last two weeks presentation

advertisement

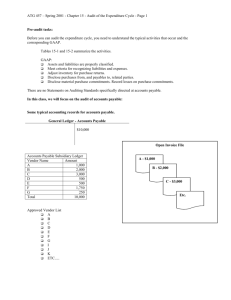

WHAT’S NEXT...?!! 2 WEEKS & FINAL EXAM!!!!!! FINAL EXAM TWO OF FOUR ESSAYS TEN MULTIPLE CHOICE 200 100 COMPREHENSIVE ESSAY AUDIT THEME RELATE AUDIT PHASES AUDIT FINDINGS COMPREHENSIVE ESSAY AUDIT PROCESS HANDOUT SIX PHASES ACTIVITIES PRODUCTS SECOND ESSAY 1 OF OTHER 3 QUESTIONS ONLY RECENT STUFF AUDIT REPORTS ALL BUT ONLY ONLY RECENT STUFF CASH ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE EXPENSES/CUTOFFS INVENTORY FIXED ASSETS ONLY RECENT STUFF SUBSTANTIVE TESTS OF BALANCES WRAP-UP PHASE - SEARCH FOR UL & SSE - SUMMARIZE & CONCLUDE - PJE ISSUE REPORT EXPENDITURE CYCLE MIRROR OF THE REVENUE CYCLE EXPENDITURE CYCLE PREPAID EXPENSES ACCOUNTS PAYABLE & ACCRUED LIABILITIES EXPENSE ACCOUNTS ACCOUNTS PAYABLE & ACCRUED LIABILITIES LIABILITIES - FOCUS ON UNDERSTATEMENT WORKPAPER SCHEME BSL AA LEAD AA-1 A/P T/B AA-1/1 CONFIRMS AA-2 A/L ANALYSIS AA-1/2 SEARCH FOR U/L ACCOUNTS PAYABLE & ACCRUED LIABILITIES TRIAL BALANCE OF A/P X-REF TO LEAD FOOT ALL & ONLY TEST TO/FROM A/P SUBSIDIARY LEDGER WORKPAPER SCHEME BSL AA LEAD AA-1 A/P T/B AA-1/1 CONFIRMS AA-2 A/L ANALYSIS AA-1/2 SEARCH FOR U/L CONFIRMATION OF A/P SELECT SAMPLE MAIL 1st & 2nd REQUESTS NONREPLIES TOTAL ERRORS IN SAMPLE EXPLODE TO POPULATION SELECTING SAMPLE BLIND REQUESTS ZERO BALANCE ACCOUNTS MAJOR SUPPLIERS VOUCHING A/P VOUCHING - Examine documents supporting a payable or disbursement VOUCHING A/P VENDOR’S INVOICE BILL OF LADING & PACKING LIST RECEIVING DOCUMENTS PURCHASE ORDER CHECK REQUEST SEARCH FOR UNRECORDED PAYABLES PART OF WRAP UP PHASE & A CUTOFF TEST SEARCH FOR UNRECORDED PAYABLES EXAMINE SUBSEQUENT C/D OVER A $ SCOPE LIST C/D RELATED TO Y/E TRACE TO RECORDED A/P TOTAL UNRECORDED A/P PROPOSE JOURNAL ENTRY SEARCH FOR UNRECORDED PAYABLES CONTINUES THRU LAST DAY OF FIELD WORK GRADUATED SCOPE AUDITING EXPENSES AUDITING BY EXCEPTION ALREADY PERFORMED? UNDERSTANDING CLIENT ASSESS INTERNAL CONTROL TEST CONTROL TECHNIQUES SUBSTANTIVE TESTS TESTS OF Y/E A/P ALREADY PERFORMED? WAGE & SALARY EXPENSE Payroll cycle audit DEPRECIATION EXPENSE - Audit of Fixed Assets INTEREST EXPENSE - Audit of Loans Payable COST OF GOODS SOLD - Audit of Inventory & Sales AUDIT BY EXCEPTION DO ANALYTICAL REVIEW FOR UNUSUAL VARIATIONS, DO ADDITIONAL WORK - Reasonable Business Explanation - Error and PJE NO UNUSUAL VARIATIONS, STOP AUDIT EXPENSES SOME HIGH RISK EXPENSES ARE ALWAYS ANALYZED - Travel & Entertainment - Legal & Professional Fees - Donations - Repairs & Maintenance PRODUCTION CYCLE INVENTORY FIXED ASSETS PHYSICAL COUNT COUNT COMPILATION (VALUATION) BOOK-TO-PHYSICAL ADJUSTMENT COUNT - CLIENT MUST DO BEFORE THE COUNT - Housecleaning Disposal of damaged/obsolete goods Close shipping/receiving & production around Y/E Written count plan/instructions Preprinted count tags or lis (Blind or prepared media?) Count team meeting COUNT - CLIENT MUST DO DURING THE COUNT Assigning teams to segregate duties Assigning recounters & supervisors Maintaining count tag control Count & recount Resolving counting problems Shipping & receiving during count Review for completeness Collect & account for all tags Complete count tag control COMPILATION - CLIENT MUST DO AFTER THE COUNT Sort & accumulate count tags Transcribe counts from tags to medium Adjust counts for in-transit items Price items using FIFO or LIFO Apply Lower-of-cost-or-market to items Extend and foot inventory Record book-to-physical adjustments BOOK-TO-PHYSICAL CLIENT MUST DO CALCULATE ADJUSTMENT RECORD ADJUSTMENT COUNT - AUDITOR MUST DO BEFORE THE COUNT - Review count plan Pre-count tour of facilities Identify most valuable items Attend count team meeting Assure shipping/receiving & production are closed COUNT - AUDITOR MUST DO DURING THE COUNT - Observe counters Do test counts Observe handling of count problems Observe count tag control process Observe rust, dust & dents Obtain shipping/receiving cutoff samples Count high value items Calculate rough estimate of total inventory Review for completeness Observe collection of & accounting for tags COMPILATION - AUDITOR MUST DO AFTER THE COUNT Do all & only tests for tags Tie in counts of high value items Test pricing Test lower-of-cost-or-market Check extensions & footings BOOK-TO-PHYSICAL ADJUSTMENT - AUDITOR MUST DO CHECK CALCULATION CHECK POSTING SHIPPING/RECEIVING CUTOFF TESTS Sample of last shipping/receiving documents before y/e Sample of first shipping/receiving documents after y/e Trace shipments to sales recorded in Sales Journals Trace receipts of goods to purchases recorded in Purchases Journals Consider effect of FOB shipping terms Propose adjustment for any errors in cutoff CUTOFFS SEE PROBLEM 21-32 ON PAGE 662 AUDIT OF FIXED ASSETS Differences from audit of receivables & inventory Focus on current activity – not whole balance Fewer transactions Large, complex transactions Peripheral costs Financing affects value recorded Liens on assets Physical existence AUDIT OF FIXED ASSETS Vouching sample of additions Capitalize v. Expense Tests of depreciation Tax basis as well as book basis significant Auditing sample of disposals Gain/Loss on disposal Trade-ins v. sales Periodic physical counts & unrecorded disposals Impairments in value