Snímek 1

advertisement

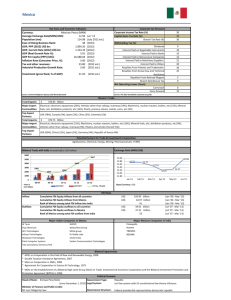

Policy on Foreign Direct Investments in the CR „There is no free Lunch“ Eva Zamrazilová, Chief economist Czech Banking Association 1 Basic story of previous two decades 6.5 4.8 4.6 4.3 5.5 3 1.3 -0.7 -0.3 7.1 2.1 2.5 3.6 2.5 2 1.6 -0.7 GDP, y/y, % -0.7 -4.7 • • • • • First posttransformation recovery 1994 - 1996 May 1997 monetary crisis followed by recession and banking crisis Recovery as of 2000 with growth peaking in 2005-2007 („golden age“) Big slump (crisis) in 2009 followed by moderate growth 2010-2011 Recovery after 6 quarters of recession (Q2/2013- Q3/2013) 2 Strong inflow of FDI as of 1998 70 60 50 40 30 20 10 0 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 FDI stock, (%of GDP) •Czech government has supported inflow of FDI as of 1998, FDI incentives as of 2000 •The stock of FDI (66 % of GDP) is very high in the world context • The companies under foreign control create almost one third of GDP 3 Strong inflow of FDI as of 1998 3000 2500 2000 Credits to non-financial companies, y/y, CZK bill. FDI Inward stock, CZK bill. Investments, CZK bill 500,000 Exports, CZK bill. 400,000 1500 300,000 1000 200,000 0 100,000 0 -100,000 Q1/95 Q4/95 Q3/96 Q2/97 Q1/98 Q4/98 Q3/99 Q2/00 Q1/01 Q4/01 Q3/02 Q2/03 Q1/04 Q4/04 Q3/05 Q2/06 Q1/07 Q4/07 Q3/08 Q2/09 Q1/10 Q4/10 Q3/11 Q2/12 Q1/13 Q4/13 500 • Foreign investors have been strongly appreciated for : • increasing the export competitiveness, access to world markets • non-debt financing of investments • transfer of technology • managerial skills • promoting economic growth without pressures on external balance 4 Foreign controlled companies in the business sector 80.0 70.0 60.0 50.0 40.0 30.0 20.0 10.0 Share of FCC on value added in the business sector (%) Share of FCC on investment in the business sector (%) 2,012 2,011 2,010 2,009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 0.0 Share of FCC on profit in the business sector (%) Source: CZSO FCC in the business sector account for approximately: • One half of value added in the business sector (non-financial companies) • Two thirds of profit in the business sector (non-financial companies) • 75 % of direct export sales • Almost half of investments in the business sector (non-financial companies): 46 % (2007) → 40 % (2011) The shares have been highest in value added in machinery : automotive industry (92 % of VA), electronics (80 %) , electrical appliances (73 %), general machinery (83 %) 5 Dual economy has been persisting Differences in productivity between FCC and private domestic companies Output per worker (CZK million) Value added per worker (CZK million) 2.5 2 1.5 1 0.5 : 0 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2,009 2,010 2,011 Source:CZSO • • • The differences in productivity have been persisting – measured either by output per worker or value added per worker The theory says that persisting duality prevents the positive FDI spillovers to domestic comapnies( Jindra et al, 2009, Narula a Driffield, 2012) The studies focused on CR confirm cheap labour force as a very important factor attracting FDI – Král (2004), Hunya a Geishecker (2005) 2,012 High and stable profitability of FDI in the CR FDI stock and profits from FDI, 1995 - 2013 350 y = 0,1298x - 38,106 R² = 0,9607 300 250 200 150 100 50 0 0 500 1000 1500 2000 2500 Source: CNB and own calculations • Correlation between FDI stock and their profitability is quite strong • Coefficient ß corresponds well to ROE (13 %) • In the international comparisons , CR is in the Top Twenty (UNCTAD, 2013) (as the only one among developed economies) 3000 The crisis has interrupted reinvestments of profits FDI stock (x axis, CZK bill.) and reinvestments (y axis , CZK bill.) 1995-2007 160 FDI stock (x axis , CZK bill.) and reinvestments (y axis , CZK bill.) 1995- 2013 y = 0,0719x - 19,978 R² = 0,9715 140 160 y = 0.0312x + 9.7859 R² = 0.5093 140 120 120 100 100 80 80 60 60 40 40 20 20 0 0 0 500 1000 1500 2000 2500 -20 0 500 1000 Source: CNB, own calculations 1500 2000 2500 Source: CNB, own calculations • Profits = reinvestments+dividends • Strong correlation between FDI stock and reinvestments of profits up to 2007, later on becomes very weak 3000 FDI: reinvestments and dividends 350 300 Dividends (CZK bill.) 250 Reinvestments (CZK bill.) 159.7 223.7 200 204.1 201.6 150 110.8 73.5 100 16.4 50 0 • • • • 178.5 5.4 5.8 1998 32.7 52.1 218.5 183.6 72.9 140.5 8.6 23.9 10.8 36.9 57.8 64.3 60.9 75.8 1999 2000 2001 2002 2003 2004 78.2 87.2 41.2 2005 2006 2007 2008 67.7 75.9 2009 2010 78 95.3 38 2011 2012 2013 Sharp change of foreign investors behaviour as of 2008 The FDI life cycle theory cannot give full explanation The outflow caused by sharp change of profit strategy is astimated at CZK 400 bill. Rough estimate indicate the yearly loss in GDP incurred by sharp change of investment strategy of multinationals around 1 – 1,5 % of GDP since 2008 9 Gross national income (in % of GDP) 102 100 98 96 94 92 90 88 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Source:Ministry of Finance • • • Gross national income= gross domestic product + balance of primary incomes (approximately balance of incomes as a part of current account) Gross national income reflects the part of GDP disposable in the respektive national economy) The difference between GNI and GDP (GNI – GDP) represents the part of value added which is produced in the respective economy but belongs to foreign subjects GDP and its factors 20 800,000 720,000 640,000 560,000 480,000 400,000 320,000 240,000 160,000 80,000 0 10 0 -10 -20 Investments ,,CZK bill, constant prices 2010 Exports, CZK bill, constant prices 2010 • • • GDP, y/y, % Consumption of households, y/y, % Investments, y/y, % Exports, y/y, % 3 per. Mov. Avg. (Investments, y/y, %) 4 per. Mov. Avg. (Exports, y/y, %) Czech economy was strongly hit by the fall of foreign demand during the crisis Exports have recovered soon, which was not the case for investments Weak investments were an important factor od prolonged recession (Q2 2012 – Q3 2013) 11 Conclusion • • • • • • • • Strong inflow of FDI has resulted into high penetration of foreign controlled companies into domestic Czech economy The pre-crisis success story of the Czech economy was largely due to FDI However, high share of companies under foreign control led to new form of dependency Uncertain future ahead – not only exports but also investments will be determined by multinationals Solid export performance is not enough for growth of investments and wages Conditions of mothers will strongly affect domestic companies - sometimes „daughters feeding their mothers“ Czech policy of FDI incentives just blindly followed neighboring countries and the CR became winner in the „leap to the unknown“ Strategy for FDI inflow is an important part of economic policy – contrary to monetary or fiscal policy, theoretical background of short-term versus long-term consequences has been missing 12 Some reccomendations for economic policy • Strengthening role of domestic SMEs achieving a better balance between big foreign companies under foreign control – long-term stable and transparent environment highly needed • Stable environment could also help to promote reinvestments of big multinationals • Support of relationship between big companies and SMEs • FDIs should not be promoted and attracetd blindly – stratégy first • The analysis of real impact of FDI incentives in the past . Suggested literature • • • • • • • • • • • • • • Bolcha,P.,Zemplinerová,A. (2012).Dopad investičních pobídek na objem investic v České republice. Politická ekonomie, Vol.60, č.1,s. 81-100. Blomstrom, M., Kokko, A. (1997). How Foreign Investment Affect Host Countries. The World Bank, Working Paper No. 1745. Criscuolo, P, et al. (2005). Measuring knowledge flows among European and American multinationals: a patent citation analysis. Economics of Innovation and New Technologies, Vol. 14, p. 417-433. Dries, L., Swinnen, J. F. M. (2004). Foreign direct investment, vertical integration, and local suppliers: Evidence from the Polish dairy sector., World Development, Vol. 32, No 9, pp. 1525–1544. Gorg, H., Greenaway, D. (2003). Much ado about nothing? Do domestic firms really benefit from foreign direct investment?. World Bank Research Observer, No.19: 171–197. Hansen, H.,Rand, J. (2006). On the causal links between FDI and growth in developing countries, World Economy, Vol. 29, No.1, pp. 21-41. Hunya, G., Geishecker, I. (2005).Employment Effects of Foreign Direct Investment in Central and Eastern Europe. Vienna, WIIW August 2005, Research report No. 321. Chowdhury, A., Mavrotas. G. (2006). FDI and growth: What causes what? World economy, Vol 29, No.1, pp 9-19. Jindra, B. et al . (2009) Subsidiary Roles, Vertical Linkages and Economic Development: Lessons from Transition Economies, Journal of World Business, Vol. 44, No.2, pp. 167-17. Jindra, B. et al. (2006). Theories and review of the latest research on the effects of FDI in CEE. In J. Stephan (Ed.), Technology transfer via foreign direct investment in Central and Eastern Europe – Theory, method of research – Empirical evidence (pp. 3–74). Houndsmill Basingstoke Palgrave, MacMillan 2006. Král,P. (2004). Identification and Measurement of Relationships Concerning Inflow of FDI: The Case of the Czech Republic. Working paper No. 5, Czech National Bank. Lall, S., Narula, R. (2004). FDI and its role in economic development: Do we need a new research agenda? The European Journal of Development Research, Vol. 16, No 3, pp. 447–464. Suggested literature • • • • • • • • • • • • • • Lim, E.G. (2001). Determinants of, and Relation Between, FDI and growth: A Summary of the Recent Literature. Working paper No. 01/175, IMF, Washington. Mandel,M.,Tomšík,V. (2006). Přímé zahraniční investice a vnější rovnováha v tranzitivní ekonomice: aplikace teorie životního cyklu. Politická ekonomie, Vol. 54, č.6, s. 723-741. Narula, R.,Driffield,N. (2012). Does FDI cause development? The ambiguity of the evidence and why it matters. European journal of developmental research, Vol. 24, No. 1, pp. 1-7. Narula, R., Dunning, J. H. (2000). Industrial development, globalization and multinational enterprises: New realities for developing countries. Oxford Development Studies, Vol.28, No.2, pp.141–167. Narula, R., Dunning, J. H. (2010). Multinational enterprises,, development and globalization. Some clarifications and a research agenda. Oxford Development studies, Vol 38, No. 3, pp. 263-287. Smarzynska – Javorcik, B. (2004): Does FDI Increase the Productivity of Domestic Firms?. In Search of Spillovers Through Backward Linkages. The American Economic Review. Vol. 94, No. 3, pp. 605–626. Spěváček, V. (2005). K vývoji souhrnných ukazatelů reálného důchodu v České republice. Statistika, 2005, č.3, s.188-204. Spěváček,V.a kol. (2012). Makroekonomická analýza. Praha, Linde, 2012. UNCTAD (2001). World Investment Report 2001: Promoting Linkages. New York and Geneva: United Nations. UNCTAD (2005). World Investment Report 2005: Transnational Corporations and the Internationalization of R&D, United Nation’s Conference on Trade and Competitiveness, New York and Geneva: United Nations. UNCTAD (2006). World Investment Report 2006: FDI from Developing and Transition Economies: Implications for Development. United Nation’s Conference on Trade and Competitiveness, New York and Geneva: United Nations. UNCTAD (2012). World Investment Report 2012: Towards a New Generation of Investment Policies. New York and Geneva: United Nations. UNCTAD (2013). World Investment Report 2013: Global value Chains: Investment and Trade for Development. New York and Geneva: United Nations. Zamrazilová, E. (2007). Přímé zahraniční investice v české ekonomice: rizika duality a role trhu práce. Politická ekonomie, Vol.55, č. 5, s.579-602. Thank you for attention Eva Zamrazilová zamrazilova@czech-ba.cz 16