The Market System

advertisement

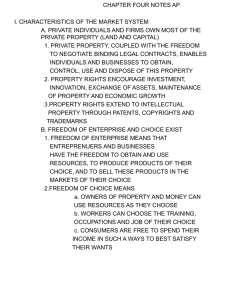

The Market System 1. Private individuals and organizations own and control their property resources by means of private property. – – – PP, coupled with the freedom to negotiate contracts, enables individuals/firms to obtain, control, use and dispose of property PP rights encourage investment, innovation, exchange of assets, maintenance of property and economic growth PR extend to intellectual property through patents, copyrights, and trademarks. 2. Freedom of Enterprise and choice exists. Freedom of enterprise • Entrepreneurs and businesses have the freedom to obtain and use resources, to produce products of their choice, and to sell these products in the markets of their choice Freedom of choice • Owners of property and money resources can use resources as they choose. • Workers (labor), can choose the training, occupations, and job of their choice. • Consumers free to spend their income in such a way as to best satisfy their wants (consumer sovereignty) 3. Self-Interest • One of the driving forces in a market system. Entrepreneurs try to maximize profits/minimize losses; resource suppliers try to maximize income; consumers maximize satisfaction • As each tries to maximize profits, income, satisfaction the economy will benefit if competition is present. 4. Competition among buyers/sellers is a controlling mechanism • Large #s of sellers mean that no single producer/seller can control the price or market supply • Same for buyers (consumers, employers) • Ease of entry/exit for producers 5. Markets and Prices • • • A market system conveys the decisions of the many buyers and sellers of the product and resource market. A change in the market price signals that a change in the market has occurred. Those who respond to the market signals will be rewarded with profits and income. 6. Active but limited government. • Although the market system promotes efficiency, it has certain shortcomings. • Later referred to as market failures. • Looked at closer in chp 5 In common with the other advanced economies of the world, the U.S. has three major characteristics. 7. Reliance on technology and capital goods • Competition, freedom of choice, selfinterest, and the potential of profits provide the incentive for capital accumulation (investment). • Advanced technology and capital goods uses the more efficient roundabout method of technology. 8. Specialization • Division of labor allows workers to specialize – Makes use of differences in abilities and skills – identical skill sets can still benefit from specialization – saves time (set up costs) • Geographic specialization • regional/international specialization take advantage of localized resources 9. Use of money as a medium of exchange. • Money substitutes for barter – coincidence of wants Market System at Work • Self-Interest • Brings consumers and producers together in an efficient manner • 4 questions that must be addressed by every economic system (Key) 4 QUESTIONS 1. What goods and services to be produced? 2. How will these goods and services be produced? 3. Who will get these goods and services? 4. How will the system accommodate change? The price system, including markets and households’ and business firms choices furnish the economy with answers to theses questions. 1. In order to be profitable, businesses must respond to consumers’ wants/desires. 2. When businesses allocate resources in a way that is responsive, they will be profitable leading to allocative efficiency. Must know! • Economic Profit = total revenue (TR) – total cost (TC) • TR = Product price x quantity of product sold • TC = The sum of the (price of each resource used by the amount employed) • Economic costs include the return to the entrepreneur. This return must be received if the entrepreneur is to continue. continued The payment for the entrepreneur’s contribution is called normal profit. If the TR exceeds of these economic costs the gravy goes to the entrepreneur and is called economic profit. 2. Self-regulating nature of the market place • Expanding industries • Declining industries • Remind me to diagram How? • Least cost method • Lc production techniques include: locating firms in the optimum location considering resource prices, resource productivity, and transportation costs, available technology and resource prices in general • production of a given amount of output with the smallest input of scarce resources, measured in $s and ¢s. Whooooooo? • Directly related to distribution of income of households and individuals, tastes/preferences • products go to those who are willing and able to pay for them • productivity of the resources,, relative supply of and ownership of will determine the income of individuals and households • The resource (factor) markets, which determine income, are closely linked to this decision Change • An ↑ in D for some products will lead to higher prices in those markets • A↓ in D for other products will lead to lower prices in those markets • ↑ D leads to higher prices that induce > Qs of output. The opposite is true for a ↓ in D. • Higher prices lead to more profits & new firms entering the market • Lower prices lead to losses & firms leaving the industry The market system promotes technological improvements & capital accumulation • An entrepreneur/firm that introduces a popular new product will be rewarded with ↑ revenue and profits. (Topline.bottomline) • New technologies that reduce production costs and thus price will spread throughout the industry as a result of competition • Creative destruction occurs when new products/production methods destroy the market positions of firms that can’t or won’t adjust. Competition & the “Invisible hand” • Competition is the mechanism of control for the market system. Consumer gets what they want, firms must adopt the most efficient production techniques. • “Invisible Hand” promotes public interest through a market system where the primary motivation is self-interest. by attempting to maximize profits, firms will also be producing the g/s most wanted by society.