home-insurance-review - Bridges In Real Estate

advertisement

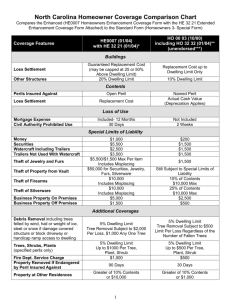

Manager Joe Kemp, CLF Financial Representative Office: Wood Village (503) 492-2228 • 11 Years Financial Planning Industry Experience • Licensed Securities Representative • Registered Principle • Licensed Insurance professional • Member NAIFA (National Association of Insurance and Financial advisors) • Member GAMA (General Agency Managers Association) • 2010 Regional Champion Agency Manager • 2010 Agency of the Year • 2010 Gama – Diamond International Management Award for excellence Home Insurance and Your Financial Security Common Misconception’s • What my policy covers • What my policy is Everything is covered Home Insurance Policy Maintenance Policy We know this is not the case What can effect my insurance costs? • • • • • • • • • • • • Credit Prior Claims (C.L.U.E. Reports) Flood Zones Distance to a Fire Department and Hydrant •Fire Protection Class Code (From Fire Department) Zip Code the Home is in Age of the Home Condition of the home Solid Fuel Burning Units (wood stoves) Alarm Discounts Multi Policy Discounts Deductible Coverage selected What are the Parts to a Home Insurance Policy Liability (Bodily Injury, Property Damage and Medical Payments) Dwelling Coverage Amount Deductible Perils Insured against Additional Structures Personal Property Settlement Options Loss of Use Limitations Exclusions Discounts Lets Start with Liability Pop Quiz One windy night your neighbors tree falls on your home causing massive damage. Can you go after his insurance? Liability Coverage Personal Liability (Bodily Injury and Property Damage) • Coverage for you when you are on or off your premises and will cover you when you are legally responsible for an act that causes damage to someone else’s person or property • Covers cost of Defense if you are sued • Multiple Liability Limit Options = $50,000 to $1,000,000 Medical Payments Liability • Covers medical expenses stemming from injuries that occur to others while they are on your premises regardless of fault • Multiple Medical Limits ($1000, $2000, $5000, $10,000, $25,000) Extending Liability (not all companies allow this) • Allows you to extend the Liability coverage you have on your main home to other homes you own • Saves money as you don’t have to have liability on your rental insurance policy • Great for multi property owners Liability Coverage (cont.) Personal Injury Liability (can be added to policy) This endorsement provides liability coverage for personal injury from one or more of the following: • false arrest, detention, imprisonment, or malicious prosecution, • libel, slander, defamation of character or a violation of a person’s right of privacy, or • wrongful entry, eviction, or the invasion of a person’s right to private occupancy Business Related Liability (limited exposures can be added) • Not intended to be a business policy – can jeopardize coverage • Farming, Child Care, Wood Working, Barber or Beautician etc.. (check with your insurer) Dwelling Coverage Dwelling • applies to the structure you inhabit. This would cover the dwelling, attached structures (garage, breezeway) and permanently installed property (wall to wall carpet, etc.) How do you choose an amount? • • • • • Don’t take this lightly 2 out of every 3 homes are underinsured Most Insurers cap coverage or provide an additional % (extended replacement) Trouble with Insuring to Market Value Article Replacement cost calculators **Additional Replacement Coverage**(Hard to find) Pays full replacement cost of your home, even if the amount of loss is greater than the limits on your policy Dwelling Coverage Additional Structures • Applies to other structures on your property, like tool shed, separate garage, green house, fencing etc. • 10% of what you insure the home for (can be increased if needed) • Does not cover – Structures that are used in a business or farming etc. What am I insured against? • • • • You actually choose this coverage and it is called Peril coverage Basic Form Broad Form Special Form Coverage (This is the premiere coverage) Broad Form Perils Special Form Perils Changes the policy language to: • Provides coverage for losses not specifically excluded in the policy • This is the premier coverage you should have Normally Excluded Losses: • • • • • • • • • Earthquake Flood Earth Movement Sump Pump Failure Sewer Backup Seepage of water Homes unoccupied for 60 days Business related losses Rule of thumb – It must be sudden and accidental Additional Coverage's Personal Property What's Covered: • The basic home insurance policy provides blanket coverage for personal property owned or used by the named insured and family members anywhere in the world. • 10 percent of the amount (minimum of $1,000) to cover personal property located at another residence, like a seasonal dwelling. Does not apply to property in a rental dwelling. Limit Varies by Company: Usually 75% of what you insure the home for (200,000 home = 150,000 for the contents) Limitations on Personal Property How are claims settled on Dwelling and Personal Property Again, you choose Actual Cash Value: • Pays Replacement cost minus Depreciation • This is one of the main causes of dissatisfaction when a claims are settled Replacement Cost: • Pays cost of replacing the item at current market value You get ACV until you actually replace item (personal property) Additional Types of Home policies Condo’s: • Specifically designed to cover the interior of the home (“studs” in coverage) • Drywall, Light fixtures, cabinets, subfloor, carpet, railings, countertops, etc. ** LOSS ASSESSMENT** Condominium, townhouse and homeowner associations generally assess the unit owner for their share of any loss which isn’t fully covered by the association’s insurance policy, including liability and physical damage claims. Additional Types of Home policies Rental’s: • • • • • • Insured like Owner Occupied Does not provide personal property (some insurer’s provide up to $2500 to cover appliances) Home is limited to amount of coverage without extended % increase Unlimited coverage not available Most insurers only allow Broad form Peril coverage Some property types need to go on a commercial policy (whole other animal) What insurance is supposed to do Take you from this To this What should you do? Partner with your COUNTRY Financial Representative to review your current financial scenario. Providing Financial Security since 1925