Econ_Chap1

advertisement

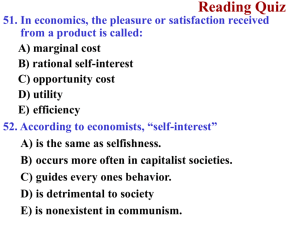

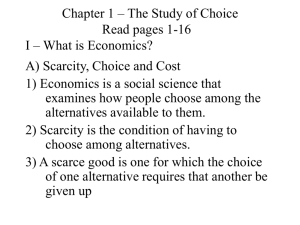

Chapter 1: Limits, Alternatives, and Choices Economics: social science that is concerned with how individuals, institutions, and society make optimal (best) choices under conditions of scarcity The economics way of thinking or economic perspective ha several interrelated features: o Scarcity and choice o Purposeful behavior o Marginal analysis Scarcity economic resources means limited goods and services Because of scarcity, we must choose what goods and services to produce with out limited resources Once a choice is made, the value of the next thing forgone is the opportunity cost. Individuals seeks to maximize their utility o Utility: the pleasure or satisfaction from consuming a good or services Economic decisions are “rational” or “purposeful” because the costs and benefits of the decisions are weighed Individuals compare the marginal benefits and marginal costs in making economic decisions. o Marginal means “extra” or “additional” So long as marginal benefits are greater than marginal costs, we consume (or produce) more. When marginal costs exceed marginal benefits, we consume (or produce) less. A summary of the same scientific method: o Observing real-world behavior and outcomes o Formulating a hypothesis of cause and effect o Testing the hypothesis o Accepting, rejecting, or modifying the hypothesis o Continued testing of the hypothesis against the facts, evolving into a theory as favorable results accumulate A very well-tested widely accepted theory is called an economic principle Economic principles and models: o Are generalizations o Incorporate the other-things-equal-assumption or ceteris paribus o Are expressed graphically Microeconomics: o Studies behavior of the individual units such as a household, a firm, or an industry. Macroeconomics: o Examines the economy as a whole or its basic subdivisions or aggregates, such as the government, household, and business sectors. Both microeconomics and macroeconomics contain elements of positive economics and normative economics o Positive economics: focuses on facts and cause-and-effect relationships- what is o Normative Economics: incorporate value judgments about what the economy should be like- what ought to be Limited Income: We have a finite amount of income, which means we must decide how to apportion this limited income for goods and services. Unlimited Wants: We have virtually unlimited wants ranging from necessities such as food and shelter to luxuries such as perfumes and sports cars. Budget Lines (constraints) depict the various combinations of two products a consumer can purchase with a specific money income. All combinations on or inside the budget line are attainable All combinations beyond the budget line are unattainable. A budget line illustrates the idea of tradeoffs arising from limited income The budget line illustrates those choices that are attainable The location of the budget line varies with money income. The four general categories of inputs include: o Land: including natural resources o Labor: the physical and mental talents of humans o Capital: manufactured aids such as tools and factories o Entrepreneurial Ability: a special human resource distinct from labor.