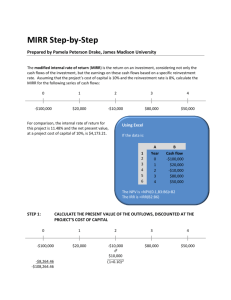

LO6

Appendix A – The Modified Internal

Rate of Return

• The MIRR is used on projects with nonconventional cash flows

• The cash flows are modified first and then

the IRR is calculated using the modified

cash flows

• There are three MIRR methods that are

used:

• The Discounting Approach

• The Reinvestment Approach

• The Combination Approach

© 2013 McGraw-Hill Ryerson Limited

9-0

LO6

MIRR Method #1

The Discounting Approach

• All negative cash

flows are discounted

back to the present at

the required return

and added to the

initial cost.

• From the previous

non-conventional

cash flow example,

we had a required

return of 15% and:

Year 0

-$90,000

Year 1

$132,000

Year 2

$100,000

Year 3

-$150,000

© 2013 McGraw-Hill Ryerson Limited

9-1

LO6

MIRR Example - Continued

• Using Method #1, the cash flow at year 3

would be discounted back to year 0 at 15%

• The cash flows would look like this:

Year 0: -$90,000 - $150,000/(1.153)

= -$188,627.43

Year 1: $132,000

Year 2: $100,000

Year 3: $0

• MIRR using Method #1 is 15.77%

© 2013 McGraw-Hill Ryerson Limited

9-2

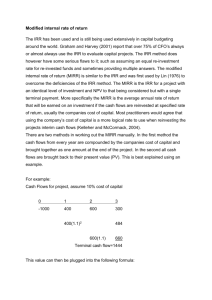

LO6

MIRR Method #2

The Reinvestment Approach

• All cash flows (positive and negative) except the

first are compounded out to the end of the

project’s life and then the IRR is calculated

• The cash flows would look like this:

Year 0: -$90,000

Year 1: $0

Year 2: $0

Year 3: $-$150,000 + $100,000(1.15) +

$132,000(1.152)

• MIRR using Method #2 is 15.75%

© 2013 McGraw-Hill Ryerson Limited

9-3

LO6

MIRR Method #3

The Combination Approach

• All negative cash flows are discounted back to

the present and all positive cash flows are

compounded out to the end of the project’s life

• The cash flows would look like this:

Year 0: -$90,000 - $150,000/(1.153)

= -$188,627.43

Year 1: $0

Year 2: $0

Year 3: $100,000(1.15) + $132,000(1.152)

= $289,570

• MIRR using Method #2 is 15.36%

© 2013 McGraw-Hill Ryerson Limited

9-4

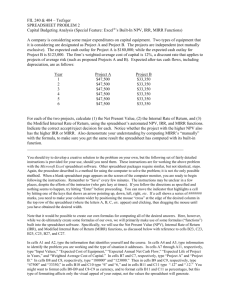

LO6

MIRR vs. IRR

• MIRR can handle non-conventional cash flows,

where as the IRR can’t

• But there are problems with MIRR:

• There are three methods, and three different MIRRs.

Which MIRR is correct? The differences could be

larger on a more complex project

• MIRR is a rate of return on a modified set of cash

flows, not the project’s actual cash flows

• Since the MIRR depends on an externally supplied

discount rate, the result is not truly an “internal” rate of

return

© 2013 McGraw-Hill Ryerson Limited

9-5

0

0