Colonial First State Presentation Title

advertisement

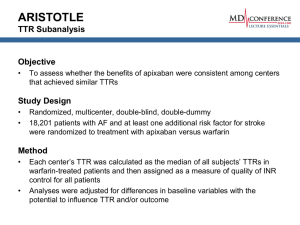

Transition to retirement strategy – everything you need to know Kim Guest: Senior Technical Manager - FirstTech July 2014 firsttech@colonialfirststate.com.au Disclaimer This presentation is given by a representative of Colonial First State Investments Limited AFS Licence 232468, ABN 98 002 348 352 (Colonial First State). Colonial First State Investments Limited ABN 98 002 348 352, AFS Licence 232468 (Colonial First State) is the issuer of interests in FirstChoice Personal Super, FirstChoice Wholesale Personal Super, FirstChoice Pension, FirstChoice Wholesale Pension and FirstChoice Employer Super from the Colonial First State FirstChoice Superannuation Trust ABN 26 458 298 557 and interests in the Rollover & Superannuation Fund and the Personal Pension Plan from the Colonial First State Rollover & Superannuation Fund ABN 88 854 638 840 and interests in the Colonial First State Pooled Superannuation Trust ABN 51 982 884 624. The presenter does not receive specific payments or commissions for any advice given in this presentation. The presenter, other employees and directors of Colonial First State receive salaries, bonuses and other benefits from it. Colonial First State receives fees for investments in its products. For further detail please read our Financial Services Guide (FSG) available at colonialfirststate.com.au or by contacting our Investor Service Centre on 13 13 36. All products are issued by Colonial First State Investments Limited. Product Disclosure Statements (PDSs) describing the products are available from Colonial First State. The relevant PDS should be considered before making a decision about any product. Stocks referred to in this presentation are not a recommendation of any securities. The information is taken from sources which are believed to be accurate but Colonial First State accepts no liability of any kind to any person who relies on the information contained in the presentation. This presentation is for adviser training purposes only and must not be made available to any client. This presentation cannot be used or copied in whole or part without our express written consent. © Colonial First State Investments Limited 2014. 2 What we’ll cover … • How tax effective is TTR? • TTR strategy Mythbusters • Excess contributions 3 Tax benefits of a TTR strategy TTR strategy has two main benefits: • Earnings Tax Benefit • No tax on earnings on assets supporting pension + • Personal Tax Benefit • • • 4 Tax saved by salary sacrifice increases this benefit Tax paid on TTR pension payments reduces this benefit Contributions tax and 15% pension offset also taken into account Tax savings on TTR strategy for clients aged 55-59 Personal income tax benefits for salary vs TTR Income - $100 before tax income Net $100 after tax MTR (%) Gross TTR Income 0.00 100.00 100 21.00 79.00 84.04 34.50 65.50 39.00 47.00 Net tax on TTR Net TTR Income Total Tax Payable Effective Tax Savings* 100.00 15.00 5.04 79.00 15.00 20.04 0.96 81.37 15.87 65.50 15.00 30.87 3.63 61.00 80.26 19.26 61.00 15.00 34.26 4.74 53.00 77.94 24.94 53.00 15.00 39.94 7.06 This is ignoring the earnings tax benefit *5Tax savings reflected in higher super account balance -15.00 Cont Tax payable 0 0 Tax savings on TTR strategy for clients aged 60 or over Personal income tax benefits for salary vs TTR Income - $100 before tax income MTR (%) Net $100 after tax Gross TTR Income Net tax on TTR Net TTR Income Cont Tax payable Total Tax Payable Effective Tax Savings* 21.00 79.00 79.00 0 79.00 15.00 15.00 6.00 34.50 65.50 65.50 0 65.50 15.00 15.00 19.50 39.00 61.00 61.00 0 61.00 15.00 15.00 24.00 47.00 53.00 53.00 0 53.00 15.00 15.00 32.00 This is ignoring the earnings tax benefit *6Tax savings reflected in higher super account balance How tax effective is a TTR strategy? • Jane earns $60,000 salary and has a super balance of $200,000 • Justin earns $80,000 salary and has a super balance of $350,000 • Jasmine earns $100,000 salary and has a super balance of $500,000 Let’s look at TTR strategies, specifically: • Impact of $35,000 CC from last July assuming clients are aged 60… • Impact of $35,000 CC from this July assuming clients are aged 55… 7 Clients aged 55, benefit of TTR for one year $4,500 $4,146 $4,000 $3,601 $3,773 $3,500 $3,000 $2,500 $2,625 $2,156 $2,156 $2,000 $1,500 $1,000 Sal.$60,000 Sal.$80,000 Sal.$100,000 $500 $0 Jane 8 Justin $25,000 concessional cap $35,000 concessional cap Jasmine Clients aged 60, benefit of TTR for one year $10,000 $9,051 $9,000 $8,000 $7,450 $7,000 $6,701 $6,468 $6,000 $5,000 $4,257 $4,257 $4,000 $3,000 $2,000 Sal.$60,000 Sal.$80,000 Sal.$100,000 $1,000 $0 Jane 9 Justin $25,000 concessional cap $35,000 concessional cap Jasmine Long term impact of a TTR strategy- Judy case study 55 years old, works full time and has no plans to change employers Income $50,000 gross pa ($41,453 pa net) Judy $300,000 accumulated in super Aims to retire at 65 Objective: Judy wants to keep working and at the same time increase her retirement savings in super 10 Long term impact of TTR strategy- Judy case study Without a TTR strategy Using a TTR strategy $50,000 $50,000 Salary sacrifice n/a ($14,813) Pension payment n/a $12,000 Tax paid ($8,547) ($5,735) After-tax income $41,453 $41,453 $495,416 $540,850 $24,770 $27,040 Salary At age 65 Retirement balance Minimum pension Assumptions: earning 7.7% pa after fees and before taxes with inflation at 3%; using 2014-15 income tax rates; minimum pension is paid as an allocated pension; superannuation guarantee contributions are 9.50% of gross salary before any salary sacrifice in year 1, rising gradually to 12% in year 7; all superannuation contributions and pension payments are made regularly throughout the year. This also assumes the low income tax offset applies. A change to any of the assumptions and variables can provide significantly different results. 11 1. This applies whilst the TTR is in existence. Transition to Retirement strategy Myth 1 When a TTR pension commences part way through the year, the 10% maximum pension drawdown must be pro-rata based on the number of days remaining in the financial year. There’s no requirement to pro-rata the 10% maximum pension payment if the pension’s commenced part way through the year. i.e. TTR pension commenced on 1 March 2014 for $500,000 the member can withdraw $50,000 before 30 June 2014. 13 Myth 2 Under no circumstances can lump sum commutations be taken from a transition to retirement pension . Unrestricted Non-Preserved can be accessed if trustees are able to keep track of it. However, be mindful that pension payments are deemed to come out of the URNP component first. Some super funds preserve all benefits 14 Myth 3 TTR strategy is not worthwhile if earn less than $37,000 pa Case study: Ron is aged 55 and has approximately $250,000 in superannuation (all taxable component). He works part time and has a salary of $25,000 pa while his wife Lucy earns $70,000 pa. Ron plans to retire in 5 years time. Should Ron implement a TTR strategy, draw the minimum payment and direct any surplus income to his superannuation account as a non-concessional contribution? 15 Ron Myth 3: TTR strategy worthwhile if earning less than $37,000? Retirement savings balance $320,000 Year 3 $4,811 $300,000 Year 2 $3,122 $280,000 Year 1 $1,520 $260,000 no ttr Year 5 $8,472 $240,000 $220,000 Year 4 $6,592 $200,000 55 56 57 58 Age 1 Assumptions: amounts shown in today’s dollars; income and realised gains of 4.63% and capital growth of 2.31%; franking percentage of 22.2%. Tax rates and thresholds for 2014/15 financial year; includes government co-contribution; 16 59 ttr Myth 4 When implementing a TTR strategy a client should always convert 100% of their super balance to a TTR pension. 17 For clients over 60 – yes move it all to pension phase! Case study: Betty • Aged 60 and working full time, earning $150,000 pa • Concessional cap $35,000, SG $13,875, – $21,125 remaining for salary sacrifice under TTR strategy • Current super balance $600,000 $150,000 TTR $300,000 TTR $450,000 TTR $600,000 TTR Min TTR pension $6,000 $12,000 $18,000 $24,000 Salary sacrifice $9,756 $19,512 $21,125 $21,125 Non-concessional - - $5,008 $11,008 Net contribution $8,293 $16,585 $22,964 $28,964 Personal Tax Benefit $2,293 $4,585 $4,964 $4,964 Earnings Tax Benefit* $900 $1,800 $2,700 $3,600 Total benefit of TTR strategy $3,193 $6,385 $7,664 $8,564 18 Assumes 4% pa income, taxed at 15% in accumulation phase or tax free in pension phase For clients between preservation age and 59, not so easy! Case study: Chris • Aged 55 and working full time, earning $150,000 pa • Concessional cap $35,000, SG $13,875, – $21,125 remaining for salary sacrifice under TTR strategy • Current super balance $600,000 $150,000 TTR $300,000 TTR $450,000 TTR $600,000 Min TTR pension $6,000 $12,000 $18,000 $24,000 Salary sacrifice $7,475 $14,951 $21,125 $21,125 Non-concessional - - $794 $5,354 Net contribution $6,354 $12,708 $18,750 $23,310 Personal Tax Benefit $354 $708 Earnings Tax Benefit* $900 Total benefit of TTR strategy $1,254 19 $750 - $690 $1,800 $2,700 $3,600 $2,508 $3,450 $2,910 * Assumes 4% pa income, taxed at 15% in accumulation phase or tax free in pension phase Clients 55 to 59, how personal tax benefit changes… Tax saved from salary sacrifice Concessional cap Extra tax on pension payments Personal Tax Benefit is maximised when minimum pension payment is only just enough to allow a client to use their concessional cap. 20 Chris’s Personal Tax Benefit peaks when TTR is $425,000 $4,000 $3,500 $3,000 $2,500 But won’t the increasing Earnings Tax Benefit more than make up for this reducing benefit? $2,000 $1,500 $1,000 $500 $0 -$500 -$1,000 $600,000 Chris's Personal Tax Benefit $500,000 21 $400,000 $300,000 $200,000 $100,000 $0 TTR pension starting balance Earnings tax benefit v Personal Tax Benefit Effect of increasing TTR starting pension balance by $25* MTR Personal Tax Benefit lost Earnings tax benefit gained Outcome 21% 6 cents 15 cents 9 cents better off 34.5% 19.5 cents 15 cents 4.5 cents worse off 39% 24 cents 15 cents 9 cents worse off 47% 32 cents 15 cents 17 cents worse off 22 * 2014-15 MTRs including 2% Medicare levy, 100% taxable component, earning rate is 8% pa consisting of half income and half unrealised gain Chris’s optimum TTR is where Personal Tax Benefit peaks $4,000 $3,500 $3,000 $2,500 $2,000 $1,500 $1,000 $500 $0 -$500 -$1,000 23 Chris's Earnings Tax Beneift Chris's Personal Tax Benefit Total benefit of TTR $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $0 TTR pension starting balance 24 Salary $35,000 concessional cap $250,000 $240,000 $230,000 $220,000 $210,000 $200,000 $190,000 $180,000 $170,000 $160,000 $150,000 $140,000 $130,000 $120,000 $110,000 $100,000 $90,000 $80,000 $70,000 $60,000 $50,000 $40,000 $30,000 Ideal maximum TTR starting balance Optimum TTR balance for employee clients aged 55 to 59 $800,000 $700,000 $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $0 Myth 5 It is not worthwhile for people earning over $300,000 to implement a TTR strategy. Background: From 1 July 2012 clients who earn over $300,000 will pay an additional 15% tax on any non-excessive concessional contributions. • Clients earning over $300,000 likely to have already maxed out their CC cap • Clients aged 55-60: benefit of a TTR strategy is likely to be marginal • Clients aged 60 or over: still worthwhile because of savings on earnings tax in pension phase 25 TTR strategy summary • Extending $35,000 cap to clients age 55-59: – existing 55-59 yo clients may need existing TTR strategy adjustments • Clients aged 60 or over, always best to use as much super as possible to commence TTR – Some exceptions, eg, already maximising NCC, in untaxed fund, etc. • Clients aged 55 to 59, a maximum optimum balance will apply – Make most use of concessional contribution cap unless on low income – Salary sacrifice so that taxable income is no less than $20,542 – If the client’s super balance is substantial and the minimum pension balance exceeds the income requirement, then consider optimum pension balance – Refreshing to optimum balance each year may maximise benefit – Also recommence with 100% of super balance at age 60 26 Excess contributions Excess concessional contribution tax changes • Substantial changes to old system • Excess CCs included in assessable income – taxed at marginal rate plus excess contributions tax charge • Entitled to tax rebate of 15% of excess concessional contributions • applies regardless of effective tax rate on contributions 28 Excess concessional contribution tax changes • Can elect to have up to 85% of excess contributions released • Must apply to ATO within 21 days of receiving excess notice • Once made election irrevocable • Payment to ATO who will then pay member (net of any outstanding liabilities) • Payment is non-assessable non-exempt income • Proportioning rules don’t apply • Reduces non-concessional contributions (amount x 0.85) 29 Case Study • Jessie (age 50) has assessable income of $100,000 in 2013-14 year • In the same year her concessional contributions totalled $35,000 ($10,000 excess) • Tax on excess concessional contributions calculated as follows: • amended assessable income = $110,000 • additional tax liability: $10,000 x 38.5% = $3,850 • less 15% of excess CCs: $3,850 – ($10,000 x 15%) = $2,350 • could elect to have up to $8,500 released • What if fund neutrally geared? • same result (15% rebate based on amount of excess CCs) 30 Excess concessional contribution tax changes • Should clients release their excess contributions? • do they need the money • do they have an excess non-concessional tax liability? • could pull out and put back in as non-concessional 31 Excess concessional contribution tax changes • Additional charges apply to adjust for timing difference • excess contributions charge • shortfall interest charge • Excess contributions charge • payable on the amount of an individual’s income tax liability attributable to the taxpayer’s excess concessional contributions in a year • applies from first day of the year to which the contributions relate to day before tax is payable under first assessment • 90 day bank accepted bill rate + 3% (currently 5.69%) • not deductible expense 32 Excess concessional contribution tax changes • Shortfall interest charge • payable on difference between original tax liability and amended assessment taking into account excess concessional contributions • applies from time original tax liability due until time additional liability paid • same rate as excess contributions tax charge (currently 5.69%) 33 Excess concessional contributions tax changes Example Assuming same details for Jessie (tax on excess CCs of $2,350) 1 July 2013 30 June 2014 Lodges tax return 31 August 2014 21 September 2014 Tax assessment for 2013-14 issued Total tax liability on excess contributions = $2,547 34 Commonwealth Bank of Australia / Presentation Title / Confidential 30 November 21 December 2014 2014 Amended assessment for 2013-14 issued Additional tax paid Thank You FirstTech team: 13 18 36 Email: firsttech@colonialfirststate.com.au