(a) consumption and

advertisement

consumption and")

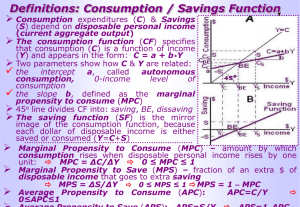

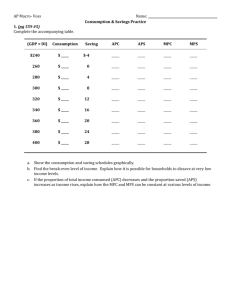

Ch 8. Basic Macroeconomic Relationships A. Income & consumption schedules. Consumption and disposable income, 1980 – 2002. Each dot shows consumption and DI in a given year. Line C generalizes the relationship between consumption & DI, indicates a direct relationship and shows that households consume most of their incomes. -- Savings (S) equals disposable income (DI) minus consumption (C). -- 45 degree line shows all points where DI and C are equal. -- The Consumption Schedule and the Savings Schedule. Basic Relationships • Income-Consumption • Income-Saving • 45° Line • C = DI on the Line • S = DI - C B. APC (average propensity to consume) APC = consumption income C. If a family’s C > DI, The APC is > 1. APS (average propensity to save) APS = saving income -- From the schedule before, the APC is 450 = 45 or about 96%. 470 47 -- The APS is 20 = 2 or about 4%. 470 47 -- ‘Average’ is for one year. APC + APS = 1 Consumption and Saving GLOBAL PERSPECTIVE Average Propensities to Consume Select Nations GDPs Average Propensities to Consume .80 .85 .90 .95 1.00 United States .963 Canada .958 United Kingdom .953 Japan .942 Germany .896 Netherlands .893 Italy France .840 .833 Source: Statistical Abstract of the United States, 2006 D. MPC (marginal propensity to consume) MPC = change in consumption change in income E. MPS (marginal propensity to save) MPS = change in saving change in income MPC + MPS = 1 -- ‘Marginal’ is over time MPC + MPS = APC + APS -- The graph is on the next slide. • (a) consumption and (b) saving schedule. • The saving schedule in (b) is found by subtracting the consumption schedule in (a) vertically from the 45 degree line. • Consumption equals disposable income (and savings equals zero) at $390 billion in this example. Consumption and Saving (1) Level of (2) Output ConsumpAnd tion Income (C) (GDP=DI) (1) $370 (4) (5) (6) (7) Average Average Marginal Marginal Propensity Propensity Propensity Propensity (3) to Consume to Save to Consume to Save Saving (S) (APC) (APS) (MPC) (MPS) (1-2) (2)/(1) (3)/(1) Δ(2)/Δ(1) Δ(3)/Δ(1) $375 $-5 1.01 -.01 (2) 390 390 0 1.00 .00 (3) 410 405 5 .99 .01 (4) 430 420 10 .98 .02 (5) 450 435 15 .97 .03 (6) 470 450 20 .96 .04 (7) 490 465 25 .95 .05 (8) 510 480 30 .94 .06 (9) 530 495 35 .93 .07 (10) 550 510 40 .93 .07 .75 .25 .75 .25 .75 .25 .75 .25 .75 .25 .75 .25 .75 .25 .75 .25 .75 .25 Consumption and Saving Consumption (billions of dollars) Consumption and Saving Schedules 500 C 475 450 425 Saving $5 Billion Consumption Schedule 400 375 Dissaving $5 Billion Saving (billions of dollars) 45° 370 390 410 430 450 470 490 510 530 550 Disposable Income (billions of dollars) 50 Dissaving Saving Schedule S 25 $5 Billion Saving $5 Billion 0 370 390 410 430 450 470 490 510 530 550 Consumption and Saving Consumption and Saving Schedules Consumption (billions of dollars) C1 C0 C2 Saving (billions of dollars) 45° Disposable Income (billions of dollars) S2 S0 S1 F.Expected Rate of Return – anticipated profit from investment. r = is expected to be 10% (on a $1,000 investment = $100/$1,000) G. Real Interest Rate – expressed in dollars (adjusted for inflation) & = to nominal interest rate less the rate of inflation. i = $1,000 times 7% = $70 ($30 profit) -- The interest-Rate-Investment Relationship. -- Investment is expenditures on new plants, equipment, machinery, etc. -- Nominal interest rate is not adjusted for inflation. H. Investment Demand Curve Rates of Expected Return and Investment Expected Rate of Return (r) 25% 20 15 10 5 0 Cumulative amount of investment having this rate of return or higher (in billions) $0 $10 20 30 40 50 Investment Demand Curve Inverse Relationship (sloping down) -- We move from a single firm’s investment to total demand by entire business sector. -- This shows the amount of investment forthcoming at each real interest rate. -- The level of investment depends on the expected rate of return & real interest rate. I. Shifts 1. Operating costs. 2. Business taxes. 3. Tech changes. 4. Stock of goods. 5. Expectations. Shifts of the Investment Demand Curve -- When these things change, the Demand Curve shifts. -- If businesses expect greater returns on their investments it increases investment demand and shifts the demand curve to the right (from ID₀ to ID₁). -- Expected lower rates of return moves the shift to the left (from ID₀ to ID₂). Interest Rate and Investment Shifts in the Investment Demand Curve r and i (percent) Increase in Investment Demand Decrease in Investment Demand 0 Investment (billions of dollars) ID2 ID0 ID1 6. Instability of investment. 7. Durability. 8. Irregularity of innovation. 9. Variability of profits. 10. “ of expectations. Interest Rate and Investment Percentage Change The Volatility of Investment Gross Investment GDP 1971 1975 1979 1983 1987 1991 Year 1995 1999 2003 J. Multiplier Effect: spending = GDP. Multiplier = Δ in real GDP initial Δ in spending If investment rises by $30 billion and the GDP rises by $90 billion, we then know that the multiplier is 3 (= $90/30). -- Other things equal, there is a direct relationship between changes in spending and changes in real GDP. -- The multiplier determines how much larger that change will be. -- Or, Change in GDP = multiplier x initial change in spending. MPC & MPS are #D & E • • • • • • $5 bill increase in the incomes of households MPC in .75 Raises consumption by $3.75 (.75 x $5) Savings by $1.25 (= .25 x $5 bill) column 2&3. 2nd round has $3.75 in consumption. Consume .75 of $3.75 ($2.81 bill), and save .25 ($.94 bill) -- Initial change of investment spending of $5 bill creates and equal $5 bill of new income. -- The multiplier is 4 (= $20 bill/$5 bill). The MPC and the multiplier are directly related and the MPS and the multiplier are inversely related. Multiplier = 1 1 – MPC Multiplier = 1 MPS -- Remember that MPC + MPS = 1. -- Therefore, MPS = 1 – MPC.