Chapter 1

advertisement

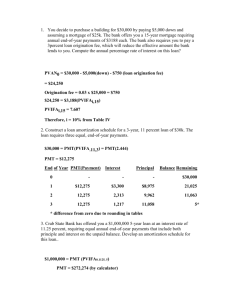

Chapter 6 Residential Financial Analysis 1 Overview Incremental Borrowing Cost Loan Refinancing Effective Cost of Multiple Loans Below Market Financing Cash Equivalency 2 Incremental Borrowing Cost Compare financing alternatives What is the real cost of borrowing more money at a higher interest rate? Alternatively, what is the required return to justify a lower down payment? Basic principle when comparing choices: What are the cash flow differences? 3 Incremental Borrowing Cost – Continued Example: Home Value = $150,000 Two Financing Alternatives: #1: 90% Loan-to-Value, 8.5% Interest Rate, 30 Years #2: 80% Loan-to-Value, 8.0% Interest Rate, 30 Years It appears there is only a 50bp interest rate difference, but… 4 Incremental Borrowing Cost – Continued House Value Loan-to-Value Ratio Loan Amount Interest Rate Loan Term Payment per Year Number of Payments Alternative 1 Alternative 2 $100,000.00 $100,000.00 80% 90% $80,000.00 $90,000.00 12.00% 13.00% 25 25 12 12 300 300 Monthly Payments $842.58 $1,015.05 Additional Borrowing $10,000.00 Additional Payment $172.47 What is the cost of additional amount borrowed? N I/Y P/Y PV PMT 300 12 -10,000 172.47 20.57% FV 0 5 Incremental Borrowing Cost – Continued 20.57% represents the real cost of borrowing the extra $10,000 Can you earn an equivalent risk adjusted return on the $10,000 that is not invested in the home? Alternatively, can you borrow the additional $10,000 elsewhere at a lower cost? 6 Incremental Borrowing Cost – Early Repayment Loan Costs with Prepayment in 5 Years Loan Balance Alternative 1: N I/Y P/Y PV 240 12.00% 12 -76,523 Loan Balance Alternative 2: N I/Y P/Y 240 13.00% 12 PV -86,640 What is the cost of additional amount borrowed? N I/Y P/Y PV 60 12 -10,000 20.83% PMT 842.58 FV 0 PMT 1,015.05 FV 0 PMT 172.47 FV 10,117 7 Incremental Borrowing Cost – Origination Fees Loan Costs with Origination Fees Points Loan Amount Additional Borrowing Additional Payment Alternative 1 Alternative 2 2% 3% $78,400.00 $87,300.00 $8,900.00 $172.47 What is the cost of additional amount borrowed? N I/Y P/Y PV 300 PV -8,900 23.18% PMT 172.47 FV 0 8 Incremental Borrowing Cost – Second Mortgage In the first case we compared 80 and 90% LTV loans By borrowing $90,000, cost of additional $10,000 was 20.57% What if we borrow $80,000 (80% LTV) and shop for loan for $10,000 with 25 year term If we can borrow that $10,000 at a cost less than 20.57% then we would have loan with a lower cost than 90% LTV loan. Suppose a lender can loan us that $10,000 at 18% Composite cost of borrowing would be ($80,000 / $90,000) × 12% + ($10,000 / $90,000) × 18% This is 12.66% It is clear that break-even rate for second mortgage is 20.57% 9 Incremental Borrowing Cost – Maturity Differences House Value Loan-to-Value Ratio Loan Amount Interest Rate Loan Term Payment per Year Number of Payments Alternative 1 Alternative 2 $100,000.00 $100,000.00 80% 90% $80,000.00 $90,000.00 12.00% 13.00% 25 30 12 12 300 360 Monthly Payments Additional Borrowing Additional Payment (First 300 Months) Additional Payment (Last 60 Months) $842.58 $995.58 $10,000.00 $153.00 $995.58 What is the cost of additional amount borrowed? CF0 = -10,000.00 C01 = 153.00 F01 = 300 C02 = 995.58 F02 = 60 CPT IRR 1.572 % Annual 18.86 % 10 Loan Refinancing Borrower consideration Lower interest rates in the market than on the current loan The borrower can secure lower monthly payments There is a cost to refinance Application of basic capital budgeting investment decision: What is our return on an investment in a new loan? 11 Loan Refinancing for Remaining Term of Original Loan 300 P/Y 12 PV -80,000.00 PMT 1,011.56 FV 0 Loan balance after 5 years: N I/Y 300 15.00% P/Y 12 PV -78,976.50 PMT 1,011.56 FV 0 PMT of the new loan: N I/Y 300 14.00% P/Y 12 PV -78,976.50 PMT 950.69 FV 0 Prepayment penalty $1,579.53 Financing costs $2,525.00 Cost of new loan $4,104.53 N I/Y P/Y PV PMT FV 300 12 -4,104.53 60.87 0 17.57% It appears that 4,104.53 committed to refinancing earns 17.57% annual return over 25 years. Unless you can earn more than that with similar risk you should refinance. F01 = PMT of the old loan: N I/Y 360 15.00% Last Computation with CF: -4,104.53 CF0 = C01 = 60.87 1.4640 % CPT IRR 17.57 % Annual Loan amount Loan rate Term (years) Prepayment penalty Financing costs Five Years Original Loan Later $80,000.00 15.00% 14.00% 30 25 2% $2,525.00 12 PMT 1,011.56 FV 0 Old loan balance after 15 years: N I/Y P/Y 180 15.00% 12 PV -72,275.26 PMT 1,011.56 FV 0 PMT of the new loan: N I/Y 300 14.00% PV -78,976.50 PMT 950.69 FV 0 P/Y 12 New loan balance after 10 years: N I/Y P/Y PMT FV PV 180 14.00% 12 950.69 0 -71,386.86 No prepayment penalty and financing costs at that time for the new loan. N P/Y PV I/Y 120 12 -4,104.53 14.21% Return on funds committed to refinancing. PMT 60.87 FV 888.40 Last Computation with CF: -4,104.53 CF0 = F01 = C01 = 60.87 F01 = C02 = 949.27 1.1843 % CPT IRR 14.21 % Annual Alternatives: 1. Keep the old loan for 10 more years 2. Refinance now and keep it for 10 years PMT of the old loan: N I/Y P/Y PV 360 15.00% 12 -80,000.00 119 1 Loan Refinancing – Early Repayment of New Loan 13 P/Y 12 PV -80,000.00 PMT 1,011.56 FV 0 Old loan balance after 15 years: N I/Y P/Y 300 15.00% 12 PV -78,976.50 PMT 1,011.56 FV 0 PMT of the new loan rolling financing cost: N I/Y P/Y PV 300 14.00% 12 -83,081.03 PMT 1,000.10 FV 0 PMT 1,000.10 FV 0.00 Effective cost: N P/Y PV I/Y 300 12 -78,976.50 14.81% Return on funds committed to refinancing. Last Computation with CF: -78,976.50 CF0 = F01 = C01 = 1,000.10 1.2344 % CPT IRR 14.81 % Annual PMT of the old loan: N I/Y 360 15.00% 300 Borrowing the Financing Costs 14 Effective Cost of Multiple Loans Basic Technique Compute the payments for the loans Combine into a cash flow stream Compute the effective cost of the amount borrowed, given the cash flow stream Compare the cost to alternative financing options 15 Effective Cost of Multiple Loans – Continued Example: You need a $500,000 financing package. $100,000 at 7.0%, 30 Years $200,000 at 7.5%, 20 Years $200,000 at 8.0%, 10 Years 16 Effective Cost of Multiple Loans – Continued Loan 1 Payment: N I/Y 360 7.00% Loan 2 Payment: N I/Y 240 7.50% Loan 3 Payment: N I/Y 120 8.00% P/Y 12 PV -100,000.00 PMT 665.30 FV 0 P/Y 12 PV -200,000.00 PMT 1,611.19 FV 0 P/Y 12 PV -200,000.00 PMT 2,426.55 FV 0 CF0 = -500,000.00 C01 = 4,703.04 F01 = C02 = 2,276.49 F02 = C03 = 665.30 F03 = CPT IRR 0.6239 % Annual 7.49 % 120 120 120 17 Below Market Financing A seller with a below market rate assumable loan may increase the home price All else equal, a buyer is paying a higher price for lower payments Similar to other problems, we compute interest rate and compare it to other equivalent risk investments 18 Below Market Financing – Continued Price Loan Balance Loan Characteristics Down payment I Term (Years) Payments per Year Payment A B $105,000 $100,000 $70,000 $70,000 Assumable New Loan $35,000 $30,000 9% 11% 15 15 12 12 $709.99 $795.62 Return on investment: CF0 = -5,000.00 C01 = 85.63 F01 = CPT IRR 1.6172 % Annual 19.41 % 180 The buyer can secure below market financing by paying $5,000 more for an identical home The below market financing results in a monthly payment of $85.63 less than if regular financing was used The buyer earns 19.41% on the $5,000 investment by reducing the monthly payment by $85.63 19 Cash Equivalency How much more a borrower would be most willing to pay for a property with an assumable loan? This is same as PV of payment savings discounted at the rate a new loan could be obtained CF0 = C01 = I= CPT NPV 0.00 85.63 11% 7,534.00 F01 = 180 20 Cash Equivalency – Continued Together with the financing premium, a buyer could be willing to pay $107,534 for this property to receive the benefit of below-market financing Does this mean the house is worth more than $100,000? Need to separate the value of the property with and without the effects of financing Note that the amount of cash invested in this property would be $100,000 if you take away the assumable loan benefit 21 Cash Equivalency - Smaller Loan Balance Price Loan Balance Loan Characteristics Down payment I Term (Years) Payments per Year Payment CF0 = C01 = I= CPT NPV 0.00 22.14 11% 1,947.59 A1 A2 $105,000 $50,000 $20,000 Assumable New Loan $30,000 9% 14% 15 15 12 12 $507.13 $266.35 F01 = Total $773.48 B $100,000 $70,000 New Loan $30,000 11% 15 12 $795.62 180 Need for additional borrowing due to relatively low balance on the assumable loan reduces the financing premium on the property 22