Full Article - Scott + Company

advertisement

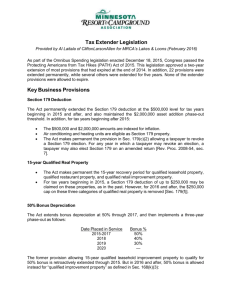

Congress Extends, Makes Permanent Business-Friendly Tax Provisions By Tony Perricelli For all of 2015, CPAs, tax preparers, and many of their tax-paying clients were frustrated by the lack of certainty in the tax law. As we neared the end of the year we wondered if Congress would pass legislation extending many of the provisions that expired at the end of 2014. Some of these provisions had become very important to business owners and individuals seeking to minimize their tax burdens so we were eager to see them extended. Congress finally came through in mid-December and even added something unexpected to the mix—permanent status for some items that had typically been only extended year-to-year. The PATH Act On December 18, 2015 President Obama signed the Protecting Americans from Tax Hikes Act of 2015 (PATH Act). The PATH Act accomplishes two things of particular interest to businesses. First, it makes permanent certain key business tax provisions that previously only had temporary status. Second, it extends other provisions for a period ranging from two to five years. Permanent status was granted to several business-friendly provisions including: Enhanced Sec 179 expensing The Research Tax Credit 15-year cost recovery for qualified leasehold improvements, restaurant property, and retail improvements Enhanced Section 179 expensing Without passage of the PATH Act, Sec 179 expensing for businesses would have plummeted to $25,000 on a maximum property investment of only $200,000 for 2015. With the PATH Act, though, the 2015 amounts are now back to 2014 levels--a $500,000 maximum deduction that does not phase out until you reach $2 million in property acquisitions each year. These new 2015 amounts will also be indexed for inflation beginning with the 2016 tax year. Research & Development Credit The PATH Act also permanently extends the Research & Development (R&D) Tax Credit, a credit for companies that invest in qualified research expenses. Research-intensive businesses have clamored for a permanent extension of this credit for years because of the long-term nature of many research and development activities. In addition to a permanent extension, the PATH Act also adds two new features to the R&D Credit that will benefit small businesses and startups. First, the R&D Credit will now be allowed to offset Alternative Minimum Tax for eligible small businesses that are privately held and have $50 million or less in revenue. Second, startup companies with current year revenue of less than $5 million and no previous revenues can use the R&D credit to offset their employer’s payroll tax up to $250,000 if they don’t have taxable income. Permanent status and the enhanced ability for smaller and startup businesses to use it will make the R&D credit a boon to technology-based businesses for many years. 15-year cost recovery The PATH Act permanently extends a special 15-year cost recovery rule for certain types of real estate improvements. Under general tax rules, improvements to real estate are depreciated over 39 years for commercial property. Several years ago, Congress acknowledged that many property users—in particular, those in the restaurant and retail industries or using space for commercial offices—will improve or refresh their properties more often than once every 39 years. To give such users the ability to deduct their improvement costs more quickly and avoid continuing to depreciate outdated costs, Congress passed a special 15-year cost recovery exception for three categories of improvements: Qualified leasehold improvements—generally commercial office space Qualified restaurant property—more than 50% of property is used for prep & consumption of meals Qualified retail property—property open to the public selling tangible goods The special 15-year rule is only allowable for properties that have been in service more than 3 years at the time the improvements are made and does not apply to improvements that enlarge the building. New for 2016, bonus depreciation (as described in the next section of this article) is allowed for a new class of property called “qualified improvement property” or QIP. QIP is defined similarly to Qualified Leasehold Improvements but with two changes. The new law removes the 3 year use rule and the requirement that the improvements must be made pursuant to the terms of a lease. This allows bonus depreciation to be taken by either the tenant or the owner of the property—a change from prior years. Also a change from prior years, most restaurant and retail improvements fall under the definition of QIP so they are now eligible for bonus depreciation. Temporary Extensions The PATH Act also extended many tax provisions on a temporary basis. Probably of most interest to businesses is the extension of bonus depreciation for 5 years and at declining rates and the two-year extension of the Work Opportunity Tax Credit. Bonus depreciation is similar to Sec 179 expensing in that it allows an immediate deduction for purchases of property that would otherwise be depreciated over several years. Unlike Sec 179, though, bonus depreciation is only allowed on a pre-set percentage of the purchase price and the property must be purchased new—no used items. The PATH Act lays out the pre-set percentages to be deducted each year of the extended period as follows: 50 percent for 2015-2017 (same as before the extension) 40 percent in 2018 30 percent in 2019 After 2019, bonus depreciation will once again expire and will have to be renewed by Congress. The Work Opportunity Tax Credit is a credit employers can take if they hire employees from targeted groups such as: Recipients of public assistance and food stamps Ex-felons Recipients of SSI Unemployed or disabled veterans Long-term unemployed individuals The employer who hires individuals from these qualifying groups can take a credit of up to 40% of the $6,000 of wages paid to the employee. The PATH Act also contains numerous permanent and temporary extensions of individual tax provisions. For more details on the individual extenders, please visit our website at www.scottandco.com.