Steel: Not a Crisis, A Wake Up Call

advertisement

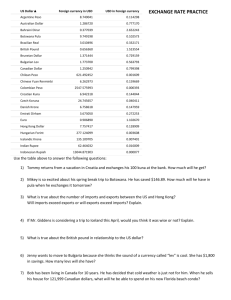

Steel: Not a Crisis, A Wake Up Call • The Topics – Immediate Issues • Supply and Demand – Demand or capacity? – Capacity or raw materials? – What happened and why? • Price Drivers – Raw materials (domestic/global) – Supply/demand factors versus “metal margin” – Much Bigger Issues • Manufacturing Issues • Currency Manipulation • The Tie-In to Trade Supply and Demand • The Global Capacity Situation – Overall – LFR • Global Raw Materials Infrastructure – Ore, Coke, Alloys – Scrap • The Results of Trade Abuse, Manipulation, Subsidy and Regulation – From “TPM” to “VRA” to “201 – Impact on earnings and investment/divestment – Welcome to globalization of strategic resources (action by other countries) Price Drivers • Raw Materials Changes – Ore, Coke, Scrap, Alloys • Energy and Other Inputs – Natural gas, freight/fuel (in/out) – Refractories, Maintenance • “Metal Margin” and Capacity Utilization – Where was it, where it is, where it should be (Nucor’s view) – Capacity Utilization Factors • Imports and Capacity Utilization • Capacity Utilization and Price ports and U.S. Capacity Utilization The Manufacturing Sector • By itself – the 5th largest “economy globally • Employs 14.3 million directly, millions more indirectly. • Consumes over 60% of R&D in U.S. • Is the country’s engine of growth and wealth • And, the sector is in big trouble The Problem Statement Manufacturing in this country is subject to massive regulation, pays for social issues handled by governments elsewhere and is under attack by well orchestrated offshore opponents. Only recently have policy makers seriously addressed core issues. However, problems have been studied to death. The time for action is now. We are running out of time. The Evidence • Studies point to several critical issues – NAM Study – DOC Study NAM Study • High Corporate Tax Rates • Cost of Health Benefits – Health Care – Private Pensions • Cost of Litigation • Cost of Regulatory Compliance • Energy Costs Quantified Findings - NAM • US manufacturing is “penalized” for being here to the • • • • tune of a 22.4% cost disadvantage versus major competing (developed) countries The trade playing field is not level whether related to subsidy/dumping or export incentives Continued lack of correction is creating a serious talent drain from manufacturing The damage to manufacturing will impact the industries that depend on manufacturing as a customer NAM has numerous recommendations and steps to address the issues Department of Commerce Study • Developed via “field” hearings and academic • input – parallels NAM findings but puts government spin on solutions Highlighted recommendations – Economic environment – – – – Make tax cuts permanent Reduce tax complexity and compliance costs Permanent tax credit for R&D Expand access to low cost capital DOC Study • “Investing in innovation” – – – – – Strengthen patent system “Review” federal R&D emphasis MEP enhancement (ended up cutting back program) “Promote” technology transfer Cooperative research programs – – – – Regulatory “review” Health care cost control “review” Legal reform Energy legislation • Lowering Costs Proposals DOC Study • Education, Retraining, Economic Diversification – Training partnership initiative – Analyze adequacy of existing training – Personal re-employment accounts (to finance retraining) – Economic adjustment programs for communities in transition – “Transform” workforce development programs DOC Study • Promote open markets/level playing field – “Encourage” economic growth, open trade, capital market access – “Negotiate” trade agreements that benefit US manufacturers – Enforce trade agreements/combat unfair trade – “Reinforce” promotion of American goods globally The DOC Study • “Enhancing” Government’s Focus on Manufacturing Competitiveness – Establish manufacturing council – New office of Industry Analysis – “Foster” government coordination Some Pitfalls in the DOC Report? – Emphasis on retraining, re-education, readjustment for communities impacted by closure, educational partnerships – Words like explore, study, support, promote and leverage are used throughout recommendations – Requires legislative changes on health care, tort reform, revamping energy policy and oversight group – little of which has been done Status • Czar has been appointed (Asst. Sec.) • Manufacturing council being established • Trade enforcement group being established • Intellectual property rights effort ongoing The Missing Element Currency intervention and manipulation has been given precious little attention in either report. Why? • Pic of China © 2003 by Prof. Werner Antweiler, University of British Columbia, Vancouver BC, Canada. Permission is granted to reproduce the above image provided that the source and copyright are acknowledged. © 2003 by Prof. Werner Antweiler, University of British Columbia, Vancouver BC, Canada. Permission is granted to reproduce the above image provided that the source and copyright are acknowledged. © 2003 by Prof. Werner Antweiler, University of British Columbia, Vancouver BC, Canada. Permission is granted to reproduce the above image provided that the source and copyright are acknowledged. © 2003 by Prof. Werner Antweiler, University of British Columbia, Vancouver BC, Canada. Permission is granted to reproduce the above image provided that the source and copyright are acknowledged. © 2003 by Prof. Werner Antweiler, University of British Columbia, Vancouver BC, Canada. Permission is granted to reproduce the above image provided that the source and copyright are acknowledged. Manipulated Currency Reserves AWASH IN DOLLARS Asia’s growing foreign reserves, in billions of dollars Country Year-End 2003 $673.5 Japan $403.3 China Taiwan South Korea Hong Kong India Singapore Malaysia Thailand Indonesia Phillipines Source: Reuters % Change From 2002 $206.6 $155.4 $118.4 $100.6 $96.3 $44.9 $42.1 $36.3 $16.7 43% 41% 28% 28% 6% 43% 17% 30% 6% 15% 5% Currency Manipulation • Market fundamentals have historically not set the value of the Japanese Yen, Taiwanese Dollar, Korean Won and Chinese Yuan – Governments Have! • China’s growing trade surplus and huge foreign investment inflows would suggest one thing – a stronger yuan – reality is vis-a-vis the U.S. dollar there has been no change • China, et al, aren’t the only problem – Russia devalued 485% in 1998, offset by 270% PPI increase for a net devaluation of 215% The United States’ Current Account Deficit $100 Dollars In Billions $0 ($100) ($200) ($300) ($400) ($500) ($600) '82 '83 '84 '85 '86 '87 '88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 The Effects of Intervention and Manipulation • On Manufacturing • On Steel – Imports – Pricing • On Other industries The Dollar Goes Up Manufacturing Profits Go Down 28 130 Broad Real Dollar Index (right scale) 24 115 20 100 16 85 12 70 8 4 Profit Share of National Income in Domestic Manufacturing (left scale) 1995 1996 1997 1998 1999 55 2000 2001 2002 Sources: Federal Reserve Statistical Release H.10; U.S. Department of Commerce, Bureau of Economic Analysis, National Income and Product Accounts 40 Overvalued Dollar Devastates U.S. Manufacturing Change in: Stable Dollar (‘91-’96) Strong Dollar (’97-’02) Trade Deficit - $176 billion - $468 billion Imports $800 billion One Trillion Dollars ! Exports + $204 billion - $80 billion “Six Years After” Coalition for a Sound Dollar March 2003 Overall Mfg. Capacity Utilization 85.0 82.5 80.0 77.5 75.0 72.5 70.0 67.5 ‘90 ‘91 ‘92 ’93 ’94 ’95 ’96 ’97 ’98 ’99 ’00 ’01 ’02 ’03 ‘04 150 When the Dollar goes up so do US Steel Imports 140 35 30 Steel Import Share (right scale) 130 25 120 20 110 15 100 10 Fed’s Broad Real Dollar (left scale) 90 80 1995 1996 1997 1998 1999 5 0 2000 2001 2002 Sources: Federal Reserve Statistical Release H.10; U.S. Department of Commerce, Bureau of Economic Analysis, National Income and Product Accounts Overvalued Dollar Hits U.S. Agriculture Change in: Stable Dollar (‘92-’96) Strong Dollar (‘97-’02) Exports: Up $20.9 billion Down $2.6 billion Imports: Up $9.2 billion Up another $7 billion Trade Surplus: Rose to $27 billion Fell to $11 billion Overvalued Dollar Hits U.S. High Tech Change in: Stable Dollar (’92-‘96) Overvalued Dollar (’97-‘02) Exports + $25 billion - $31 billion* Imports + $17 billion + $50 billion Trade Deficit + $35 billion (‘96) -$17 billion (‘02) Projection for 2002 based on YTD 9/02 figures. *Since 2000 peak. “Six Years After” Coalition for a Sound Dollar March 2003 U.S. Trade Balance in Advance Technology 30 20 Billions of $ 10 2002 0 1999 -10 -20 -30 Source: U.S. Census Bureau. 2000 2001 2003 Investments Are Down … $37 Billion The Trade Tie-In • “Free” trade cannot long endure if it isn’t fair trade • All metal sector manufacturers located in the U.S. will eventually be impacted – directly or indirectly – by currency manipulation and ineffective trade laws and/or lack of enforcement • There are solutions Solutions • AFL-CIO 301 Petition on WTO obligation • • • • violations by China (rejected by the administration) Emergency Steel Scrap Coalition (use of Export Administration law) FCA 301 Petition on currency manipulation (rejected by the administration) Trade law reform Pressure for aggressive enforcement of laws and trade agreements Trade Law Reform • What are the weaknesses in current laws? – Repeat dumping (country/product switching) – Major offenders provided special consideration that encourages repeat behavior – The WTO “legislation” problem • What are the solutions? – H.R. 2092 and S. 136 (Berry/Lincoln) – H.R. 3716 (English), S. 2212 (Collins, Bayh) – H.R. 2365 (English, Levin, Houghton, Cardin) and S. 1258 (Bayh) & S. 676 (Baucus) and H. Con. Res. 243 (Levin) Other Trade Related Reforms • Import Monitoring, Licensing and Enforcement • OECD Update – VERY instructive One Company’s Approach • Educate employees on issues germane to their jobs • Provide them the tools to reach elected representatives – local, state, national • Engage in the debate – thoughtfully, nonpartisan • Be an agent of awakening and change