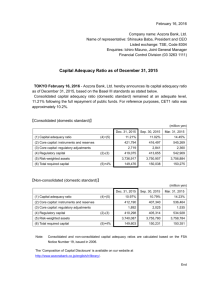

Reform of Capital Adequacy and Solvency Standards

advertisement