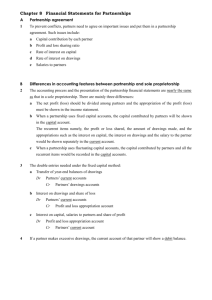

1 Partnership

Tutor: Marie O’Callaghan

Sole Trader

Unlimited

Liability

Company

Partnership

Limited

Liability

Partnerships

• Professionals such as doctors, lawyers ,dentists, vets,

accountants are not allowed to form companies.

• There are advantages to partnerships over forming a

company from the point of view of tax, accounting and

disclosure requirements.

• Partnerships do not go through a registration process to

form.

• Partnership is not a separate legal identity = partners have

unlimited liability, unlike directors or shareholders in

companies.

• The downside is that each partner is liable for the losses of

his co-partner in carrying on the partnership business, even

where the other partner has defrauded clients of the

business.

Partnership Act 1890 - Amended 1907

• Partnership Act 1890 defines a partnership

and essentially states that where 2 or more

people carry on business with a common view

of profit, then a partnership exists.

• A written partnership agreement is not

necessary.

• The act applies where no partnership

agreement is in place.

The Main Provisions

1.

2.

3.

4.

5.

6.

7.

8.

P&L must be shared equally

No interest paid on capital

No remuneration

Differences settled by majority

Change of business requires consent of all

No right to expell a partner

No right to retire

All Partners have the right:

1.

2.

3.

4.

5.

Take part

Prevent entry of another partner

Examine the books

Receive interest 5%PA on loans/advances ex capital

Dissolve the partnership

9. does not prevent a former partner from competing after leaving

10. Partnership dissolves automatically on

1.

2.

3.

death of partner

bankruptcy of partner

Illegal activity of partnership

Written Agreement

Written partnership agreement is crucial to set out:

• Function of the partnership

• Capital each partner will invest

• The profit sharing ratio

• The role of each partner

• Drawings – remuneration

• Expulsion

• New partners

• non compete agreement

• Dissolution

• etc.

Written Partnership agreement overrides the terms of the act

Partnership

Accounting

Capital A/C

• Records the original monies invested

• Usually remains fixed unless

– More capital introduced

– Non-current assets re-valued

– Goodwill crystallised and recognised

• Credit balance

– Credit the giving: partners giving capital to the

business

1 ABC Opening credit balances

2 B introduces additional capital

3 C withdraws capital

4 ABC Capital upward adjustment for recognition of goodwill and positive re-valuation of assets

Capital Account

DATE

DETAILS

PARTNERS

A

3/3/..

31/12

B

Bank

Balance

c/d

DATE

DETAILS

C

X

X

X

X

X

X

X

PARTNERS

A

B

C

X

X

X

1/1/..

Balance b/d

2/2/..

Bank

31/12

Goodwill

X

X

X

31/12

Revaluation

X

X

X

X

X

X

X

X

X

1/1/..

Balance b/d

X

Current A/C

• Short term element of each partners capital

• Record for each partner

– Share of profit/loss

– Drawings

– Interest on loans given to partnership

– Interest on credit capital

• Corresponding entry in appropriation

Current A/C - Partner A

DATE

DETAILS

31/12/..

31/12/..

31/12/..

DATE

DETAILS

Drawings

1/1/..

Balance b/d

Interest on Draw

31/12/..

Interest on Cr bal

31/12/..

Interest on Cap

31/12/..

Loan Interest

31/12/..

Share of Profits

1/1/..

Balance b/d

Balance c/d

€

€

Partner A

Debit

• Drawings – withdraw from

cash instead of salary

• Interest on drawings –

charge for overdraw

Credit

• Interest on Credit balance –

interest on investment held

in the current account

• Interest on Capital – interest

earned on original

investment

• Loan Interest – interest due

(not yet paid) for a loan

given to the partnership

• Share Profits – divide of

profit

Current A/C - Partner B

DATE

DETAILS

1/1/..

€

DATE

DETAILS

Balance b/d

31/12/..

Interest on Cap

31/12/..

Drawings

31/12/..

Share of Profits

31/12/..

Interest on

Drawings

31/12/..

Salary

31/12/..

Interest on Debit

bal

31/12/..

Balance c/d

1/1/..

Balance b/d

€

Partner B

Debit

• Interest on Debit balance –

money take out of the

partnership/loan from

business – interest charged

Credit

• Salary – reward for taking

extra responsibility or work

Current A/C - Partner C

DATE

DETAILS

31/12/..

31/12/..

31/12/..

DATE

DETAILS

Drawings

1/1/..

Balance b/d

Interest on Draw

31/12/..

Interest on Cr bal

31/12/..

Interest on Cap

31/12/..

Salary

31/12/..

Share of Profits

1/1/..

Balance b/d

Balance c/d

€

€

Partner C

Debit

Credit

• Capital – partner introduced

more capital to the

business.

Appropriation A/C

• In a partnership, the profits earned are due to

the various partners in their profit sharing

ration and are apportioned to them in the

appropriation section on the Statement of

Comprehensive Income

• 3 Sections

– Distributable income (Profit for year)

– Balance of Net Profit

– Share of Profit (as per PSR)

Appropriation Account for year ended 31/12/..

€

€

Gross Profit

X

Other Partnership Expenses

(X)

Interest on Loan by partners to business

(X)

Profit for Year

XX

*Other Comprehensive income for the year

X

Total Comprehensive income for the year

X

*Distributable income (Profit for year)

XX

Appropriation Account for year ended 31/12/..

Salaries: A

(X)

B

(X)

C

(X)

Interest on capital Accounts: A

(X)

B

(X)

C

(X)

Interest on Current Accounts:

X

C

(X)

A

(X)

(X)

B

Interest on Drawings:

Balance of Net Profit

A

(X)

(X)

X

B

X

C

X

X

XXX

Appropriation Account for year ended 31/12/..

€

€

Share of Profit (as per PSR)

A

X

B

X

C

X

XXX

Statement of Financial Position

• Equity Section

– List of the closing balances from the partners

capital and current accounts.

Statement of Financial Position as at 31/12/..

€

Capital Account

Current Account

A

X

B

X

C

X

A

X

B

(X)

C

X

€

X

X

XX

0

0