worth a single click, he can keep tab of what is happening in a bank branch thousands of kilometers away. Union Bank of India is planning to launch 100 digital branches in 2015.The bank has a strong technology backend to take this project forward On the wallet front, Bank is looking at tying up with mobile wallet player-PayTm to allow its user to top-up their wallet from any Union Bank of India ATM’s. Currently, these top-up facilities are only available on Bank’s net banking & Debit/Credit Card gateways. Along with increasing offerings for customers on the digital front, bank is also looking at tying up with online retailer Flipkart to roll-out its M-POS solution for customers ordering their product through Cash on Delivery(CoD) Apart from Digital Branches, the bank will soon be launching NFC(Near Field Communication)enabled contactless Debit Cards. This facility allows customers to just tap their Debit Card on Pont-of-Sale terminals instead of swiping them. Other banks like ICICI,SBI & Axis Bank have already launched NFC Cards. The Bank also plans to launch Mobile Wallets that will allow customers to view their accounts online, transfer funds based on e-mail ID/Mobile Number, open SB Accounts online etc The Bank has already launched M-Passbook as initiative to go digital Union Bank of India is looking at the digital medium not only to provide more convenience to customers & reduce its cost but lso to provide additional security while transacting. Ex: The bank will soon be allowing customers to block/unblock their Debit/Credit Card on their own.Also customers can also set limits for Cash Withdrawals, POS & E-Commerce transactions on their own Currently,59% of the Union bank of India’s txns take place on digital platform. Till last year the number was around 63% but has come down due to increase in the total number of accounts opened under Pradhan Mantri Jan Dhan Yojana Scheme. According to RBI data for Union BankAt the end of April 2015 Rs.118 Crores were carried out on the mobile platform. In 2014 the number stood at Rs.26 Crores SBI has tied-up with the following online retailers; Snapdeal to roll out a capital assistance programme for sellers using the online retailers platform PayPal to help international trade Amazon.com-SBI has signed a memorandum of understanding to develop a payment solution for customers & sellers MakeMyTrip Digital medium brings costeffectiveness for a bank .A transaction at the brick-and-mortar branch costs anywhere between Rs.55-60 whereas transaction through online costs about Rs.15-17 & on mobile it is very less with just Rs.2-3 ICICI Bank has tie-up with Alibaba.com With this Indian entrepreneurs who are a part of the online portal will get a whole host of Banking facility from ICICI Bank According to PwC report, the e-commerce market in India will touch $22 billion by the end of 2015.With this in view banks are clearly seeing lending to small & medium enterprises in the online space as a growing opportunity Digital Effect RBI introduces New Category of Prepaid Payment Instruments for Mobility Cards The Prepaid Payment Instruments(PPI’s)will be issued by the mass transit operators(such as Metro/Road Transport) RBI has issued Draft guidelines on Mobility Cards that will allow people to travel without Cash in metros, buses & taxis The user of this card will not be allowed any cash-out facility or refund on the cards.RBI has not laid down any mandatory KYC norms for issuing such cards but has suggested that issuer can conduct KYC procedure on their own The main idea to launch these type of Cards is to gradually move towards a Cashless Economy. One such area where a large number of small value cash payments take place relate to mass transit system These prepaid Cards can also be used at other merchants as long as the activity is limited to transit. The cards have a minimum validity of 6 months from the date of issue. The maximum amount that can be loaded onto this card is Rs.2000.This is a re-loadable Card HDFC Bank has the highest Mobile Banking share (Report by BNP Paribas Securities India Pvt Ltd) HDFC Bank Ltd has emerged as the leader in mobile banking with 38.2% market share in FY15 followed by ICICI Bank Ltd(according to data compiled by BNP Paribas Securities India Pvt Ltd) With urban customers & those below 35 years of age clearly preferring mobile banking –market leaders like HDFC,ICICI stand a better chance of becoming their primary bank. Lenders who win the battle in this space will be able to bolster their low-cost base (like Savings Account & Current Account )& fees Most of the state-run banks which account for more than 70% of the banking assets in the country are clear laggards in this segment with just 17% share in total mobile transaction value BNP Paribas analyst points out a significant mismatch between the market share of savings account & mobile banking. For instance in FY15 even as SBI beats HDFC Bank with the savings account market share of 39.3% compared with the latter’s 9.5% but the mobile banking market share of HDFC Bank at 38.2% is much higher than SBI’s 12.9% Given the clear preference towards mobile banking the mismatch could result in potential loss in the market share of savings accounts for these banks sooner rather than lateraccording to the report. Also all government –run banks except SBI & Union Bank of India are yet to catch-up on the digital banking side –BNP Paribas said in its Digital Banking report Tamil Nadu, Kerala States lead surge in Financial Inclusion Five States/Union Territories drove a surge in India’s Financial Inclusion index which improved to 50.1(of a possible 100)at the end of 2013 As many as 45 of India’s top 50 districts that offer affordable, formal financial services are in 4 south Indian States with 30 in Tamil Nadu & Kerala-according to CRISIL Inclusix, a measure of financial inclusion The top 5 States/Union Territories are; (1)Puducherry (2)Kerala (3)Tamil Nadu (4)Goa (5)Chandigarh These States drove a surge in India’s Financial Inclusion index which improved to 50.1(of a possible 100)at the end of 2013 from 42.8 at the end of 2012 The index does not take into account the Prime Minister’s Jan Dhan Yojana (People’s Wealth Scheme).With over 149 million new bank accounts opened since August 2014-the index will likely be boosted further in 2015 Financial Inclusion is defined as “the extent of access by all sections of society to formal financial services such as credit, deposit, insurance & pension services (as defined by CRISIL-Mumbai based ratings agency) CRISIL’s Inclusix is a relative index that combines three parameters of basic financial services; -Branch Penetration -Deposit Penetration -Credit Penetration A score of 100 indicates the ideal state for each of the three parameters CRISIL has included District-Wise data from microfinance institutions(MFI’s)to calculate the index for the first time covering 653 districts in 35 States & Union Territories •As many as 117 million Savings Bank accounts were opened in the financial year 2013(almost 50% more than the 79 million that opened in the previous year).The total operative bank accounts in India at the end of 2013 were 820 million as against 703 million in 2012(an increase of 17%-the fastest growth in four years •Growth in credit accounts declined due to a reduction in small-borrower accounts to 102 million in 2013 from 109 million in 2012.The decline was primarily observed in 5 metro districts; Delhi Kolkata Mumbai Suburban Bangalore Urban South Leads; North-East at bottom but moves ahead With an increase of 40% in bank credit accounts, the northern state of Jammu & Kashmir saw its Inclusix score improve to 45.2.The State also saw High Deposit & Branch scores of 61.6 & 56.3 The limited presence of MFI’s in Micro-Finance Institutions(MFI’s) States like Uttar Pardesh, Bihar & Manipur leads to a low level of credit The presence of a large number availability for small borrowers of MFI’s including the largest The inclusix score of 50.1 shows that a 9 districts hit the Micro-finance Institution in India part of India’s population does maximum Inclusix score large ‘Bandhan Financial Services’ not have access to formal Financial of 100.All are from the Services but this is before taking into (that has already obtained account the boost from ‘Jan Dhan Banking license & soon be South. Yojana’ operational from October 2015) -Six districts are from Kerala Financial Inclusion will improve from saw West Bengal improve its State(Pathanamthitta,Alappuzha, various policy steps taken by the govt, Inclusix score to 46.6 Ernakulam,Kottayam,Thiruvanan one being ‘Pradhan Mantri Jan Dhan Yojana’ which has not been factored in The presence of MFI’s also saw thapuram,Thrissur) this edition of Inclusix.Under ‘Jan -Two are from Puducherry the North-East improve its State(Karaikal & Mahe) Dhan Yojana’ more than 140 Inclusix score to 39.7 -One district from Tamil million new Savings Bank Nadu(Coimbatore) Accounts have been opened . Of the 107 districts in South India,104 have an Inclusix score more than the all-India average Parameters & Measures used by CRISIL to Measure Financial Inclusion Parameters Branch Penetration Credit Penetration Measure No. Of. branches per lakh of population in a district Measures the ease with which people in a particular territory can access Financial Services No. Of loan accounts per lakh of a population in a district Measures the extent of access to ‘loan products’ offered in a particular territory No. Of small-borrower loan accounts as defined by RBI per lakh of population in a district (small borrowers are borrowers with a sanctioned credit limit of up to Rs.2 lakhs) No. Of agricultural advances per lakh of population in a district Deposit Penetration Significance No. Of Savings Bank Accounts per lakh of population in a district Measures access to credit for small borrowers who typically face Financial Non –Inclusion Measures farmer’s access to credit Measures the extent of access to Savings products offered by banks in a particular territory CRISIL Method of measurement Anup George Rebello Asst.Manager The Catholic Syrian Bank Ltd anuprebello.6@gmail.com http://www.slideshare.net/anuppresentations