RESPONSIBLE FINANCE: OPPORTUNITIES IN THE MSME SECTOR

advertisement

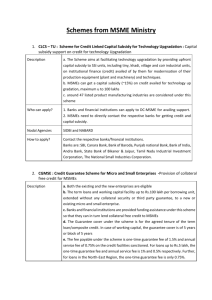

RESPONSIBLE FINANCE: OPPORTUNITIES IN THE MSME SECTOR Responsible Enterprise Finance Project GIZ May 2014 What is Responsible Finance? • As India moves towards propelling its economy back on course, it is important to acknowledge the role of the financial sector. • The importance of environment, society, governance and transparency (ESG) as determinants of sustainable growth cannot be over emphasized either. • These factors also become immediately relevant for financial institutions as they become directly or indirectly involved in financing projects, and can have influence across sectors, industries and communities. Responsible Finance Why is Responsible Finance important for MSMEs? Big Companies Individual impact and contribution to the economy Contributes to 45 per cent of the industrial output, 40 per cent of exports MSMEs Provides employment to more than 60 million people and creates as many as 10 lakh jobs each year. Produces more than 8,000 different products annually Some relevant developments • Regulatory landscape • Development organisations/ DFIs The regulatory landscape RBI Nachiket Mor Committee’s Vision Statements Business Responsibility Reports • Sufficient Access to Affordable Formal Credit • Universal Access to a Range of Deposit and Investment Products at Reasonable Charges • Universal Access to a Range of Insurance and Risk Management Products at Reasonable Charges • Right to Suitability • In 2012, SEBI mandated the reporting of performance of the top 100 listed companies on the National Voluntary Guidelines in the form of Annual Business Responsibility Reports • The BRRs contain information not only about the company’s own performance, but also that of their supply chain which typically consist of MSMEs SEBI Alternative Investment Fund Regulations • Released in 2012, SEBI details the definition of AIFs in India: • Any fund established or incorporated in India in the form of a trust or a company or a limited liability partnership or a body corporate which is a privately pooled investment vehicle which collects funds from investors, whether Indian or foreign, for investing it in accordance with a defined investment policy for the benefit of its investors DFIs| Energy-efficiency Financing With the establishment of the Bureau of Energy Efficiency in 2002, the Indian Government took the initiative to promote Energy Efficiency within the Indian economy. Efforts towards promoting Energy Efficiency among MSMEs are still at a nascent stage. The following are a few lines of credit: Examples of lines of credit: • Since 2009, SIDBI has been running focused lending schemes through a dedicated “Energy Efficiency Cell” under bilateral lines of credit from KfW, JICA, AfD and the World Bank. So far, at least 6,000 MSMEs have benefitted from Rs.3,000 crore (€422 million) in loans dedicated for investments in clean production and energy efficient technologies. • State Bank of India, the country’s largest bank, has developed an energy efficiency credit product with the support of GIZ and SIDBI. It is likely to be rolled out soon across all bank branches and has the potential of reaching some 6 million MSMEs. DFIs| Impact Investments In India, over 100 impact investments worth Rs.2,100 crore (€395 million) have been made so far in funding to innovative enterprises serving the needs of the poor and providing solutions in sectors such as education, sustainable agriculture and health. Examples of lines of credit: • The Samridhi Fund, operated by SIDBI with investments from DfID, will make impact investments of Rs.336 crore (€47 million) in social enterprises operating in India’s low-income states. • The India Opportunities Fund, managed by SIDBI on behalf of the Indian government, is the first in a series of funds that will provide Rs.5,000 crore (€703 million) in capital to innovative MSMEs over a ten year period. Focus on sectors such as: • Health • Education • Water and Sanitation • Rural Development • Women Empowerment Innovative Debt-Finance IFMR Capital: • Provides low cost refinance to local financial institutions so that they can in turn serve microenterprises – very similar to the role a District Credit Cooperative Bank may play in the life of Primary Agricultural Credit Society. Specialised Venture Debt Funds: • These include Intellegrow (http://intellegrow.com) and Caspian (http://www.caspian.in) that provide debt funds to Small Enterprises though perhaps not to microenterprises per se. Local Full-Service Financial Institutions: Specialised SME lenders: • These include Cooperative Banks, Regional Rural Banks, and the Kshetriya Gramin Financial Services (KGFS) companies promoted by IFMR Trust. These institutions have the capacity to fund a mix of micro and small enterprises in both rural and urban areas. • These include non-bank companies like Vistaar Finance (www.vistaarlfi.com) and AU Finance (www.aufin.in) who have developed specialised approaches to assess small enterprise cashflows and manage collateral. GIZ | The Responsible Enterprise Finance Project GIZ and SIDBI have come together under the Responsible Enterprise Finance Project to explore activities and make strategic interventions under the following four buckets: • Environmental and Social Risk Management Framework in MSME Financing • Innovative Products and Services for Energy Efficiency Financing • Risk Capital for Social Enterprises that target underserved markets • Voluntary Principles and Self-Regulation for the financial sector Environmental and Social Risk Management Framework in MSME Financing Financial sector side • The Project aims to: – Create a standardised ESG risk management framework for financial institutions to measure risk before financing MSMEs – Build capacities of credit- risk officers of FIs – Open dialogue with regulators for some development of regulation in this regard MSME side • Need for MSMEs to start taking their environmental, social and governance (ESG) impacts into account • Challenges: – General low adoption of regulatory requirements by MSMEs – Often, day-to-day survival struggles tend to put ESG concerns secondary Innovative Products and Services for Energy Efficiency Financing (EEF) Financial Sector Side • The Project aims to: – Develop and pilot some innovative financial products to promote and incentivise energy efficiency in MSMEs – Have FIs recognise EEF as a new stream of revenue and a distinct product • Challenges: – Lack of refinancing makes smallscale banks more risk-averse. – Some banks face difficulty in coping with general loan demand from MSMES but don’t anticipate demand from EEF products MSME Side • MSMEs need to recognise the long-term benefits of and business case for energy efficiency • Challenges: – Lack of knowledge amongst MSMEs regarding measurements like NPV, etc. – Lack of demand for financial products from the MSME side – Lack of domain experts who understand MSMEs processes and the financial side alike Risk Capital for Social Enterprises that target underserved markets Financial Sector Side • The Project aims at: – Mobilising innovative financial instruments for social business financing – Policy advocacy with: • India Inclusive Innovation Fund (IIIF) for supporting non-technology social enterprises MSME Side • MSMEs which can be classified as social businesses need to be made investor-ready. • Needed: Development of an enabling environment for social businesses to operate easier Voluntary Principles and Self-Regulation for the financial sector Financial Sector Side MSME Side • The Project aims to mainstream responsible business conduct (especially among MSMEs) by working with key constituency, which is, the financial sector and developing ESG guidelines for more responsible lending and investment decisions • Challenges • MSMEs need to work towards becoming more sustainable in terms of environmental performance, employee health and safety and other such factors – Perceived lack of incentive to adopt the guidelines Overall challenges • Lack of capital • Lack of systems within • Lack of awareness amongs MSMEs

![[Burning Issue] MSMEs – The lifeline of the India…](http://s2.studylib.net/store/data/025647773_1-ec866fd77e058b2bbb32f78ef6bac097-300x300.png)