Financial feasibility analysis

advertisement

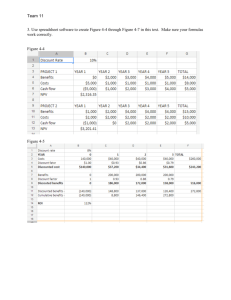

Financial Feasibility Analysis Energizing Cleaner Production Management Course 1 Session Agenda: Introduction Cash Flow Profitability Indicators 1. Simple Payback 2. Return on Investment (ROI) 3. Net Present Value (NPV) 4. Internal Rate of Return (IRR) 2 Step 1: Planning and Organization But first… In what step(s) of the methodology is financial feasibility analysis relevant? • • • • • task 1a: Meeting with top management task 1b: Form a Team and inform staff task 1c: Pre-assessment to collect general information task 1d: Select focus areas task 1e: Prepare assessment proposal for top management approval Step 2: Assessment • • • • • task 2a: Staff meeting and training task 2b: Prepare focus area flow charts task 2c: Walkthrough of focus areas task 2d: Quantify inputs and outputs and costs to establish a baseline task 2e: Quantify losses through a material and energy balance Step 3: Identification of Options • task 3a: Determine causes of losses • task 3b: Identify possible options • task 3c: Screen options for feasibility analysis Step 4: Feasibility Analysis of Options • task 4a: Technical, economic and environmental evaluation of options • task 4b: Rank feasible options for implementation • task 4c: Prepare implementation and monitoring proposal for top management approval Step 5: Implementation and Monitoring of Options • task 5a: Implement options and monitor results • task 5b: Evaluation meeting with top management Step 6: Continuous Improvement • task 6a: Prepare proposal to continue with energy efficiency for top management approval 3 Introduction Step 4 – Feasibility Analysis Technical Other - Regulatory - Organizational - Health/safety - Community Project Selection Company’s priority Financial Environmental 4 Introduction Questions Management Will Ask 1. Is the project profitable? • Initial investment costs • Annual operating costs and savings – Cost of operating inputs – Cost of waste management – Less tangible costs – Revenues 2. Determine availability of internal investment funds for bigger projects 3. Obtain external financing for remaining projects 5 Introduction Capital Budgeting Process Process by which organisation decides: • Which investment projects are – Needed – Possible – Special focus on projects that require significant up-front capital investment • How to allocate available capital between different projects • If additional capital is needed 6 Introduction Capital Budgeting Practices • Vary widely from company to company – Larger companies tend to have more formal practices than smaller companies – Larger companies tend to make more and larger capital investments than smaller companies – Some industry sectors require more capital investment than others • Vary from country to country 7 Introduction Typical Project Types and Costs • Maintenance – Maintain existing equipment and operations • Improvement – Modify existing equipment, processes, and management and information systems to improve efficiency, reduce costs, increase capacity, improve product quality, etc. • Replacement – Replace outdated, worn-out, or damaged equipment or outdated/inefficient management and information systems 8 Cash Flow Cash Flow Concept Common management planning tool Distinguishes between • Costs: cash outflows • Revenues/savings: cash inflows 9 Cash Flow Types of Cash Flow One-time Outflow Inflow Initial investment cost Equipment salvage value Annual Operating costs & taxes Operating revenues & savings Other Working capital Working capital 10 Cash Flow Costs and Savings • Initial investment costs – purchase of the camera system, delivery, installation, start-up • Annual operating costs (and savings) – Operating input — materials, energy, labour – Incineration — fuel, fuel additive, labour, ash to landfill – Wastewater treatment — chemicals, electricity, labour, sludge to landfill 11 Cash Flow Working Capital and Salvage Value • Working capital: total value of goods and money needed to maintain project operations – – – – Raw materials inventory Product inventory Accounts payable/receivable Cash-on-hand • Salvage Value: resale value of equipment or other materials at the end of the project 12 Cash Flow Timing End of project: Salvage Value Annual Revenues/Savings Year 1 Year 2 Year 3 TIME Time zero: Initial Investment 13 Cash Flow Incremental Analysis • Needed for many CP or EE projects • Compares cash flow of implemented options to the “business as usual” cash flow • Covers only the cash flows that change 14 Profitability Indicators • Definition: “a single number that is calculated for characterisation of project profitability in a concise and understandable form” • Common indicators 1. 2. 3. 4. Simple Payback Return on Investment (ROI) Net Present Value (NPV) Internal Rate of Return (IRR) 15 1. Simple Payback • Definition: number of years it will take for the project to recover the initial investments • Usually a rule of thumb for selecting projects, e.g. payback must be < 3 years Simple Payback (in years) = Investment Cash Flow 16 2. Return on Investment • Definition: the percentage of initial investment that is recovered each year Initial Investment Simple Payback = (in years) Year 1 Cash Flow ROI (in %) Year 1 Cash Flow = 3 years 33% Initial Investment 17 Workshop Exercise PLS Company: produces rolls of laminated film plastic film, aluminium film, adhesive solvent air emissions solvent air emissions INVENTORY plastic film, ink PRINTING printed printed laminated film film SLITTING LAMINATION Solid scrap Solid scrap Solid scrap Liquid waste ink to waste management to waste management 18 Workshop Exercise PLS Company installs QC Camera Printing step • Printing errors cause high scrap rate • Quality Control (QC) 3-camera system – Detect printing errors – Operators halt the operations before too much solid scrap is generated • QC camera system costs US$105,000 to purchase and install • 40% reduced scrap and operating costs 19 Workshop Exercise • Question 1: Calculate annual cash flows using the cash flow worksheet (15 min) • Question 2: Calculate simple payback (5 min) 20 3. Net Present Value Money Loses its Value Question: If we were giving away money, would you rather have: (A) $10,000 today, or (B) $10,000 3 years from now Explain your answer... 21 3. Net Present Value Inflation Money loses purchasing power over time as product/service prices rise, so a dollar today can buy more than a dollar next year inflation 5% costs $1 now costs $1.05 next year 22 3. Net Present Value Return on Investment A dollar that you invest today will bring you more than a dollar next year — having the dollar now provides you with an investment opportunity Investing $1 now Investment 10 % interest, or “return on investment” Gives you $1.10 a year from now 23 3. Net Present Value PLS Company’s QC Camera Project Initial Investment Cost Business As Usual Installing quality control camera Annual Operating Costs 0 $ 2,933,204 $ 105,000 $ 2,894,741 Annual Savings = US$38,463 (in US$) 24 3. Net Present Value Question Is the annual savings of $38,463 per year for 3 years a sufficient return on the initial investment of $ 105,000? 25 3. Net Present Value Time Value of Money • Money is worth more now than in the future because of – Inflation – Investment opportunity • “Time value” of money depends on – Rate of inflation – Rate of return on investment 26 3. Net Present Value Cash Flows from Different Years • Before you can compare cash flows from different years, you need to convert them all to their equivalent values in a single year • It is easiest to convert all project cash flows to their “present value” now, at the very beginning of the project 27 3. Net Present Value Converting Cash Flows to Present Value Annual Savings = ?? = ?? = ?? $38,463 Year 1 Year 2 End of project $38,463 Year 3 $38,463 TIME Time zero: Initial Investment = $105,000 28 3. Net Present Value Converting Cash Flows to Present Value Discount rate: • Converts future year cash flows to their present value • Incorporates: – Desired return on investment – Inflation • Reverse of an interest rate calculation 29 3. Net Present Value Discount Rate & Interest Rate Invested at an interest rate of 20%, how much will $10,000 now be worth after 3 years? $10,000 x 1.20 x 1.20 x 1.20 = $17,280 At a discount rate of 20%, how much do I need to invest if I want to have $17,280 in 3 years? $17,280 1.20 x 1.20 x 1.20 = $10,000 30 3. Net Present Value Which Discount Rate? • Equal to the required rate of return for the project investment, based on – A basic return - pure compensation for deferring consumption – Any ‘risk premium’ for that project’s risk – Any expected fall in the value of money over time through inflation • At least cover the costs of raising the investment financing from investors or lenders (i.e. the company’s “cost of capital”) • A single “Weighted Average Cost of Capital” (WACC) characterises the sources and cost of capital to the company as a whole 31 3. Net Present Value Calculating “Present Value” Value of the cash flow in year n Present Value = Future Valuen x (PV Factor) Value of cash flow at “Time Zero,” i.e. at project start-up Present Value (PV) Factors or “discount factors” • For various values d (discount rate): 10%, 15%, 20% • For various years n (number of years) • Tables available 32 3. Net Present Value The Value of a Future $1 Discount rate (d): 10% 20% 30% 40% .9091 .8264 .7513 .6830 .6209 .3855 .1486 .0573 .8333 .6944 .5787 .4823 .4019 .1615 .0261 .0042 .7692 .5917 .4552 .3501 .2693 .0725 .0053 .0004 .7142 .5102 .3644 .2603 .1859 .0346 .0012 .0000 Years into future (n) 1 2 3 4 5 10 20 30 Handout: Table with discount rates Present value factors 33 3. Net Present Value Net Present Value (NPV) • Definition: sum of present values of all project’s cash flows – Negative (cash outflows) – Positive (cash inflows) • Characterises the present value of the project to the company – If NPV > 0, the project is profitable – If NPV < 0, the project is not • More reliable than Simple Payback or ROI as it considers – Time value of money – All future year cash flows 34 3. Net Present Value Workshop Exercise (15 min) Question 3: Calculate the NPV Year Expected Future Cash Flows X PV Factor Present Value = of Cash Flows (at time zero) 0 - $105,000 ??? - $??? 1 + $38,463 ??? $??? 2 + $38,463 ??? $??? 3 + $38,463 ??? $??? Sum = project’s Net Present Value = $??? 35 3. Net Present Value Workshop Exercise (5 min) Question 4: compare the Simple Payback and the NPV 36 3. Net Present Value Sensitivity Analysis • In business as usual scenario PLS Company needs waste water treatment plant in year 3: $150,000 investment – With QC project: $95,000 – Savings: $55,000 • Also consider taxes! – Pollution taxes / fees – Tax deductions for equipment depreciation – Tax deduction for “environmental projects” 37 3. Net Present Value Workshop Exercise (answer B) Year Expected Future Cash Flows X PV Factor Present Value = of Cash Flows (at time zero) 0 - $105,000 1 + $38,463 .8696 33,447 2 + $38,463 .7561 29,082 3 + $93,463 .6575 61.452 - $105,000 Sum = project’s Net Present Value = -18,981 38 4. Internal Rate of Return (IRR) • Definition: discount rate for which NPV = 0, over the project lifetime • Tells you exactly what “discount rate” makes the project just barely profitable • Similar to NPV, considers – Time value of money – All future year cash flows 39 Profitability Indicators Summary Advantages Disadvantages Simple Payback & ROI Easy to use Neglect TVM NPV Considers TVM Needs firm’s discount rate Indicates project size IRR Considers TVM Neglect out-year costs Do not indicate project size Requires iteration Does not indicate project size 40 Financial Feasibility Analysis of Options Thank you for your attention! 41 Acknowledgements This training session was prepared as part of the development and delivery of the course “Energizing Cleaner Production” funded by InWent, Internationale Weiterbildung und Entwicklung (Capacity Building International, Germany) and carried out by the United Nations Environment Programme (UNEP) The session is based on the presentation “Financing Cleaner Production and Energy Efficiency Projects” from the “Energy Efficiency Guide for Industry in Asia” developed as part of the GERIAP project that was implemented by UNEP and funded by the Swedish International Development Cooperation Agency (Sida). www.energyefficiencyasia.org The workshop exercise is taken from “Profiting from Cleaner Production”, in Strategies and Mechanisms For Promoting Cleaner Production Investments In Developing Countries, developed by UNEP 42