MICROECONOMICS:Theory & Applications Chapter 1 An

advertisement

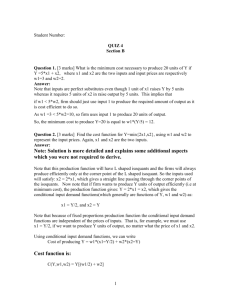

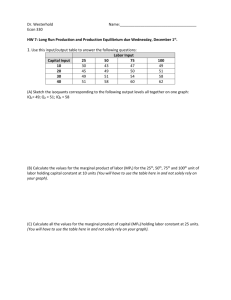

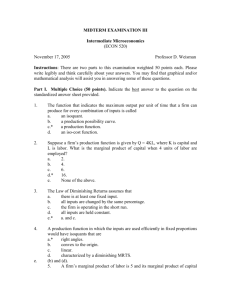

MICROECONOMICS: Theory & Applications Chapter 7 Production •By Edgar K. Browning & Mark A. Zupan •John Wiley & Sons, Inc. •9th Edition, copyright 2006 •PowerPoint prepared by Della L. Sue, Marist College Learning Objectives • Establish the relationship between inputs and output. • Distinguish between variable and fixed inputs. • Define total, average, and marginal product. • Understand the Law of Diminishing Marginal Returns. (Continued) Learning Objectives (continued) • Investigate the ability of a firm to vary its output in the long run when all inputs are variable. • Explore returns to scale: how a firm’s output response is affected by a proportionate change in all inputs. • Overview how production relationships can be estimated and some difference potential functional forms for those relationships. Relating Output to Inputs • Factors of production – inputs or ingredients mixed together by a firm through its technology to produce output • Production function – a relationship between inputs and output that identifies the maximum output that can be produced per time period by each specific combination of inputs Q = f(L,K) • Technologically efficient – a condition in which the firm produces the maximum output from any given combination of labor and capital inputs Production When Only One Input is Variable: The Short Run • Fixed inputs - resources a firm cannot feasibly vary over the time period involved • Total product - the total output of the firm • Average product - the total output divided by the amount of the input used to produce that output • Marginal product - the change in total output that results from a one-unit change in the amount of an input, holding the quantities of other inputs constant Total, Average, and Marginal Product Curves [Figure 7.1] Production Output Table Production Table - Table 7.1 Capital 3 3 3 3 3 3 3 3 3 3 Labor 0 1 2 3 4 5 6 7 8 9 TP 0 5 18 30 40 45 48 49 49 45 MP of Labor AP 5 5 9 13 10 12 10 10 9 5 8 3 7 1 6.125 0 5 -4 The Relationship Between Average and Marginal Product Curves • When the marginal product is greater than average product, average product must be increasing. • When the marginal product is less than average product, average product must be decreasing. • When the marginal and average products are equal, average product is at a maximum. [Figure 7.2] The Law of Diminishing Marginal Returns • A relationship between output and input that holds that as the amount of some input is increased in equal increments, while technology and other inputs are held constant, the resulting increments in output will decrease in magnitude Production When All Inputs Are Variable: The Long Run • Short run – a period of time in which changing the employment levels of some inputs is impractical • Long run – a period of time in which the firm can vary all its inputs • Variable inputs – all inputs in the long run Production Isoquants • Isoquant – a curve that shows all the combinations of inputs that, when used in a technologically efficient way, will produce a certain level of output • Characteristics: – Isoquants must slope downward as long as both input are productive (I.e., marginal products > 0) – Isoquants lying farther to the northeast identify greater levels of output – Two isoquants can never intersect. – Isoquants will generally be convex to the origin. Marginal Rate of Technical Substitution (MRTS) • The amount by which one input can be reduced without changing output when there is a small (unit) increase in the amount of another input • When the MRTS diminishes along an isoquant, the isoquant is convex. Production Isoquants [Figure 7.3] MRTS and the Marginal Products of Inputs MRTSLK = (-) ΔK/ΔL = MPL/MPK Returns to Scale • Constant returns to scale – a situation in which a proportional increase in all inputs increases output in the same proportion • Increasing returns to scale – a situation in which output increases in greater proportion than input use • Decreasing returns to scale – a situation in which output increases less than proportionally to input use • Figure 7.5 Factors Giving Rise to Increasing Returns • Specialization and division of labor • “Volume” capacity increases faster than “area” dimensions (arithmetic relationship) • Available of techniques that are unique to large-scale operation Factors Giving Rise to Decreasing Returns • Inefficiency of managing large operations: – Coordination and control become difficult – Loss or distortion of information – Complexity of communication channels – More time is required to make and implement decisions Functional Forms and Empirical Estimation of Production Functions • Functional Forms – Linear • Q = a + bL + cK – Multiplicative • Cobb-Douglas production function: Q = aLbKc • Empirical Estimation Techniques – Survey – Regression analysis