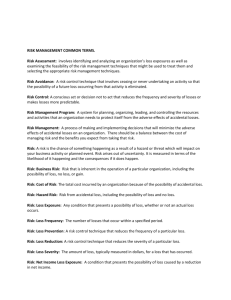

Energy Insurance and

Risk Management

Finance 4359/7397

Professor Dan C. Jones

C. T. Bauer College of Business

Risk Management Purpose to Finance

Claim Payments

• Risk Management Methods

– Retain/Self Insure

– Transfer/Insure

– Control

• Limitations

2

Lets see how well we have done

3

1937

• New London, Texas

• Natural Gas explosion in school over 200

killed

• Now use t-butyl mercaptan or thioplane

4

1989

• Exxon Valdez

• Spilled 10.8 million gallon of crude off coast

of Alaska, Prince William Sound

• Now require double hull crude carriers in all

US ports

• March 2009 Korean vessel found a drilling rig

lost after IKE, Double Hull prevented any spill

5

2004

• Explosion BP plant Texas City

• Extensive damage. BP admitted fault but

ignition came during recovery cycle but

fatalities due to location of work trailers

6

2005

• Hurricane Katrina & Rita

– Failure of flood gates New Orleans

– Inadequate wave clearance & offshore platforms

for class 5 storm

– Inadequate response FEMA

7

2008

• Hurricane Ike

– Class 2 winds offshore

– Class 5 storm surge Galveston Bay and Trinity Bay

– Now referred to as Integrated Kinetic Energy

– Over 2,000,000 million customers lost power.

Unforeseen especially by CenterPoint.

8

1984

• Bhopal India- Union Carbide pesticide plant

– 300 killed, thousands injured release of 42 tons of

methyl isocyanate

– Plant was not following safety and operating

guidelines of Union Carbide

9

1986

• Chernobyl, Ukraine explosion released more than 400

times the radioactivity than with atomic bombing of

Hiroshima

– Built a sarcophagus a cover for the reactor

• That and Three Mile Island incident stopped

any nuclear construction, in US in 1970’s.

Now 4 projects being considered in Texas

10

2002

• Approved repository site in Yucca Mountain, Nevada

– Operational 2010, to be sealed 2035

– Repository in solid rock 1000 feet underground

and on average 1000 feet above water table

– Holds 77000 metric tons of waste Plulonuim-239

has half life of 24000 years Cost $9 billion

– 2010 budget includes no funding for Yucca

Mountain

– Present 100 nuclear plants-20% of electricity 30

plants in planning stage

11

Asbestos- Alaska Pipe Line recognition Asbestosis and

mesothelioma but was used in shipbuilding in 1940’s

Used by the Ancient Greeks because of its soft and

pliant properties- the miracle mineral

Over 80 companies involved with asbestos have filed

for chapter 11 beginning with Johns Mansville

12

US Air Flight 1549

Sulley Sullenberger

Airbus A 320-214

N10GUS

13

1988

• North Sea- Piper Alpha Platform

– Explosion many workers killed platform severely

damaged.

– Equipment stacked near crew quarters

– Due to economic effort for more production

14

SEMPRA Energy

Owners of San Diego Gas & Electric- SDGE

2007 Wildfires in California

Have $1.1 billion tower of liability insurance on

aggregate basis and now totally consumed.

15

But in all my experience, I have never been in

any accident… of any sort worth speaking

about I have never seen but one vessel in

distress in all my years at sea. I never saw a

wreck and never have been wrecked nor was I

ever in any predicament that threatened to end

in any disaster of any sort.

16

EJ Smith

Captain-Titanic

1907

17

We can add others not directly part of energy but which

impact us all

9-11

Enron

AIG

Banking system

2001

2001

2008

2007-08

We do live in a risky world

18

Others

• Draught

– Began 2008

– Will continue in 2012

• Cargo Ship Rena

– Breaks up off Tauranga Harbor, New Zealand

19

• Catastrophe Losses

• Insured Losses

• Natural Disasters

• $105 Billion

20

2010

Macondo

Gulf of Mexico

Transocean

British Petroleum

Halliburton

Anadarko

Cameron

Issues

– Damages

– Fault

– Liability

21

Insurance Buyer

Insurance Manager

Risk Manager

Director of Risk Management

Enterprise Risk Management

Sustainability Risk Management

22

Risks we have failed to manage

Banks

Investment Houses

Merrill Lynch

Lehman Bros

Bear Stearns

All from

Sub prime Credit Crises

Mortgage valued securities

CDO’s- Collateralized Debt Obligations

Credit Default Swaps

AIG- a subject all its own

23

New Risks

Cyber Liability

Gamma- Ray Burst

Nanotechnology

Somalia Pirates

Global Warming

24

http://www.houstonpress.com/

25

26

Insurance Regulation

State Regulation

Federal Regulation

Optional Regulation

Insurance CZAR Candidate

Opinions

27

Is the insurance market stable?

Will the regulation applying to insurance, state

vs. federal change?

Will we have federal regulation?

Will new leaders become known for the

insurance industry?

28

Summary

We all have risks

Our challenge is to finance the losses that occur

Risk management is the art of selection of the

method(s) to pay

We cannot eliminate all risk nor should we

29

Risk Assumption

Assume risks that are comfortable and

predictable

Transfer those risks that could negatively impact

your company

Be mindful of the risk bearing capacity of your

company

There are limitations- one is Chapter 11

30

BP

April 20, 2010

•

•

•

•

•

•

BP Blow out

Macondo Blow out

Deepwater Horizon Blow out

Vessell - $575,000,000

11 deaths

17 injured

31

Gulf Issues/Energy

•

•

•

•

•

•

•

•

BP Pollution Liability

Liability

Force Majure

Insurance

No Insurance

Available Limits

Inspections

Regulation

32

• Risk financing vs. Risk management

• Risk and the world

• As a society, always sought to reduce

uncertainty-tribes/clans

• Business but an extension and risk is at

heart of ALL business operation

• Decisions cross borders and industriesharm to stakeholders

33

•

•

•

•

•

•

•

Language of risk & insurance

Risk

Speculative risk

Pure risk

New term-enterprise risk

Management of Risks

A process

– Identification and evaluation

– Exploration of Techniques

– Implementations and review

• Current Risk management

• Losses without gain

• Holistic approach

34

• Fundamentals of risk & uncertainty

• Risk- variation of outcomes

• Uncertainty- the doubt from inability to

predict future (outcomes)

• Arises from risk

• Add managers and becomes complicated

35

• Corporate demand for insurance

• Risk managers assumed risk neutral

• Assumption

– Increasing wealth leads to inc. Satisfaction

AND

– Marginal utility constant as wealth increases

• Individuals risk adverse but

• Owners / shareholders are not

• Investors require higher return if unable to

diversify or systemic risk

• CAPM theory

36

• Shareholder risk aversion does not explain why

corporations buy insurance why?

• Insurance companies have comparative

advantage

• Insurance can lower cost of financial distress

• Insurers may have service efficiencies

• Insurance can lower tax liabilities (property)

• Regulated industries have higher demand

• Compulsory insurance laws

• Financial consideration of stock price

37

• Practitioners increasingly taking holistic

approach

• Conceptual and applied economic knowledge

continues to expand

• Private markets can not deal with some societal

risks

• Publicly traded companies undergoing

evolutionary changes

• Resources committed to understanding capacity

of capital markets

• A challenge for ALL

38

• Economic development

• Benefits

– More competitive

– Better values

– Shareholder value increased

– Cash flow leveling

– Reduces insolvency

– Expands credit availability

– Loss control / risk control

• Reduced costs results and better able to

compete

39

•

•

•

•

•

Property rights and economic freedom

Right to own real & personal property

Right to enter into contracts

Right to be compensated for tortious acts

Needed

– A system and a means to enforce

• Markets are means of exchanging property

rights

• Insurance can not function without defined

ownership interests

• Restrictive - monopolies, insider trading

40

•

•

•

•

Hard market

Soft market

9/11

Today

41

•

•

•

•

Value of insurance company services

Pricing, underwriting, claims handling

Pricing - statisticians / actuaries

Time lag of loss payments and premium

payments

• Competitive premium is of expected losses,

expenses, profit

• Investment return

– Life companies -calculable

– Non-life - long tail claims

• Government treatment

42

• Internationalization of business creates

internationalization of financial services

• No one market can provide all needed

coverage

–

–

–

–

–

–

Oil refineries

Oil tankers

Off shore rigs

Satellites

Jumbo jets

Environmental impairment

• National markets benefit

• Increase competitiveness

43

• The financial environment

• Finance and insurance have much in

common

• Each provide its customers tools for

managing risks AND

• Valuation methods are the same

– Fair value of the security

– An insurance policy

– Based on discounted cash value of future cash

flows

44

• Same definition of risk- the variation of

future results from expected values

• Rely on same fundamental concepts

– Risk pooling

– Risk transfer

• Therefore we have convergence as

insurance company managers, owners and

customers must recognize and understand

45

• Risk management fundamentals

• What is risk?

• Is risk different if building a new plant in

Jakarta?

– Currency

– Language

– Training / hiring

– Laws

• Separate

– Hazard risk management

– Financial risk management

46

• Objective of risk management - to

contribute to a firms value

• Factors

– Unmanaged risk reduce value of firm

– With increase in risk, cost of doing business

increases

– Results in lower levels expected cash flow

• Reciprocal is that

– Reducing risk increases cash flow

– Increases value of firm

47

• Risk assessment

– Identification of exposure

– Analyzing to determine potential impact

• Assets subject to loss

– Tangible, intangible, human

– The analysis should answer

• What assets are exposed

• What perils can cause harm

• What are potential consequences

48

• Financial loss

• Property

– Real property

– Personal property

– Intangible property

• Net income losses (revenue less expenses)

– Fire losses

– Auto accident

– Employee injury

• Magnitude function of revenue decrease

• Insurance terms - time element or business

interruption because it is time dependent

49

• Liability losses

• Occur when parties assert legal rights

• Many types - mostly civil in nature

– Defective products

– Environmental impairment

– Injury to employees

– Breach of contract

– Professional errors or omissions

• Huge cost associated with defense even if

no liability

50

• Personnel losses - human assets

– Injury

– Disability

– Death

– Retirement

– Resignation

– Kidnapping

• Which consumes most time?

51

•

•

•

•

•

External influences broadening scope of risks

Globalization

Industry consolidation

Deregulation

Regulatory attention to corporate governance

– Sarbanes-Oxley

• Technological progress enabling better risk

quantification and analysis

52

Internal Factors

• Increased firm value – the emphasis

– Reduces inefficiencies inherent in traditional

approach

– Improving capital efficiencies

– Stabilize earnings

– Reduce expected costs of external capital

53

Forces Creating Uncertainty

•

•

•

•

•

•

•

•

Technology and Internet

Increased worldwide competition

Freer trade and investment worldwide

Complex financial instruments, notably

derivatives

Deregulation of key industries

Changes in organizational structures resulting

from downsizing, reengineering, and mergers

Higher customer expectations for products and

services

More and larger mergers

54

• Enterprise Risk Management (ERM)

• Synonymous with:

– Integrated Risk Management (IRM)

– Holistic Risk Management

– Enterprise-wide Risk Management

– Strategic Risk Management

55

Alternatives to Insurance

•

•

•

•

•

Retentions

Self Insurance

Captives

Mutual Company

Industry developments as alternative

–

–

–

–

Weather

Loss portfolio transfer

Finite

Securitization

56

Retention

Capacity

Rules of Thumb

•

•

•

•

•

Shareholders Equity2 - 3%

Pre-tax Earnings

5 - 10%

Cash Flow

4 – 5%

Total Assets

1 – 2%

Earnings

10%

57

Risk Management Continuum

Mitigate

Retain

Transfer

58

World Market

• United States

– Stock

– Mutual

• European

• Reinsurance

• Lloyds of London

FINA 4397/7397

59

∑ of the Good

60

0

0