4.01 STUDY GUIDE Procedure for Reconciling a Bank Statement

advertisement

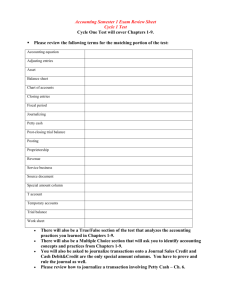

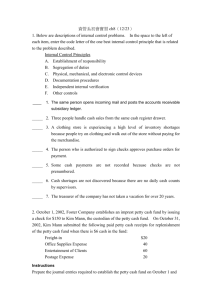

4.01 STUDY GUIDE I. Procedure for Reconciling a Bank Statement A. Procedure for calculating adjusted checkbook balance (left side of reconciliation form) 1. Write the date on the reconciliation form. 2. Record the balance from the checkbook. 3. Subtract any bank service charges in the Bank Charges section. 4. Write in the Adjusted Checkbook Balance. B. Procedure for calculating adjusted bank balance (right side of reconciliation form) 1. Write the date on the reconciliation form. 2. Record the ending balance from the bank statement. 3. Add outstanding deposits. 4. Calculate the subtotal. 5. Subtract outstanding checks. 6. Write in the Adjusted Bank Balance. C. Procedure for Comparing Adjusted Balances 1. If the two balances are equal, the account is reconciled. 2. If the two balances are not equal, find and correct the error(s) before any more work is done. II. Procedures for Recording and Journalizing a Bank Service Charge A. Procedure for recording a bank service charge in the checkbook 1. Write Service charge on the check stub under Other. 2. Write the amount of the charge in the Amount column. 3. Calculate and record the new subtotal. B. Procedure for journalizing a bank service charge 1. Write the date in the Date column of the Journal. 2. Write the title of the account to be debited, Miscellaneous Expense, in the Account Title column. 3. Record the amount debited in the Debit column. (If using a multicolumn journal, record the amount debited in the General Debit column.) 4. Write the title of the account to be credited, Cash, in the Account Title column. 5. Record the amount credited in the Credit column. (If using a multicolumn journal, record the amount credited in the Cash Credit column.) 6. Post the entry to the appropriate General ledger accounts. III. Procedures for Recording and Journalizing a Dishonored Check A. Procedure for recording a dishonored check on a check stub 1. Write Dishonored check on the line under the heading Other. (The amount to be recorded is the amount of the check plus any service fee charged by the bank.) 2. Write the total of the dishonored check in the amount column. 3. Calculate and record the new subtotal on the Subtotal line. B. Procedure for journalizing a dishonored check 1. Write the date in the Date column. 2. Write the title of the account to be debited, Accounts Receivable/Vendor, in the Account Title column. 3. Record the amount debited in the General Journal column. (Amount is the amount of the check and any bank service fee charged for the dishonored check.) 4. Write the amount credited in the Cash Credit column. 5. Write the source document number in the Doc. No. column. 6. Post the entry to the appropriate general ledger accounts. IV. Procedure for Reconciling General Ledger Cash Account to Balance with Adjusted Bank Balance A. After reconciling bank statement with checkbook, compare the general ledger Cash balance with the Adjusted Bank Balance. B. If all adjusting entries have been posted properly, the general ledger Cash account balance will equal the Adjusted Bank Balance and the Adjusted Checkbook Balance. 4.02 STUDY GUIDE V. Procedure for Establishing Petty Cash A. Petty cash is an amount of cash kept on hand and used for making small payments for which writing a check is not time- or cost-effective. B. Petty cash is an asset with a normal debit balance. C. Determine the amount of petty cash needed. D. Make the payment for petty cash (write the check). E. Journalize the petty cash transaction. 1. Debit Petty Cash. 2. Credit Cash. VI. Procedure for Replenishing Petty Cash A. Prove/reconcile petty cash. 1. Add all amounts on petty cash slips. A Petty Cash Slip or Voucher is a form showing proof of a petty cash payment and contains: a. Petty cash slip number b. Date of petty cash payment c. To whom paid d. Reason for the payment e. Amount paid f. Account in which the amount is to be recorded g. Signature of petty cashier – person approving the petty cash payment 2. Count cash remaining in the petty cash fund. 3. Compare the total of #1 + #2 with starting balance of petty cash. The two amounts should equal. (Possible Petty Cash Issues – Cash Over/Short occurs when the total amount of cash and petty cash slips in the petty cash fund does not agree with the reconciled petty cash balance.) B. Prepare a Petty Cash Requisition form for the amount needed to replenish petty cash. C. Journalize the entry to replenish Petty Cash. Three possible scenarios for the procedure include: 1. With no shortage or overage a. Debit the appropriate expense accounts. b. Credit Cash. 2. With an overage a. Debit the appropriate expense accounts. b. Credit Cash for the necessary amount to balance petty cash. c. Credit Cash Over/Short for the overage amount. 3. With a shortage a. Debit the appropriate expense accounts. b. Debit Cash Over/Short for the shortage amount. c. Credit Cash for the necessary amount to balance petty cash. 4.03 STUDY GUIDE VII. Procedure for Preparing and Recording a Payroll (Use a Payroll Register to record the following information.) A. Calculate employee hours. If hours are over 40 per week, overtime earnings must be calculated. B. Calculate regular earnings. Multiply hours worked up to 40 by hourly rate of pay. C. If hours are over 40, calculate overtime earnings. Multiply hours over 40 by hourly pay rate times 1 ½. D. Calculate total earnings by adding regular earnings and overtime earnings. E. Calculate deductions. 1. Social Security tax withholding (multiply total earnings by 6.2%) 2. Medicare tax withholding (multiply total earnings by 1.45%) 3. Federal income tax withholding (use federal tax tables) 4. State income tax withholding (use state rate or state tax tables) 5. Other deductions – some employers will have other deductions such as health insurance, etc. F. Calculate total deductions. (Add all deductions together). G. Calculate net pay. (Subtract total deductions from total earnings). H. Prepare payroll checks. (Write checks for net pay amount.) VIII. Procedure for Journalizing a Payroll A. Total all columns of the Payroll Register. Prove register by checking totals across for accuracy. B. Write the date in the Date column of the General Journal. C. Debit Salary Expense for the total earnings amount. D. Credit appropriate liability accounts for the deductions. 1. Credit Social Security Tax Payable for the total Social Security tax withholding. 2. Credit Medicare Tax Payable for the total Medicare tax withholding. 3. Credit Federal Income Tax Payable for the total federal income tax withholding. 4. Credit State Income Tax Payable for the total state income tax withholding. 5. Credit any other appropriate liabilities for other deductions. E. Credit Cash for the total net pay amount. F. Post the entry to the appropriate general ledger accounts. IX. Procedure for Calculating Employer Payroll Taxes A. Social Security tax – Multiply total earnings by 6.2%. (Employers pay the same amount of Social Security tax as employees.) B. Medicare tax – Multiply total earnings by 1.45%. (Employers pay the same amount of Medicare tax as employees) C. Unemployment taxes 1. Federal unemployment tax – 0.8% of the first $7,000.00 earned by each employee a) The actual federal rate used for calculating federal unemployment tax is 6.2% of the first $7,000.00 earned by each employee. b) Employers can receive a credit up to 5.4% of taxable earnings for the amounts paid for state unemployment tax, which results in the 0.8%. 2. State unemployment tax – rates and tax bases vary based on the state. X. Procedure for Journalizing Employer Payroll Taxes A. Write the date in the Date column of the General Journal. B. Debit Payroll Taxes Expense for the total of the employer’s Social Security, Medicare, federal unemployment, and state unemployment taxes. C. Credit the appropriate liability accounts. 1. Credit Social Security Tax Payable for the employer’s Social Security tax amount. 2. Credit Medicare Tax Payable for the employer’s Medicare tax amount. 3. Credit Federal Unemployment Tax Payable for the federal unemployment tax amount. 4. Credit State Unemployment Tax Payable for the state unemployment tax amount. 5. Post the entry to the appropriate general ledger accounts. XI. Procedure for Journalizing the Payment of Social Security, Medicare, and Federal Income Taxes A. Write the date in the Date column of the Cash Payments Journal. B. Debit the appropriate tax liability accounts. 1. Debit Social Security Tax Payable for the amount of Social Security tax paid. (Employer and Employee) 2. Debit Medicare Tax Payable for the amount of Medicare tax paid. (Employer and Employee) 3. Debit Federal Income Tax Payable for the amount of federal income tax paid. (Employees) C. Credit Cash for the total of the taxes paid. D. Post the entry to the appropriate general ledger accounts. XII. Procedure for Journalizing Payment of Federal Unemployment Taxes A. Write the date in the Date column of the Cash Payments Journal. B. Debit Federal Unemployment Tax Payable for the amount of federal unemployment tax paid. C. Credit Cash for the amount of federal unemployment tax paid. D. Post the entry to the appropriate general ledger accounts. XIII. Procedure for Journalizing Payment of State Unemployment Taxes A. Write the date in the Date column of the Cash Payments Journal. B. Debit State Unemployment Tax Payable for the amount of state unemployment tax paid. C. Credit Cash for the amount of state unemployment tax paid. D. Post the entry to the appropriate general ledger accounts.